MIT Sloan Finance Problems

and Solutions Collection

Finance Theory I

Part 2

Andrew W. Lo and Jiang Wang

Fall 2008

(For Course Use Only. All Rights Reserved.)

1

Acknowledgement

The problems in this collection are drawn from problem sets and exams

used in Finance Theory I at Sloan over the years. They are created by many

instructors of the course, including (but not limited to) Utpal Bhattacharya,

Leonid Kogan, Gustavo Manso, Stew Myers, Anna Pavlova, Dimitri Vayanos

and Jiang Wang.

CONTENTS CONTENTS

Contents

1 Questions 4

1.4 Forward and Futures . . . . . . . . . . . . . . . . . . . . . . . 4

1.5 Options . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

1.6 Risk & Portfolio Choice . . . . . . . . . . . . . . . . . . . . . 19

1.7 CAPM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

1.8 Capital Budgeting . . . . . . . . . . . . . . . . . . . . . . . . 42

2 Solutions 45

2.4 Forward and Futures . . . . . . . . . . . . . . . . . . . . . . . 45

2.5 Options . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55

2.6 Risk & Portfolio Choice . . . . . . . . . . . . . . . . . . . . . 79

2.7 CAPM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 90

2.8 Capital Budgeting . . . . . . . . . . . . . . . . . . . . . . . . 104

3

c

° 2008, Andrew W. Lo and Jiang Wang

1 QUESTIONS

1 Questions

1.4 Forward and Futures

1. During the summer you had to spend some time with your uncle, who

is a wheat farmer. Your uncle, knowing you are studying for an MBA

at Sloan, asked your help. He is afraid that the price of wheat will fall,

which will have a severe impact on his profits. Thus he asks you to

compute the 1yr forward price of wheat. He tells you that its current

price is $3.4 per bushel and interest rates are at 4%. However, he also

says that it is relatively expensive to store wheat for one year. Assume

that this cost, which must be paid upfront, runs at about $0.1 per

bushel. What is the 1yr forward price of wheat?

2. The Wall Street Journal gives the following futures prices for gold on

Septemb er 6, 2006:

Maturity Oct Dec Jun 07 Dec 07

Futures price ($/oz) 635.60 641.80 660.60 678.70

and the spot price of gold is $633.50/oz. Compute the (effective annu-

alize) interest rate implied by the futures prices for the corresponding

maturities.

3. Suppose that in 3 months the cost of a pound of Colombian coffee will

be either $1.25 or $2.25. The current price is $1.75 per pound.

(a) What are the risks faced by a hotel chain who is a large purchaser

of coffee?

(b) What are the risks faced by a Colombian coffee farmer?

(c) If the delivery price of coffee turns out to be $2.25, should the

farmer have forgone entering into a futures contract? Why or

why not?

4. Consider a 6-month forward contract (delivers one unit of the security)

on a security that is expected to pay a $1 dividend in three months.

The annual risk-free rate of interest is 5%. The security price is $20.

What forward price should the contract stipulate, so that the current

value of entering into the contract is zero?

5. Spot and futures prices for Gold and the S&P in September 2007 are

given b elow.

4

c

° 2008, Andrew W. Lo and Jiang Wang

1.4 Forward and Futures 1 QUESTIONS

07-September 07-December 08-June

COMEX Gold ($/oz) $693 $706.42 $726.7

CME S&P 500 $1453.55 $1472.4 $1493.7

Table 1: Gold and S&P 500 Prices on September 7, 2007

(a) Use prices for Gold to calculate the effective annualized interest

rate for Dec 2007 and June 2008. Assume that the convenience

yield for Gold is zero.

(b) Suppose you are the owner of a small gold mine and would like

to fix the revenue generated by your future production. Explain

how the futures market enables such hedges.

6. Use the same set of information given in the problem above.

(a) Use S&P 500 future prices to calculate the implied dividend yield

on S&P 500. For simplicity, assume you can borrow or deposit

money at the rates implied by Gold’s futures prices.

(b) Now suppose you believe that we are headed for a slow-down in

economic activity and that the dividend yield will be lower than

the value implied in part (a). What June-2008 contracts you would

buy or sell to make money, assuming your view is correct? Again,

assume you can borrow or deposit money at the rates implied by

Gold’s futures prices.

7. The Wall Street Journal gives the following futures prices for crude oil

on Septemb er 6, 2006:

Maturity Oct Dec Jun 07 Dec 07

Futures price ($/barrel) 67.50 69.60 72.66 73.49

and the spot price of oil is $67.50/barrel. Use the interest rates you

found in the previous problem.

(a) Compute the net convenience yield (in effective annual rate) for

these maturities. (You can use the market information provided

in the above problem.)

(b) Briefly discuss the convenience yield you obtained.

8. The data is the same as in the two problems above. You are running a

refinery and need 10 million barrels of oil in three months.

(a) How do you use oil futures to hedge the oil price risk? The contract

size is 1,000 barrels for futures.

5

c

° 2008, Andrew W. Lo and Jiang Wang

1.4 Forward and Futures 1 QUESTIONS

(b) Suppose that you can also rent a storing facility for 10 million

barrels of oil for three months at an annualized cost of 5% (in

terms of the value of oil stored). Describe how you can utilize it

to lock into a fixed oil price for your future demand.

(c) Which of these two strategies is better? Explain why.

9. The data is the same above. Now suppose instead that you are not in

the oil business but can also rent the storage facility at the same cost.

Can you take advantage of the current market conditions and the rental

opportunity? If yes, please explain how (i.e., describe the actions you

need to take). If not, briefly explain why.

10. The current price of silver is $13.50 per ounce. The storage costs are

$0.10 per ounce per year payable quarterly at the beginning of each

quarter and the interest rate is 5% APR compounded quarterly (1 .25%

per quarter).

(a) Calculate the future price of silver for delivery in nine months.

Assume that silver is held for investment only and that the con-

venience yield of holding silver is zero.

(b) Suppose the actual price of the futures contract traded in the

market is below the price you calculated in part (a). How would

you construct a risk-free trading strategy to make money? What

if the actual price is higher? To get full credit, say precisely what

you will buy or sell, and how much money you will borrow or

deposit into a bank account and for how long.

11. A pension plan currently has $50M in S&P 500 index and $50M in

one-year zero-coupon bonds. Assume that the one-year interest rate is

6%. Assume that the current quote on the S&P 500 index is 1, 350, each

futures contract is written on 250 units of the index and the dividend

yield on the index is approximately 3% per year, i.e., $1, 000 invested

in the index yields $30 in dividends at the end of the year.

(a) Suppose you invest $1, 350 × 250 in one-year zero-coupon bonds

and at the same time enter into a single futures contract on S&P

500 index with one year to maturity. Assume that in one year the

index finishes at 1, 200. What is the total value of your p osition?

How does this compare with buying 250 units of the index and

holding them for a year? Assume that in one year the index

finishes at 1, 400. Repeat the analysis.

(b) If this plan decides to switch to a 70 /30 stock/bond mix for a

perio d of one year, how would you implement this strategy using

S&P 500 futures? How many contracts with one year to maturity

6

c

° 2008, Andrew W. Lo and Jiang Wang

1.4 Forward and Futures 1 QUESTIONS

would you need? Assume that the index finishes the year at 1, 400,

describe the plan’s portfolio in one year and one day from now

(right after the futures expire). What is the stock/bond mix?

12. Spot price for soybean meal is $152.70 per ton and the 12-month

soyb ean-meal futures is traded at $148.00. The 1-year interest rate

is 3%.

(a) What is the net convenience yield on soybean meal for the 12

month p eriod?

(b) You need 1,000 tons of soybean meal in 12 months. How would

you lock into a price today using the futures contracts? (The size

for each soybean-meal futures contract is 100 tons.)

13. The spot price for smoked salmon is $5,000 per ton and its six-month

futures price is $4,800. The monthly interest rate is .0025 (.25%).

(a) What is the average monthly net convenience yield on smoked

salmon for the next six months?

(b) If you are a manager of Bread&Circus and need 10 tons of smoked

salmon in six months. How can you avoid the risk in the price of

smoked salmon over the next six months using futures?

(c) Suppose that your net convenience yield for smoked salmon is

1.2%. How does this change your hedging strategy?

14. A wine wholesaler needs 100,000 gallons of Cheap Chardonnay for de-

livery in Boston in June 2007. A producer offers to deliver the wine at

that time for $500, 000 paid now, in December 2006.

The wholesaler can also buy Cheap Chardonnay futures contracts for

June 2007. The current futures price is $51, 000 for each 10,000 gallon

futures contract.

The wholesaler is determined to lock in the cost of the 100,000 gallons

needed in June.

(a) The wholesaler considers the futures contract, but worries that

the contract will not lock in her cost, because futures prices may

fluctuate widely between now and June. Is her concern justified?

Why or why not?

(b) Do you recommend that the wholesaler pay the producer now or

take a long position in Chardonnay futures? (Additional assump-

tions may be needed to answer. Make sure they are reasonable.)

Explain briefly.

7

c

° 2008, Andrew W. Lo and Jiang Wang

1.4 Forward and Futures 1 QUESTIONS

15. You are a distributor of canola seed and need to make deliveries of

10,000 bushels one month from now. You currently have no canola

seed in inventory. The current spot price of canola seed is $7.45 per

bushel and the futures price for delivery in one month is $7.65. You

would like to hedge the uncertainty about the spot price one month

from now.

(a) If your storage cost is $.15 per bushel (paid at the end of month),

what would you do?

(b) Suppose that in the short run, your storage cost increases to $.25

per bushel. What would you do?

16. Assume perfect markets: no transaction costs and no constraints. In

addition assume that the one-month risk-free interest rate will remain

constant over a three-month period. Two futures contracts with two

and three months maturity are traded on a financial asset without any

intermediate payout. The price for these contracts are F

2

= $100 and

F

3

= $101, respectively.

(a) What is the spot price of the underlying asset today?

(b) Suppose that a one-month futures contract is trading at price

F

1

= $98. Does this imply an arbitrage opportunity? How would

you take advantage of this opportunity? To get full credit, be

precise on what you would buy or sell, and how much money you

would dep osit into a bank account and/or borrow.

17. Assume perfect markets: no transaction costs and no constraints. The

one-month risk-free interest rate will remain constant over a six-month

perio d. Two futures contracts are traded on a financial asset without

payouts: a three-month (futures price F (t, t + 3)) and a six-month

(futures price F (t, t + 6)) contract. You can observe that F (t, t + 3) =

$120 and F (t, t + 6) = $122.

(a) What is the spot price of the underlying asset at time t?

(b) Suppose that a three-month futures contract is trading at price

F (t, t + 3) = $119.5. Does this imply an arbitrage opportunity?

How would you take advantage of this opportunity?

8

c

° 2008, Andrew W. Lo and Jiang Wang

1.5 Options 1 QUESTIONS

1.5 Options

1. A stock price is currently $50. It is known that at the end of two

months it will be either $53 or $48. The risk-free interest rate is 10%

per annum with continuous compounding. What is the value of a two-

month Europ ean call option with a strike price of $49?

2. A stock price is currently $80. It is known that at the end of four

months it will be either $75 or $85. The risk-free interest rate is 5%

per annum with continuous compounding. What is the value of a four-

month Europ ean put option with a strike price of $80?

3. Today’s price of three traded call options on BackBay.com, all expiring

in one month, are as follows:

Strike Price Option Price

$50 $7

1

2

60 $3

70 $1

1

2

You are considering buying a “butterfly spread” consisting of the fol-

lowing p ositions:

• Buy 1 call at strike price of $50

• Sell (write) 2 calls at strike price of $60

• Buy 1 call at strike price of $70.

(a) Plot the payoff of your total position for different values of the

stock price on the maturity date.

(b) What is the dollar investment required to establish the spread?

(c) For what stock prices on the maturity date will you be making an

overall profit?

4. You are given the following prices:

Security Maturity (years) Strike Price ($)

JEK stock - - 94

Put on JEK stock 1 50 3

Put on JEK stock 1 60 5

Call on JEK 1 50 ?

Call on JEK 1 60 ?

Tbill (FV=100) 1 - 91

What is the price of the two call options?

9

c

° 2008, Andrew W. Lo and Jiang Wang

1.5 Options 1 QUESTIONS

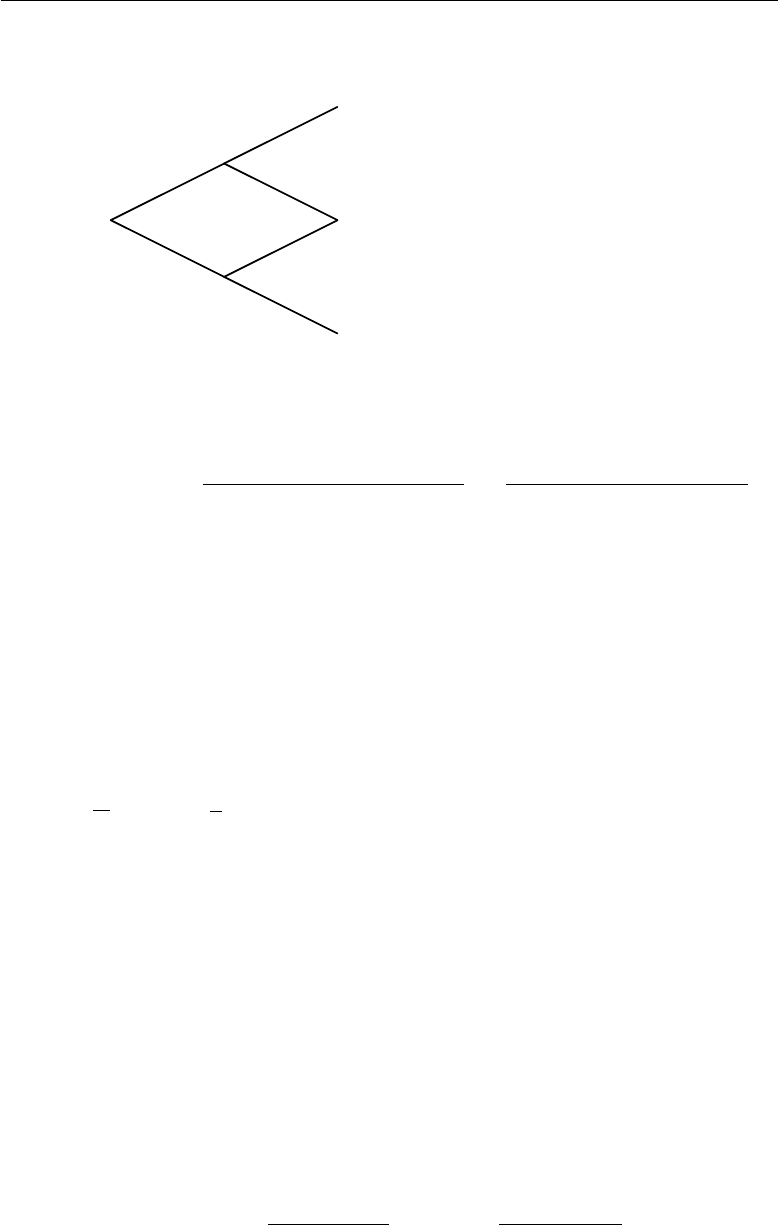

5. (a) Here are the payoff diagrams of some popular trading strategies

using just put and call options with same maturities. How would

you replicate them? Identifyfigthe number and strikes of call or

put options that have to be bought or sold in order to generate

these payoffs. (All angles are 45 degrees!)

(a)

Payoff

Stock Price

a b

Payoff

Stock Price

(b)

a

(c)

a cb

Stock Price

Figure 1: Payoff Diagrams

(b) Now suppose for institutional reasons, you are short on volatility

in this market, i.e. you will lose money if the market becomes

volatile. For example you can imagine that your are an investment

bank working on a few major M&A deals which may fall apart if

the market goes down too much or goes up too much. In either

case, you will lose money if the market becomes volatile. Explain

which if any of the above three payoffs would work well to hedge

your exp osure. What is the cost of this hedge to you?

6. A butterfly spread is a combination of option positions that involve

three strike prices. To create a butterfly spread, a trader purchases an

option with a low strike price and an option with a high strike price and

sells two options with an intermediate strike price. For this problem,

10

c

° 2008, Andrew W. Lo and Jiang Wang

1.5 Options 1 QUESTIONS

assume that the intermediate strike price is halfway between the low

and the high strike prices and that the options are European. Denote

the intermediate strike price by X, the low strike price by X − a, and

the high strike price by X + a, a > 0.

(a) Graph the payoff diagrams at maturity of the butterfly spread

in which the underlying options are call options. Holding the

intermediate strike price fixed, what happens to the payoffs as the

low and high strike price converge to the intermediate price?

(b) Suppose that a trader purchases a butterfly spread (using call

options) for which the intermediate strike price equals to today’s

stock price. Based only on this trade, what is the trader’s view of

the future direction of the market?

7. IBM shares are now traded at $80.00. The term structure of interest

rates is flat at 5%.

(a) Plot the terminal payoff from a European put option on 1 share

of IBM with a exercise price of $85 and a maturity of 3 months

(not including the price of the option).

(b) Suppose that you purchase the put option at $4.00 from the mar-

ket. Specify the ranges of IBM share price at the options maturity

date for which you will be making a net profit.

8. Suppose that after a recent news about the economy, IBM share price

remains the same, but the prices of its options shot up. How is this

possible?

9. You are given the following information. Use this information to de-

termine the unknown prices.

Table 2: Stock, Options, and T-bill prices

Secutiry Maturity (years) Strike Price($)

401 Stock - - $100

Put on 401 Stock 1 $50 $3

Put on 401 Stock 1 $60 $5

Calle on 401 Stock 1 $50 $57.50

Calle on 401 Stock 1 $60 ?

Tbill(FV=100) 1 - ?

10.

Joseph Jones, a manager at Computer Science, Inc. (CSI), received

1,000 shares of company stock as part of his compensation package.

The stock currently sells at $40 at share. Joseph would like to defer

selling the stock until the next tax year. In January, however, he will

11

c

° 2008, Andrew W. Lo and Jiang Wang

1.5 Options 1 QUESTIONS

need to sell all his holdings to provide for a down payment on his new

house. Joseph is worried about the price risk involved in keeping his

shares. At current prices, he would receive $40,000 for the stock. If

the value of his stock holdings falls below $35,000, his ability to come

up with the necessary down payment would be jeopardized. On the

other hand, if the stock value rises to $45,000, he would be able to

maintain a small cash reserve even after making the down payment.

Joseph considers three investment strategies:

(a) Strategy A is to write January call options on the CSI shares with

strike price $45. There calls are currently selling for $3 each.

(b) Strategy B is to buy January put options on CSI with strike price

$35. These options also sell for $3 each.

(c) Strategy C is to establish a zero-cost collar by writing the January

calls and buying the January puts.

Evaluation each of these strategies with respect to Joseph’s investment

goals. What are the advantages and disadvantages of each? Which

would you recommend?

11. You write a call option with strike $50 and buy a call with strike $60.

The options are on the same stock and have the same maturity date.

One of the calls sells for $3; the other sells for $9. (Assume zero interest

rate.)

(a) Draw the payoff graph for this strategy at the option maturity

date.

(b) Draw the profit graph for this strategy.

(c) What is the break-even point for this stratgy? Are you bullish or

bearish on the stock?

12. Consider an increasingly popular deposit contract with payoffs linked

to the performance on the S&P 500 Index on the U.S. stock market.

For every dollar invested in the contract, the rate of return in one year

is equal to 60% of the realized rate of return of the S&P 500 Index

during this year if this rate of return is positive; otherwise, you get

your money back. In essence, you are protected from the downside

risk of the S&P 500 Index, while you are still able to participate in the

upside potential of the stock market. The one year riskless interest rate

is 10%. For simplicity, assume that the stocks in the index do not pay

dividends.

(a) Draw a graph for the payoff one year from now for a one dollar

investment in the contract with the horizontal axis being the re-

12

c

° 2008, Andrew W. Lo and Jiang Wang

1.5 Options 1 QUESTIONS

alized rate of return on the S&P 500 Index. Also write down the

payoff symbolically.

(b) Show that the payoff one year from now for a one dollar investment

in this contract is the payoff to a portfolio of a default-free bond

and a European call option on the S&P 500 Index.

(c) Suppose that the rates of return on the S&P 500 Index can take

two possible values one year from now, 20% and -20% with prob-

abilities 60% and 40%, respectively. Do you make money or lose

money investing in this contract? If so, how much?

13. What is a lower bound for the price of 3-month call option on a non-

dividend-paying stock when the stock price is $50, the strike price is

$45, and the 3-month risk-free interest rate is 8%? Explain briefly.

14. Draw position (payoff) diagrams for each of the following trades. Each

put or call option is written on 100 shares of the same stock and has

the same 6-month maturity. The current stock price is $50 per share.

(a) Buy 100 shares, buy a put with an exercise price of $40, sell a call

with an exercise price of $60.

(b) Same as (a), except that you borrow $4902. The semi-annual

interest rate is 2%, so you will have to repay $4902×1.02 = $5000

after six months.

(c) Buy a put and a call with exercise price of $50, sell a put with

exercise price of $40, sell a call with an exercise price of $60.

15. Explain how you could generate the same payoffs as in part a of last

question without purchasing any shares.

16. Ineffable Corporations stock price is currently $100. At the end of 3

months it will be either $110 or $90.91. The risk-free interest rate is 2%

per annum. What is the value of a 3-month European call option with

a strike price of $100? Calculate your answer to this problem using

(a) replication.

(b) the risk-neutral method.

17. State whether the following statements are true or false. In each case,

provide a brief explanation.

(a) In a risk averse world, the binomial model states that, other things

being equal, the greater the probability of an up movement in the

stock price, the lower the value of a European put option.

13

c

° 2008, Andrew W. Lo and Jiang Wang

1.5 Options 1 QUESTIONS

(b) By observing the prices of call and put options on a stock, one

can recover an estimate of the expected stock return.

(c) An investor would like to purchase a European call option on an

underlying stock index with a strike price of 210 and a time to ma-

turity of 3 months, but this option is not actively traded. However,

two otherwise identical call options are traded with strike prices

of 200 and 220 respectively, hence the investor can replicate a call

with a strike price of 210 by holding a static position in the two

traded calls.

(d) In a binomial world, if a stock is more likely to go up in price than

to go down, an increase in volatility would increase the price of a

call option and reduce the price of a put option. Note that a static

position is a position that is chosen initially and not rebalanced

through time.

Draw a diagram showing an investor’s profit and loss with the terminal

stock price for a portfolio consisting of:

18. (a) One share of stock and a short position in one call option

(b) Two shares of stock and a short position in one call option

(c) One share of stock and a short position in two call options

(d) One share of stock and a short position in four call options

You should take into account the cost from purchasing the stock and

revenue from selling the calls. For simplicity ignore discounting when

combining these costs and revenues with the terminal payoff of the

portfolio. For simplicity also assume that the current stock price is

equal to the strike price, K, of the call. Denote the current call price

by c, and the terminal stock price by S

T

.

19. Stock XYZ is worth S = $80 today. Every 6 months the stock price

goes either up by u = 1.3 or down by d = 0.8. The riskless rate is 6%

APR with semiannual compounding. The stock pays no dividends.

(a) Compute the price of a European call with a maturity of 1 year

and a strike price of X = $95.

(b) Compute the price of an American call with a maturity of 1 year

and a strike price of X = $95.

(c) Compute the price of a European put with a maturity of 1 year

and a strike price of X = $95.

20. In August 1998 the Bank of Thailand was reported as offering to foreign

investors in troubled banks the opportunity to resell their shares back

to the central bank within a period of five years for the original purchase

14

c

° 2008, Andrew W. Lo and Jiang Wang

1.5 Options 1 QUESTIONS

price. “This is to guarantee that at least they will not lose any of the

money they plan to invest,” said the Deputy Governor. (The Wall

Street Journal Europe, August 6, 1998, p.20.) Suppose that(a) the

standard deviation of Thai bank shares was about 50 percent a year,

(b) the interest rate on teh Thai baht was 15%, and (c) the banks were

not expected to pay a dividend in this five-year period. How much was

this option worth? Assume an investment of 100 million baht.

21. Shares of ePet.com are traded at $60. In six months, share price could

either be $66 or $54 with probability 0.6 and 0.4, respectively. The

current 6-month risk-free rate is 6%. What is the price of a European

put on 100 ePet shares with a strike price of $64 per share? Would

your answer be different if the option is American?

22. Consider again ePet. You want to use ePet shares and the risk-free bond

to replicate a payoff in six months that equals the square of ePet’s share

price. That is, when ePet price goes up to $66, you have a payoff of

66

2

= $4, 356 and when the price goes down to $64, you have a payoff

of 54

2

= $2, 916. Describe the strategy that gives these payoffs. What

is the present value of these payoffs?

23. The price of the stock of NewWorld Chemicals Company is $80. The

standard deviation of NewWorld’s stock returns is 50%. The 1-year

interest rate is 6%.

(a) What should be the price of a call on one share of NewWorld with

a maturity of 1 year and strike price of $85? Use the Black-Scholes

formula.

(b) What should be the price of a put on one share of NewWorld with

the same maturity and strike price?

24. You are asked to price some options on ABC stock. ABC’s stock price

can go up by 15 percent every year, or down by 5 percent. Both out-

comes are equally likely. The risk free interest rate is 5 percent per year

for the next two years, and the current stock price of ABC is $100.

(a) Find the risk neutral probabilities

(b) What is the price of a European Call option on ABC, with strike

100 and maturity 2 years?

(c) Describe the strategy to replicate the payoff of the call using the

stock and the risk-free bond.

15

c

° 2008, Andrew W. Lo and Jiang Wang

1.5 Options 1 QUESTIONS

(d) What is the price of an American option with the same charac-

teristics?

25. You are asked to price some options on KYC stock. KYC’s stock price

can go up by 15 percent every year, or down by 10 percent. Both out-

comes are equally likely. The risk free rate is 5 percent, and the current

stock price of KYC is 100.

(a) Price a European Put option on KYC with maturity of 2 years

and a strike price of 100.

(b) Price an American Put option on KYC with the same character-

istics. Is the price different? Why or why not?

26. IBM is currently trading at $90.29 per share. You believe that IBM will

have an expected return of 7% with volatility of 26.1% per year, while

annual interest rates are at 0.95%. What is the price of an European

put on IBM with a strike price of $90 and maturity of 1 year?

27. Shares of Ontel will sell for either $150 or $80 three months later,

with probabilities 0.60 and 0.40, respectively. A European call with

an exercise price of $100 sells for $25 today, and an identical put sells

for $8. Both options mature in three months. What is a price of a

three-month zero-coup on bond with a face of $100?

28. 401.com’s stock is trading at $100 per share. The stock price will either

go up or go down by 25% in each of the next two years. The annual

interest rate is 5%.

(a) Determine the price of a two-year European call option with the

strike price X = $110.

(b) Determine the price of a two-year European put option with the

strike price X = $110.

(c) Verify that the put-call parity holds.

(d) Determine the price of a two-year American put option with the

strike price X = $110.

(e) What is the replicating portfolio (at every node of the tree) for

the American put option with the strike price X = $110?

29. For this problem assume that the risk-free rate of interest for one year

loans is 5%. Google stock is selling today for $500 a share. Assume

that in one year Google will either be worth $600 a share or $475 a

16

c

° 2008, Andrew W. Lo and Jiang Wang

1.5 Options 1 QUESTIONS

share and that Google will pay no dividends for at least two years.

A call option with an exercise price of $550 and one year to go until

expiration is available for Google stock. What is the value of this call

option?

30. A particular stock follows the price movement below.

$25

$29

$23

$21

$26

$24

$31

today 1-month 2-months

Figure 2: Stock Price Movement

(a) For this part, suppose the interest rate is fixed at 1% per month.

What is the price of a put option with maturity two months, and

strike of $26 ?

(b) Again, suppose the interest rate is fixed at 1% per month. What

is the price of an exotic derivative that in 2-months has a pay off

that is a function of the maximum price of the stock during the

two month period given by

max(

ˆ

S − $25, 0),

where

ˆ

S = max

0≤t≤2

S

t

.

and t is measured in months.

31. Intel stock is trading at $120 per share, and the company will not pay

any dividends over the next year. Consider an Intel European call

option and a European put option, both having an exercise price of

17

c

° 2008, Andrew W. Lo and Jiang Wang

1.5 Options 1 QUESTIONS

$124 and both maturing in exactly one year. The simple (annualized)

interest rate for borrowing and lending between now and one year from

now is 3% for each 6 month period (6.09% per year).

Assume that there are no arbitrage opportunities. Is there enough

information to determine which option has the higher market value? If

so, which option, the call or the put, has higher market value?

32. Calculate the price of a three-month European put option a non-dividend

paying stock with a strike price of $50 when the current stock price is

$50, the risk free rate is 10% per annum, and the volatility is 30% per

annum. What difference does it make to your calculations if a dividend

of $1.50 is expected in two months? Assume that the assumptions made

to derive the Black-Scholes formula are valid.

33. It is possible to buy three-month call options and three-month put

options on stock X. Both have an exercise price of $60 and both are

worth $10. Is a six-month call with an exercise price of $60 more or

less valuable than a similar six-month put?

18

c

° 2008, Andrew W. Lo and Jiang Wang

1.6 Risk & Portfolio Choice 1 QUESTIONS

1.6 Risk & Portfolio Choice

1. True or false or ”it depends”?

(a) Briefly explain or qualify your answer: diversification can reduce

risk only when asset returns are negatively correlated.

(b) If the returns on all risky assets in the world were uncorrelated

with each other, the expected return of each risky asset should be

the same.

2. True or false or ”it depends”? Optimal portfolios should exclude indi-

vidual assets whose expected return and risk (measured by its standard

deviation) are dominated by other available assets.

3. Is the following statement true or false? Explain. As more securities

are added to a portfolio, total risk would typically be expected to fall

at a decreasing rate.

4. You need to invest $10M in two assets: a risk-free asset with an ex-

pected return of 5% and a risky asset with an expected return of 12%

and a standard deviation of 40%. You face a cap of 30% on the port-

folio’s standard deviation (the “risk budget”). What is the maximum

expected return you can achieve on your portfolio?

5. Are the following statements true, false or uncertain? Briefly explain

your answer.

(a) Diversification over a large number of assets completely eliminates

risk.

(b) Diversification works only when asset returns are uncorrelated.

(c) A stock with high standard deviation may contribute less to port-

folio risk than a stock with lower standard deviation.

(d) Diversification reduces the expected return on the portfolio as its

risk decreases.

6. Are the following statements true or false? Give brief but precise ex-

planations for your answers.

(a) Stock A has exp ected return 10% and standard deviation 15%,

and stock B has expected return 12% and standard deviation 13%.

Then, no investor will buy stock A.

(b) Diversification means that the equally weighted portfolio is opti-

mal.

7. Which statement about portfolio diversification is correct?

19

c

° 2008, Andrew W. Lo and Jiang Wang

1.6 Risk & Portfolio Choice 1 QUESTIONS

(a) Proper diversification can reduce or eliminate systematic risk.

(b) Diversification reduces the portfolio’s expected return because it

reduces the portfolio’s total risk.

(c) As more securities are added to a portfolio, total risk would typi-

cally be exp ected to fall at a decreasing rate.

(d) The risk-reducing benefits of diversification do not occur mean-

ingfully until at least 30 individual securities are included in the

portfolio.

8. Which of the following portfolios can not be on the Markowitz efficient

frontier? Explain briefly.

Portfolio Exp ected Return Standard Deviation

Q 10% 15%

R 10.5% 16.5%

S 11.5% 18.5%

T 12.5% 20%

9. You have decided to invest all your wealth in two mutual funds: A and

B. Their returns and risks are as follows:

• the mean returns are ˜r

A

= 15% and ˜r

B

= 11%

• the covariance matrix is

r

A

r

B

r

A

.04 .025

r

B

.025 .032

You want your total portfolio to yield a return of 12%. What pro-

portions of your wealth should you invest in A and B? What is the

standard deviation of the return on your portfolio?

10. There are only two securities (A and B, no risk free asset) in the market.

Expected returns and standard deviations are as follows:

Security Exp ected return standard Deviation

Stock A 25% 20%

Stock B 15% 25%

(a) The correlation between stocks A and B is 0.8. Compute the

expected return and standard deviation of a portfolio that has 0%

of A, 10% of A, 20% of A, etc, until 100% of A. Plot the portfolio

frontier formed by these portfolios.

20

c

° 2008, Andrew W. Lo and Jiang Wang

1.6 Risk & Portfolio Choice 1 QUESTIONS

(b) Repeat the previous question, assuming that the correlation is

−0.8.

(c) Explain intuitively why the portfolio frontier is different in the

two cases.

11. Stock A and B have the following characteristics:

E(r) σ

A 8% 20%

B 8% 40%

Their correlation is 0. The risk-free interest rate is 2%.

(a) Consider a portfolio, P, with 90% in stock A and 10% in the risk-

free asset. What is the mean and standard deviation of portfolio

P’s return?

(b) Consider another portfolio, Q, which consists of 80% of stock A

and 20% of stock B. What is the mean and standard deviation of

portfolio Q’s return?

(c) You need to choose a portfolio to invest all your wealth in. Be-

tween portfolio P and Q, which one is better? Explain why.

(d) Given that stock A dominates stock B (A has the same mean but

lower risk), explain why you ever include stock B in your portfolio.

12. You can form a portfolio of two assets, A and B, whose returns have

the following characteristics:

Stock E[R] Standard Deviation Correlation

A 0.10 0.20

0.5

B 0.15 0.40

If you demand an expected return of 12%, what are the portfolio

weights? What is the portfolio’s standard deviation?

13. Your have decided to invest all your wealth in two mutual funds: A

and B. Their returns are characterized as follows:

• the mean returns are ¯r

A

= 20% and ¯r

B

= 15%

• the covariance matrix is

r

A

r

B

r

A

0.3600 0.0840

r

B

0.0840 0.1225

21

c

° 2008, Andrew W. Lo and Jiang Wang

1.6 Risk & Portfolio Choice 1 QUESTIONS

You want your total portfolio to yield a return of 18%. What proportion

of your wealth should you invest in fund A and B? What is the standard

deviation of the return on your portfolio?

14. In addition to the fund A and B in the previous question, now you

decide to include fund C to your portfolio. Its expected return is ¯r

C

=

10%. The covariance matrix of the three funds is

r

A

r

B

r

C

r

A

0.3600 0.0840 0.1050

r

B

0.0840 0.1225 0.0700

r

C

0.1050 0.0700 0.0625

Your portfolio now consists of fund A, B and C. You would like to

have an expected return of 16% on your portfolio and a minimum risk

(measured by standard deviation of the return). What portfolio should

you hold? What is the return standard deviation of your portfolio?

(Hint: You would need to use Excel Solver or some other optimization

software to solve the optimal portfolio.)

15. You can only invest in two securities: ABC and XYZ. The correlation

between the returns of ABC and XYZ is 0.2. Expected returns and

standard deviations are as follows:

Security E[R] σ(R)

ABC 20% 20%

XYZ 15% 25%

a) It seems that ABC dominates XYZ in that it has a higher expected

return and lower standard deviation. Would anyone ever invest in

XYZ? Why?

b) What is the expected return and standard deviation of a portfo-

lio that invests 60% in ABC and 40% in XYZ?

c) Suppose instead that you want your portfolio to have an expected

return of 19.5%. What portfolio weights do you select now? What is

the standard deviation of this portfolio?

16. You have the same data as the previous question. In addition, you

have a risk-free security with a guaranteed return of 5%. The tangency

portfolio has an expected return of ?? and standard deviation of ??.

(a) What weights are placed on ABC and XYZ in the tangency port-

folio?

22

c

° 2008, Andrew W. Lo and Jiang Wang

1.6 Risk & Portfolio Choice 1 QUESTIONS

(b) What portfolio weights will you choose for the risk-free asset and

the tangency portfolio to get an expected return of 19.5%.

(c) Compare this portfolio with the one you obtained in (c) of the

previous question. Comment.

17. Calculate the expected return and standard deviation of a portfolio of

stocks A, B and C. Assume an equal investment in each stock.

Expected Return Standard Deviation

Correlations

A B C

A 11% 30% 1.0 .3 .15

B 14.5% 45% .3 1.0 .45

C 9% 30% .15 .45 1.0

18. Your employer offers two funds for your pension plan, a money market

fund and an S&P 500 index fund. The money market fund holds 3-

month Treasury bills, which currently offer a 3% safe return per year.

The S&P 500 index fund offers an expected return of 10% per year

with a standard deviation of 20%.

(a) You want to achieve an expected return of 8% per year for your

portfolio. What should be the composition of your portfolio?

What is the standard deviation of its returns?

(b) Now your employer adds an emerging-market fund to the two ex-

isting funds. The emerging-market fund offers an expected return

of 10% per year, the same as the S&P 500 index fund, but with a

standard deviation of 30%, higher than the S&P 500 index fund.

Would you consider including the emerging-market fund as part

of your p ortfolio? Explain.

(c) The correlation between the S&P 500 index fund and the emerging-

market fund is zero. Consider portfolio A, which consists of 80%

in the S&P index fund and 20% in the emerging-market fund.

Calculate portfolio A’s expected return and standard deviation.

(d) If you mix portfolio A with the money-market fund to achieve an

expected return of 8%, is it better than the portfolio in part (a)

of this question? Explain.

19. You are given data on the following stocks:

Stock E[R] ← V[R] → Price Mkt. Cap.

A 0.10 0.0625 0.0437 0.0525 $50 $105M

B 0.15 - 0.1225 0.0420 $30 $40M

C 0.20 - - 0.0900 $27 $75M

23

c

° 2008, Andrew W. Lo and Jiang Wang

1.6 Risk & Portfolio Choice 1 QUESTIONS

a) Compute the expected return and variance of an equally weighted

portfolio (i.e. weights of 1/3 on each of the stocks).

Consider alternative portfolios formed using assets A, B, and C. For

instance, a value-weighted portfolio places weights on each assets in

proportion to their market capitalizations. The S&P500 index is an ex-

ample of a value-weighted portfolio. A price-weighted portfolio places

weights in proportion to prices. The Dow Jones is an example of a

price-weighted portfolio.

b) What are the expected returns and variance of a value-weighted

portfolio.

c) What are the expected returns and variance of a price-weighted

portfolio.

20. Your current portfolio consists of three assets, the common stock of

IBM and GM combined with an investment in the riskless asset. You

know the following about the stocks (ρ

i,j

denotes the correlation be-

tween asset i and asset j, and M denotes the market portfolio):

ρ

IBM,M

= 0.60 ρ

GM,M

= 0.80

σ

2

IBM

= 0.0900 σ

2

GM

= 0.0625

You also have the following data about the market portfolio M and the

riskless asset F:

¯r

M

= 0.13 r

F

= 0.04

σ

2

M

= 0.04

Suppose that individuals can borrow and lend at r

F

and that the Capi-

tal Asset Pricing Model (CAPM) describes expected returns on assets.

You have $200, 000 invested in IBM, $200,000 invested in GM, and

$100,000 invested in the riskless asset.

(a) What are the expected rates of return on IBM stock and GM

stock?

(b) Assume that the correlation between IBM and GM, ρ

IBM,GM

, is

0.40. What is the variance of your portfolio? What is its beta,

β

p,M

?

(c) Suppose that you can also invest in the market portfolio. Find

an efficient portfolio that has the same standard deviation as your

portfolio, but has the highest expected rate of return possible.

What is the expected rate of return on this portfolio?

24

c

° 2008, Andrew W. Lo and Jiang Wang

1.6 Risk & Portfolio Choice 1 QUESTIONS

21. There are three assets, A, B and C, where A is the market portfolio and

C is the risk-free asset. The return on the market has a mean of 12%

and a standard deviation of 20%. The risk-free asset yields a return of

4%. Asset B is a risky asset whose return has a standard deviation of

40% and a market beta of 1. Assume that the CAPM holds.

(a) Compute the expected return of asset B and its covariances with

asset A (the market portfolio) and asset C (the risk-free asset),

respectively.

(b) Consider a portfolio of the two risky assets, A and B, with weight

w in asset A (the market portfolio) and 1−w in asset B. Compute

the expected return and return standard deviation of the portfolio

with w being 0, 1/2, and 1, respectively, and enter them into the

following table:

Portfolio weight w 0 1/2 1

Expected return

Standard deviation

(c) Can you rank the three portfolios in the question above? Explain.

(d) Consider a portfolio with equal weights in asset B and C (the risk-

free asset). Denote this portfolio as asset D. Compute the return

standard deviation and expected return of asset D.

(e) Consider a portfolio of asset A (the market portfolio) and C. Find

the portfolio weight such that its return standard deviation is the

same as that of asset D in Question (d). What is the expected

return of this portfolio?

(f) What can you say about the mean-variance efficiency of asset A,

B and C (i.e., are they efficient portfolios)? Explain.

(g) Construct an efficient portfolio from the assets A, B and C with

an expected return of 10%.

22. Assume that an investor must put all of her money in the following

four stocks.

Expected Return Standard Deviation

Correlations

A B C D

A 11% 25% 1.0 .3 .15 .4

B 14.5% 35% .3 1.0 .45 .2

C 9% 30% .15 .45 1.0 .25

D 11.5% 32% .4 .2 .25 1.0

25

c

° 2008, Andrew W. Lo and Jiang Wang

1.6 Risk & Portfolio Choice 1 QUESTIONS

(a) What is the expected return and standard duration of an equally

weighted portfolio of the four stocks?

(b) Calculate the mean-variance efficient portfolios that can be con-

structed from the four stocks. (Hint: use Excel Solver)

(c) Assume the investor can borrow or lend at a 5% risk-free rate.

What is the best portfolio of the four stocks?

23. Assets X, Y, and Z have the following characteristics:

Asset Exp. Ret. (¯r) Std. Dev. ( σ)

X 15% 20%

Y 10% 15%

Z 10% 15%

Correlation X Y Z

X 1 0.7 0.3

Y 1 0.2

Z 1

Consider the portfolio frontier of the three assets. Without solving for

the portfolio weights, answer the following questions:

(a) The frontier portfolio with mean 12% has higher weight on

i. Y

ii. Z

(b) The frontier portfolio with mean 9% has higher weight on

i. Y

ii. Z

(c) The frontier portfolio with mean 20% has higher weight on

i. Y

ii. Z

Explain the intuition for your results.

24. Consider a sample of 1000 randomly selected stocks, and assume for

simplicity that each stock has a standard deviation of 35%. The corre-

lation coefficient between each pair of stocks is .3. What is the standard

deviation of an equal-weighted portfolio of 10 stocks? 100 stocks? 1000

stocks?

25. Assume that you can borrow and lend at a riskless rate of 5% and that

the tangency portfolio of risky assets has an exp ected return of 13%

and a standard deviation of return of 16%.

26

c

° 2008, Andrew W. Lo and Jiang Wang

1.6 Risk & Portfolio Choice 1 QUESTIONS

(a) What is the highest level of expected return that can be obtained

if you are willing to take on a standard deviation of returns that

is at most equal to 24%? Answer and explain below.

(b) What is the fraction of your wealth (in percent) invested in the

riskless asset in the portfolio you found in part (a) (the mean-

variance efficient portfolio with a standard deviation of 24%)?

What is the fraction invested in the tangency portfolio of risky

assets?

26. For this problem assume that it is possible to borrow and lend risklessly

at a rate of 4%. Also assume that the expected return on the tangency

(i.e., the optimal) portfolio composed only of risky assets is 13% with

a standard deviation of 18%. Below we list 6 pairs of expected return

and standard deviation combinations. For each pair determine whether

or not the pair is feasible. If it is feasible, then there is at least one

investment that can be made using risky assets and riskless borrowing

or lending that produces this level of expected return and standard

deviation. Then, if the pair is feasible, determine whether it is efficient

or not. It is efficient if the expected return is the highest level that can

be obtained for the associated level of standard deviation.

Pair Standard Deviation Exp ected Return

a 20.00% 24.75%

b 12.00% 18.00%

c 30.00% 19.00%

d 60.00% 50.00%

e 10.00% 4.00%

f 45.00% 56.50%

27. Parmacheenee Belle’s entire common stock portfolio ($500,000) is al-

lotted to an index fund tracking the Standard & Poors 500 index. The

expected rate of return on the index is 9.5% and the standard deviation

is 18% per year. The one-year risk-free rate is 2.0%.

Now Ms. Belle receives a strongly favorable security analyst’s report on

Mycronics Corp. The analyst projects a return of 25%. Myroncis has

a high volatility (40% annual standard deviation) but its correlation

coefficient with the S&P 500 is only .3.

Assume the return in the analyst’s report is an unbiased forecast.

Should Ms. Belle sell part of her index fund holdings and invest in

Myronics? If so, how much? Note: Ms. Belle can also lend or borrow

at the 2.0% risk-free rate.

28. Samantha Darling’s entire common stock portfolio ($100,000) is allot-

ted to an index fund tracking the Standard & Poors 500 index. The

27

c

° 2008, Andrew W. Lo and Jiang Wang

1.6 Risk & Portfolio Choice 1 QUESTIONS

expected rate of return on the index is 12% and the standard deviation

is 16% per year. The one-year risk-free rate is 5.5%.

Now Samantha receives a strongly favorable security analyst’s report

on e.Coli Corp. The analyst projects a return for e.Coli of 25%. e.Coli

has a high volatility (50% annual standard deviation) but its correlation

coefficient with the S&P 500 is only .4.

Assume the analyst’s report is accurate. Should Samantha sell part of

her index fund holdings and invest in e.Coli? If so, now much? Note:

Samantha can also lend or borrow at the 5.5% risk-free rate.

29. You are a salesman/investment advisor working for a major investment

bank. Whenever clients contact you with money to invest, your job is

to help them find an appropriate mutual fund to invest in given their

financial position. The available investments are:

Fund E[R] σ(R)

A 10% 15%

B 20% 45%

C 20% 55%

Assume throughout this problem that you only recommend one of the

three funds to your clients (possibly a different recommendation for

different clients though).

a) Would you recommend investment C to someone who comes to you

with all his investment funds? Explain.

b) Which investment would you recommend to Keith Richards, the

really, really old rock star from the Rolling Stones? Assume he invests

all his wealth in your particular recommendation.

c) Might your answer to b) change if Keith invests only half his wealth

in your particular recommendation? If so, under what circumstances?

30. Sarah runs an investment consulting business offering advice to clients

on portfolio choices, using what she has learned in 15.401. Her analysis

shows that the efficient frontier of risky assets can be obtained by mix-

ing two portfolios, a portfolio of ”large cap” stocks (L) and a portfolio

of ”small cap” stocks (S). In addition, she can also invest in riskless

T-Bills (F).

For a very risk-averse retiree, Sarah has recommended the following

portfolio: 70% in F, 20% in L and 10% in S. For a young, less risk-

averse executive, however, Sarah recommends only 10% in F and the

28

c

° 2008, Andrew W. Lo and Jiang Wang

1.6 Risk & Portfolio Choice 1 QUESTIONS

rest in the two risky portfolios.

Assume that Sarah has chosen the optimal portfolios for both the old

retiree and the young executive. What are the weights for the young

executive on the ”large cap” and ”small cap” portfolios, respectively?

(Hint: The tangent portfolio should a combination of portfolios L and

S.)

31. Which of the following common stock portfolios is best for a conserva-

tive, risk-averse investor? Explain briefly.

Expected Expected Standard Deviation

Return Risk Premium of Return

Portfolio A 19% 13% 20%

Portfolio B 16% 10% 16%

Portfolio C 13% 7% 12.5%

Note: the risk premium is calculated by subtracting a 6% Treasury

bill rate from the expected rate of return. The investor can also buy

Treasury bills.

32. Suppose the overall stock market is divided in four asset classes: large-

cap growth stocks (LGR, 40% of the market), large-cap income stocks

(LINC, 35% of the market), small-cap growth stocks (SMGR, 15% of

the market) and small-cap income sto cks (SMINC, 10% of the market).

Forecasted returns, standard deviations (σ) and correlation coefficients

for these asset classes are given on the table below. You can borrow or

lend at the risk-free interest rate of 5%. You have $1 million to invest in

some combination of the four asset classes. (You can buy index funds

or exchange traded portfolios tracking the asset classes.)

LGR LINC SMGR SMINC

% of market 0.40 0.35 0.15 0.10

¯r 0.1438 0.1092 0.1329 0.0931

σ 0.28 0.20 0.30 0.22

Correlations:

LGR LINC SMGR SMINC

LGR 1 0.65 0.70 0.30

LINC 0.65 1 0.40 0.55

SMGR 0.70 0.40 1 0.45

SMINC 0.30 0.55 0.45 1

29

c

° 2008, Andrew W. Lo and Jiang Wang

1.6 Risk & Portfolio Choice 1 QUESTIONS

(a) What are the expected rate of return and standard deviation of

the market portfolio? What is the market’s Sharpe ratio (the ratio

of expected risk premium to standard deviation)?

(b) Can you improve the portfolio’s Sharpe ratio by investing more in

any of the asset classes? (Hint: Analyze a two-asset portfolio, with

the market as one asset and a particular asset class as the other.

If you sell some of the market portfolio and put the proceeds in

that asset class, you end up over-weighting the asset class.)

30

c

° 2008, Andrew W. Lo and Jiang Wang

1.7 CAPM 1 QUESTIONS

1.7 CAPM

1. What is the beta of a portfolio with E(r

p

) = 18%, if r

f

= 6% and

E(r

M

) = 14%?

2. You are a consultant to a large manufacturing corporation that is con-

sidering a project with the following net after-tax cash flows (in millions

of dollars):

Years from Now After-Tax Cash Flow

0 −40

1 − 10 15

The project’s beta is 1.8. Assuming that r

f

= 8% and E(r

M

) = 16%,

what is the net present value of the project? What is the highest

possible beta estimate for the project before its NPV becomes negative?

3. Are the following true or false?

(a) Stocks with a beta of zero offer an expected rate of return of zero.

(b) The CAPM implies that investors require a higher return to hold

highly volatile securities.

(c) You can construct a portfolio with a b eta of 0.75 by investing 0.75

of the investment budget in bills and the remainder in the market

portfolio.

4. Assume that the risk-free rate of interest is 6% and the expected rate

of return on the market is 16%. A share of stock sells for $50 today.

It will pay a dividend of $6 per share at the end of the year. Its beta

is 1.2. What do investors expect the stock to sell for at the end of the

year?

5. Assume that the risk-free rate of interest is 6% and the expected rate

of return on the market is 16%. A stock has an expected rate of return

of 4%. What is its beta? Why would anyone consider buying this risky

asset which provides an expected return less than the risk-free rate?

6. In 1997 the rate of return on short-term government securities (per-

ceived to be risk-free) was about 5%. Suppose the expected rate of

return required by the market for a portfolio with a beta measure of 1

is 12%. According to the capital asset pricing model (security market

line):

(a) What is the expected rate of return on the market portfolio?

(b) What would be the expected rate of return on a stock with β = 0?

31

c

° 2008, Andrew W. Lo and Jiang Wang

1.7 CAPM 1 QUESTIONS

(c) Suppose you consider buying a share of stock at $40. The stock is

expected to pay $3 dividends next year and you expect it to sell

then for $41. The stock risk has b een evaluated by β = −.5. Is

the stock overpriced or underpriced?

7. True or False?

(a) CAPM says that all risky assets must have positive risk premium.

(b) The expected return on an investment with a beta of 2.0 is twice

as high as the expected return on the market.

(c) If a stock lies below the security market line, it is under valued.

8. If we regress the stocks’ average risk premium (return minus the risk-

free rate) on their betas, what should be the slope and the intercept

according to the CAPM?

9. If we regress a stock’s risk premium on the risk premium of the market

portfolio, what should be the slope and the intercept according to the

CAPM?

10. The risk-free rate is 5%, the expected return on the market portfolio is

14%, and the standard deviation of the return on the market portfolio

is 25%. Consider a portfolio with expected return of 16% and assume

that it is on the efficient frontier.

(a) What is the beta of this portfolio?

(b) What is the standard deviation of its return?

(c) What is its correlation with the market return?

11. Your future father-in-law is 60 years old. He shows you his portfolio:

Assets Holdings

Cash $ 50,000

S&P 500 Index Fund 100,000

Analog Devices Inc. 200,000

He asks you to forecast how much the portfolio will be worth in 5 years

when he retires. The risk-free rate is 6% per year, the average return

on the market portfolio is 12%, the beta of the S&P index is 1.0, and

the beta of Analog Devices is 1.5.

(a) What is the expected rate of return on the portfolio, assuming the

CAPM holds?

(b) What is the forecasted portfolio value after 5 years?

32

c

° 2008, Andrew W. Lo and Jiang Wang

1.7 CAPM 1 QUESTIONS

(c) Your future father-in-law is not impressed with this CAPM “the-

ory” since his portfolio has done much better than your forecasted

return over the past five years. What would you say about that?

12. Integral Industries, Inc. (II I) has three subsidiaries, A, B, and C. You

are negotiating to buy subsidiary C. Subsidiary A and B each con-

tribute to 40% of III’s market value and have betas of 0.8 and 1.4,

respectively. The company as a whole has a beta of 1.0. What is the

beta of subsidiary C? If you end up buying it, what would be C’s oppor-

tunity cost of capital? The current risk-free rate is 6% and the market

risk premium is 6%.

13. Stock 1 and 2 have the same beta of 0.8. But stock 1’s return has a

standard deviation of 40% and stock 2 has a standard deviation of 60%.

How would you compare the risk of these two stocks? Which one do

you think should have the higher expected returns? Explain briefly.

14. Stock A has a beta of 0.6 and stock B has a beta of 1.2. They both

have a return standard deviation of 40% and the market portfolio has a

return standard deviation of 25%. What fractions of the total variances

of the two stocks’ returns are market risks?

15. Five years of monthly risk premiums give the following statistics for

Ampersand Electric common stock (risk premium = rate of return -

risk-free rate):

• α is 0.4% per month, with a standard error of 1.2%

• β is 1.2, with a standard error of 0.27

• R

2

is 0.30

• σ is 7.2% per month.

(a) What does α measure? What role does it play in the CAPM?

Does a positive α indicate a higher-than-normal expected return?

(b) What does R

2

measure? Would a higher R

2

increase your confi-

dence in the estimated β?

Briefly explain your answers.

16. Consider three stocks: Q, R and S.

Beta STD (annual) Forecast for Nov 2008

Dividend Stock Price

Q 0.45 35% $0.50 $45

R 1.45 40% 0 $75

S -0.20 40% $1.00 $20

33

c

° 2008, Andrew W. Lo and Jiang Wang

1.7 CAPM 1 QUESTIONS

Use a risk-free rate of 2.0% and an expected market return of 9.5%. The

market’s standard deviation is 18%. Assume that the next dividend will

be paid after one year, at t = 1.

(a) According to the CAPM, what is the expected rate of return of

each sto ck?

(b) What should today’s price be for each stock, assuming the CAPM

is correct?

17. Assume the Fama-French 3-factor APT holds with the factor risk pre-

miums given in BM Table 8.5, p. 209. What are the expected rates

of return for stocks Q, R and S in the previous question? The factor

sensitivities are:

b

market

b

size

b

book−to−mark et

Q 0.45 0.05 0.14

R 1.45 -0.33 -0.22

S -0.20 1.21 0.64

18. It is November, 2007. The following variance-covariance matrix, for

the market (S&P 500) and stocks T and U, is based on monthly data

from November 2002 to October 2007. Assume T and U are included

in the S&P 500. The betas for T and U are T = 0.727 and U = 0.75.

S&P 500 T U

S&P 500 0.0256 0.0186 0.0192

T 0.0186 0.1225 0.0262

U 0.0192 0.0262 0.0900

Average monthly risk premiums from 2002 to 2007 were:

S&P 500 : 1.0%

T : 0.6%

U : 1.1%

Assume the CAPM is correct, and that the expected future market

risk premium is 0.6% per month. The risk-free interest rate is 0.3% per

month.

(a) What were the alpha’s for stocks T and U over the last 60 months?

(b) What are the expected future rates of return for T and U?

34

c

° 2008, Andrew W. Lo and Jiang Wang

1.7 CAPM 1 QUESTIONS

(c) What are the optimal portfolio weights for the S&P 500, T and

U? Explain.

19. CML and SML: Using the properties of the capital market line

(CML) and the security market line (SML), determine which of the

following scenarios are consistent or inconsistent with the CAPM. Ex-

plain your answers. Let A and B denote arbitrary securities while F

and M represent the riskless asset and the market portfolio respectively.

(a) Scenario I:

Security E[R] β

A 25% 0.8

B 15% 1.2

(b) Scenario II:

Security E[R] σ(R)

A 25% 30%

M 15% 30%

(c) Scenario III:

Security E[R] σ(R)

A 25% 55%

F 5% 0%

M 15% 30%

(d) Scenario IV:

Security E[R] β

A 20% 1.5

F 5% 0

M 15% 1.0

(e) Scenario V:

Security E[R] β

A 35% 2.0

M 15% 1.0

20. True/False/Depends Questions: Please include brief explanations

in your resp onses:

(a) The average return on stocks in the US over the past 30 years has

been 12% annually. You find two portfolios, one with an expected

return of 14% and another with an expected return of 19%. This

contradicts the CAPM.

35

c

° 2008, Andrew W. Lo and Jiang Wang

1.7 CAPM 1 QUESTIONS

30. True or False. Briefly explain.

(a) The capital asset pricing model assumes that all investors have

the same information and are willing to hold the market portfolio.

(b) Over the long run, average returns on low-beta stocks have been

less than predicted by the capital asset pricing model.

31. Suppose that the actual rate of return on the S&P 500 index from

Decemb er 17, 2001 (today) to December 17, 2002 (12 months hence)

is 9.0%, including dividends paid by companies in the index. You are

given the following information about the p erformance of mutual funds

X, Y and Z. Each mutual fund invests only in common stocks.

Fund (manager) Rate of return Alpha (SE) Beta (SE) R

2

X (Gladys Friday) 9.8% +.48% (1.0%) 1.05 (.05) .92

Y (Gene Po ol) 9.0% −.65% (3.0%) 1.10 (.07) .88

Z (Hugh Betcha) 13.4% +.50% (3.1%) 1.60 (.09) .65

Alphas and betas are estimated from 52 weekly returns from December

2001 to December 2002. Returns and alphas are given above as annual

percentage returns. SE means standard error. The start-of-year risk-

free rate is 2.5%.

Based on these statistics, what can you say about the investment strat-

egy and performance of each of the three managers? Explain. Consider

risk as well as return before answering.

32. Your company offers three funds to its employees for their p ensions:

a money-market fund, an S&P 500 index fund and a new-economy

equity fund. You need to form a portfolio from these funds for your

own p ension investments.

The money-market fund is invested in 3-month Treasury bills, now with

a risk-free return of 1.5% per annum. The index fund gives a premium

of 8% and a standard deviation of 20% per annum. The new-economy

fund’s return can be described by the following equation:

r

t

− r

F

= α + β(r

Mt

− r

F

) + e

t

where r

t

and r

Mt

are the fund and market returns, r

F

is the risk-free

return, α is a constant, and e

t

is the part of the fund’s returns not

explained by the market. The performance of the fund over the last 60

months gives

39

c

° 2008, Andrew W. Lo and Jiang Wang

1.7 CAPM 1 QUESTIONS

• α = 0.0

• β = 1.2

• R

2

= 0.75 (proportion of the variance of the fund’s return ex-

plained by the market return).

(a) Compute the expected return of the new-economy fund using

CAPM. Use reasonable estimates for the market return and the

risk-free return.

(b) If CAPM holds, what is the optimal portfolio to achieve an ex-

pected return of 8% per annum.

(c) If instead, the estimate of α is 0.0050 (0.5% per month) with a

standard error of 0.0015. Without doing any calculations, discuss

how this may affect your portfolio.

33. Two mutual fund managers are being evaluated for their performance in

the last ten years. One of them, Mr. Hare, has achieved an eye-popping

34% annual average return; the other, Ms. Tortoise, has obtained a

modest 12% annual average return. On closer examination of their

portfolios, it is found that Mr. Hare always bet on risky Argentinian

stocks (whose beta is 4), whereas Ms. Tortoise always invested in

conservative technology firms like IBM (whose beta is

(a) If the risk-free return was 3% every year and the expected mar-

ket return was 11% every year, who should get the higher bonus?

Why? (Credit only if reasoning is correct.)

(b) If the risk-free return was 7% every year and the expected market

return was 13% every year, who should get the higher bonus?

Why? (Credit only if reasoning is correct)

34. True or false. Explain briefly

By the CAPM, stocks with the same beta have the same variance.

35. True or false. Explain briefly

If CAPM holds, α should be zero for all assets.

36. Does the CAPM provide a good explanation of past average rates of

return? How would you (briefly) summarize the evidence?

37. True or false. Explain briefly.

40

c

° 2008, Andrew W. Lo and Jiang Wang

1.7 CAPM 1 QUESTIONS

(a) The Sharp e ratio equals average return divided by standard devi-

ation of return.

(b) The average beta of all the assets in the market is 1.

38. Assume that you can borrow and lend at a riskless rate of 5% and that

the tangency portfolio of risky assets has an exp ected return of 13%

and a standard deviation of return of 16%.

(a) What is the highest level of expected return that can be obtained

if you are willing to take on a standard deviation of returns that

is at most equal to 24%? Answer and explain below.

(b) What is the fraction of your wealth (in percent) invested in the

riskless asset in the portfolio you found in part (a) (the mean-

variance efficient portfolio with a standard deviation of 24%)?

What is the fraction invested in the tangency portfolio of risky

assets?

41

c

° 2008, Andrew W. Lo and Jiang Wang

1.8 Capital Budgeting 1 QUESTIONS

1.8 Capital Budgeting

1. Table A gives investments, NPVs, IRRs and the first three years’ cash

flow for several capital investment projects. Each project’s cash flows

continue for several more years, longer for some projects than others.

The cost of capital is 12% for all projects.

Table A (figures in millions).

Project Invest in 2000 C

1

C

2

C

3

NPV IRR

A 100 20 20 20 57 17.8

B 200 0 20 40 64 14.5

C 50 20 20 20 41 37.8

D 75 -10 10 30 0 12

E 30 -10 5 7 -3 11

F 10 3 4 5 5.5 30.2

Projects A and B are mutually exclusive - your firm can take only one.

The projects are discrete - you cannot make partial investments in any

project.

(a) Suppose the firm rejects all projects with payback periods greater

than 3 years. What is the NPV from following this policy?

(b) A manager defends the decisions in part a as a way to avoid taking

on risky projects. Does this defense make sense?

(c) Which project would you choose, A or B?

(d) Suppose that the firm now identifies a new project AA with ex-

actly the same cash flows, NPV and IRR as project A. Does the

opportunity to invest in AA change your answer to part c?

(e) Suppose the firm has only $200 million to invest - a fixed capital

constraint. Which projects would you undertake? (Ignore project

AA.)

(f) Now the firm negotiates a line of credit that allows it to borrow

up to $100 million at 8%. Would access to additional debt capital

at a cost of 8% change your answers to questions c, d or e?

Explain each answer briefly.

2. You own three oil wells in Vidalia, Texas. They are expected to produce

7,000 barrels next year in total, but production is declining by 6 p ercent

every year after that. Fortunately, you have a contract fixing the selling

price at $15 per barrel for the next 12 years. What is the present value

of the revenues from the well during the remaining life of the contract?

Assume a discount rate of 8 percent.

42

c

° 2008, Andrew W. Lo and Jiang Wang

1.8 Capital Budgeting 1 QUESTIONS

3. Your company’s CFO has budgeted $18 million for capital expenditures

during 2000 by your division. Unfortunately the division has good

opportunities to invest much more than $18 million. The cost of capital

is 12%.

Project Investment in 2000 NPV IRR

Q 10.5 5.5 15

R 2.0 0.5 18

S 6.0 2.5 25

T 7.5 2.0 30

U 1.5 1.0 26

V 3.0 1.0 20

Assume the $18 million budget can not be increased. Which projects

should be undertaken?

4. The DEF Corporation is trying to decide whether to undertake an

expansion of its production facilities. The expansion will cost $8.5

million, to be paid immediately. After tax cash flows generated by the

expansion are projected to be $1 million next year, and will be growing

indefinitely with inflation at 2.5% per year. Assume that the CAPM

holds, the beta of DEF assets is 1.2, the riskless rate is 5% per year

(and the yield curve is flat at this rate) and that the expected return

on the market portfolio is 12%. Should DEF undertake the expansion?

5. You have developed the technology to use gold to produce high capacity

fiber optic switches. The technology has cost $ 5 million to develop.

You need $50 million of initial capital investment to start production.

Sales of the switch sales will be $20 million p er year for the next 5 years

and then drop to zero. The main cost of production is gold. Each year,

you need 20,000 ounces of gold. Gold is currently selling for $250 per

ounce. Your supplier thinks that the gold price will appreciated at 5%

per year for the next 5 years. The cost of capital is 10% for the fiber-

optics business. The tax rate is 35%. The capital investment can be

depreciated linearly over the next 5 years.

(a) Calculate the after-tax cash flows of the project.

(b) Should you take the project?

6. Your company considers a new investment project, which lasts for three

years. The project requires a purchase of a new machine, which costs

$600,000. This initial investment can be depreciated to zero over the

next three years according to a straight line depreciation rule. The

machine has no salvage value at the end. Operating revenue is projected

to be $400,000 per year. Operating costs for raw materials are $100,000

43

c

° 2008, Andrew W. Lo and Jiang Wang

1.8 Capital Budgeting 1 QUESTIONS

per year. The above data is summarized in the following table (in

thousands of dollars):

Capital expenditure 600

Depreciation 200 200 200

Operating revenue 400 400 400

Operating cost 100 100 100

The corporate tax rate is 30% and the risk-adjusted discount rate is

10%.

(a) Compute after-tax cash flows every year.

(b) Should we take the project and why?

(c) Suppose that you need to purchase an inventory of raw materials

now (year 0) instead of year by year in the next three years. This

will require an initial expense of $300,000 in inventory, which will

then be depleted, by equal amount every year in the next three

years. How would your answers to the above questions change?

7. Halliburton is considering for a two-year project. The project requires

an initial capital expenditure of $100 million (in year 0), which can

be depreciated linearly to zero in the next two years. It generates a

revenue of $80 million and a cost of $25 million per year for the next

two years (year 1 and 2). The tax rate for Halliburton is 30%.

(a) Compute the net after-tax cash flows of the project.

(b) The cash flows of this project are risk-free. The market gives the

following interest rates:

Maturity (years) 1 2 3 ···

Spot interest rate (%) 4.00 6.00 6.50 ···

Should Halliburton take this project? Explain.

44

c

° 2008, Andrew W. Lo and Jiang Wang

2 SOLUTIONS

2 Solutions

2.4 Forward and Futures

1. Use simple arbitrage argument. To deliver one bushel of wheat in a

year, you can buy it today for $3.4 per bushel and store it for one

year. The cost of storage is $0.1 per bushel. So the total cost if $3.5

per bushel in today’s dollar. Project this forward one year using the

interest rate of 4% give the price of $3.5 ×(1 + 4%) = $3.64 for 1-year

forward contract.

2. We assume that the forward price is equal to (or very close) to the

futures price. The forward price is given by:

H

T

= S

0

(1 + r

T

)

T

·

Re-arreng this basic formulat to get:

r

T

=

µ

H

T

S

0

¶

1/T

− 1·

Applying this formula, we get the effetice annualized interest rates:

• October: r

Oct

= (635.60/633.50)

12

− 1 = 0.0405

• December: r

Dec

= (641.80/633.50)

4

− 1 = 0.0534