The New View of Fiscal Policy and Its Application

Jason Furman

1

Chairman, Council of Economic Advisers

Conference: Global Implications of Europe’s Redesign

New York, NY

October 5, 2016

This is an expanded version of these remarks as prepared for delivery.

A decade ago, the prevalent view about fiscal policy among academic economists could be

summarized in four admittedly stylized principles:

1. Discretionary fiscal policy is dominated by monetary policy as a stabilization tool

because of lags in the application, impact, and removal of discretionary fiscal stimulus.

2. Even if policymakers get the timing right, discretionary fiscal stimulus would be

somewhere between completely ineffective (the Ricardian view) or somewhat ineffective

with bad side effects (higher interest rates and crowding-out of private investment).

3. Moreover, fiscal stabilization needs to be undertaken with trepidation, if at all, because

the biggest fiscal policy priority should be the long-run fiscal balance.

4. Policymakers foolish enough to ignore (1) through (3) should at least make sure that any

fiscal stimulus is very short-run, including pulling demand forward, to support the

economy before monetary policy stimulus fully kicks in while minimizing harmful side

effects and long-run fiscal harm.

Today, the tide of expert opinion is shifting the other way from this “Old View,” to almost the

opposite view on all four points.

2

This shift is partly the result of the prolonged aftermath of the

global financial crisis and the increased realization that equilibrium interest rates have been

declining for decades. It is also partly due to a better understanding of economic policy from the

experience of the last eight years, including new empirical research on the impact of fiscal policy

as well as observations of the reaction of sovereign debt markets to the large increases in debt as

a share of GDP in the wake of the global financial crisis. In the first part of my remarks, I will

discuss the theory and evidence underlying this “New View” of fiscal policy (with, admittedly,

the core of this theory being an “Old Old View” that dates back to John Maynard Keynes and the

liquidity trap).

1

I am grateful to Olivier Blanchard, Maurice Obstfeld, Christopher Otrok, Carmen Reinhart, Kenneth Rogoff,

Katheryn Russ, Jay Shambaugh, Lawrence Summers, Natacha Valla, and Jeromin Zettelmeyer for helpful comments

and discussions. Marie Cases, Harris Eppsteiner, and Robert Liu provided research assistance.

2

For the Old View, see Taylor (2000). For some papers consistent with the New View, see IMF (2014), OECD

(2016), DeLong and Summers (2012), and Blinder (2016).

2

Of course, what I describe as the Old View was not a consensus position among all academic

economists (see, for one example, Blinder 2004). Moreover, those working in policy often took

the opposite tack. While many academics and textbooks were often skeptical about discretionary

fiscal stimulus, policymakers in the United States couched policy proposals intended to combat

at least the last three recessions in terms of stimulus. Moreover, what I will describe as the New

View of fiscal policy does not constitute a consensus, either. Although the New View is

increasingly found in research by academics, policy-oriented economists, and international

institutions such as the International Monetary Fund (IMF) and the Organisation for Economic

Co-operation and Development (OECD), and is embodied both in statements by these

institutions and in communiqués by the G-20, many policymakers still shy away from

implementing it in practice.

This disconnect between the New View and its application in practice is the second topic of my

remarks today. One reason for the disconnect is that some policymakers still have not accepted

the substantive theory and evidence behind the New View. But the disconnect is partly

institutional in origin. In the United States, the primary institutional issue is relatively weak

automatic stabilizers. In the case of the Europe, the institutional issues run deeper. Most notable

among them is the fact that macroeconomic institutions have been built in accord with the Old

View, with an entity for monetary policy at the euro area level, but with no corresponding entity

for fiscal policy.

I offer some suggestions for closing the divide between the New View and the conduct of fiscal

policy, some of which are common across countries. These include the benefits of additional,

efficiently allocated investments in areas like infrastructure, research, education and training. In

addition, better automatic stabilizers would be helpful, which for the United States means greatly

strengthening existing stabilizer and which for Europe means, at a minimum, allowing existing

stabilizers to actually function. More importantly, the New View of fiscal policy underscores the

importance of a more coordinated fiscal policy in Europe as well as a shift towards focusing on

the longer-run fiscal situation.

Theory and Evidence for the New View of Fiscal Policy

The New View of fiscal policy largely reverses the four principles of the Old View—and adds a

bonus one. In stylized form, the five principles of this view are:

1. Fiscal policy is often beneficial for effective countercyclical policy as a complement to

monetary policy.

2. Discretionary fiscal stimulus can be very effective and in some circumstances can even

crowd in private investment. To the degree that it leads to higher interest rates, that may

be a plus, not a minus.

3. Fiscal space is larger than generally appreciated because stimulus may pay for itself or

may have a lower cost than headline estimates would suggest; countries have more space

today than in the past; and stimulus can be combined with longer-term consolidation.

3

4. More sustained stimulus, especially if it is in the form of effectively targeted investments

that expand aggregate supply, may be desirable in many contexts.

5. There may be larger benefits to undertaking coordinated fiscal action across countries.

I will discuss each of these five in turn.

Principle 1: Fiscal Policy Is Often Beneficial For Effective Countercyclical Policy As a

Complement to Monetary Policy.

In the summer of 2015, I met with Fed Up, an advocacy group focused on monetary policy, at

the Federal Reserve Bank of Kansas City’s Symposium in Jackson Hole. I started by telling them

that, consistent with Administration policy, I do not comment on monetary policy, either in

private or in public. Instead, I focused my comments to them on the importance of fiscal policy

in supporting aggregate demand.

A year later, many of the Governors of the Federal Reserve and presidents of the regional

Reserve Banks held a public meeting with Fed Up and, among other messages, told the group

that fiscal policy is essential in supporting aggregate demand and that the entire burden should

not fall on monetary policy.

The message was consistent, but not coordinated—and it reflects a view which is heard

increasingly often from central bankers and institutions like the IMF and which is well-presented

by Mohamed El-Erian (2016) in his book The Only Game in Town. Specifically, monetary policy

cannot, by itself, be fully effective and would benefit from supportive fiscal policy. For example,

in Congressional testimony in 2013, then-Chairman of the Federal Reserve Ben Bernanke noted,

“Although monetary policy is working to promote a more robust recovery, it cannot carry the

entire burden of ensuring a speedier return to economic health. The economy’s performance both

over the near term and in longer run will depend importantly on the course of fiscal policy.”

In part, this view is motivated by the limitations of conventional monetary policy resulting from

the long-term trend across the advanced economies toward lower equilibrium interest rates.

These lower equilibrium rates, in turn, affect the level of nominal rates, both during

accommodative and tight conditions.

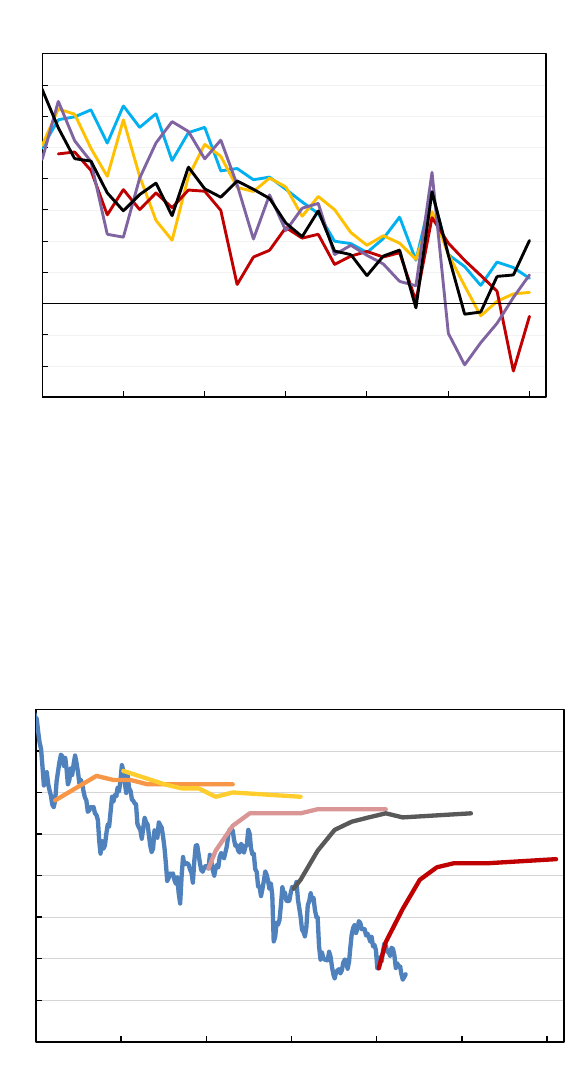

This is not a recent phenomenon. The real interest rate has trended down since the 1980s in a

wide range of countries and prior to the global financial crisis in 2007 was already quite low

relative to its history, as shown in Figure 1.

4

Figure 1

For decades, at least in the United States, economists and financial markets missed this

development—consistently expecting interest rates to rise and then stabilize (as shown in Figure

2), when in fact they kept falling. Even today, while the Blue Chip forecast expects the U.S.

nominal rate on ten-year Treasury notes to eventually rise to 3.9 percent, the market-implied rate

is about 1 percentage point lower for the ten-year yield ten years from now.

Figure 2

A range of explanations have been advanced for this decline in interest rates. These include

increased global savings, less global demand for investment, and a paucity of safe assets as well

as shifting demographics and changes in potential output or productivity growth, with some of

these developments associated with what has been termed “secular stagnation” (Summers 2014;

Tuelings and Baldwin 2014). But regardless of the cause, the sustained and widespread decline

France

Japan

United Kingdom

Germany

United States

-3

-2

-1

0

1

2

3

4

5

6

7

8

1985 1990 1995 2000 2005 2010 2015

Real Ten-Year Benchmark Rate in Selected Countries

Percent

2015

1996

2000

2005

2010

2015

0

1

2

3

4

5

6

7

8

1995 2000 2005 2010 2015 2020 2025

Percent

Ten-Year Treasury Rates and Historical Economist Forecasts

5

of real interest rates indicates that even as rates have partly rebounded from their post-crisis lows

they are unlikely to return to where they were expected to be prior to the crisis (CEA 2015;

Holston, Laubach, and Williams 2016).

The stronger form of secular stagnation argues that with low inflation, real interest rates cannot

fall low enough to restore aggregate demand as a result of the effective lower bound, leading to a

self-reinforcing spiral of weak economic performance and low interest rates. While I do not

believe the stronger form of the secular stagnation is a correct description of the United States or

Europe, the weaker form—that conventional monetary policy will be constrained more often in

the future—is certainly a source of concern (Furman 2014).

In 2000, David Reifschneider and John Williams estimated that the zero lower bound would be

constraining about 5 percent of the time in the United States, with a mean duration of four

quarters when rates hit the zero lower bound. However, the experience across the advanced

economies since the Great Recession suggests that, if anything, this estimate was overoptimistic.

As the authors clearly stated at the time, a key assumption in this result was that the equilibrium

real federal funds rate was 2.5 percent, the consensus view at the time. This is well above the

most recent projections from the members of the Federal Open Market Committee, which range

from 0.5 to 1.8 percent for the long-run real federal funds rate. Consequently, it is reasonable to

assume that the zero lower bound or effective lower bound will constrain conventional monetary

policy more than 5 percent of the time in the future (Dordal-i-Carreras et al. 2016).

3

And while

unconventional monetary policy can still operate, there is substantial controversy on its efficacy

and side effects—making other, complementary efforts to achieve the same goals desirable.

Principle 2: Discretionary Fiscal Stimulus Can Be Very Effective in Practice

For decades after World War II, the ability of fiscal policy to affect the economy was broadly

accepted (see, for example, Blinder and Solow 1973). In fact, the principal objection to the use of

fiscal policy was not that it did not affect the economy. It was, in fact believed, to do just that—

just that policymakers would do a bad job timing its impact, so that in practice it would add to

instability rather than reducing it (Friedman 1953).

A decade ago, however, even the basic premise underlying the earlier debate about fiscal policy

was increasingly under assault. On one side was the Ricardian view that rational, forward-

looking agents could effectively undo fiscal stimulus. In this view, what matters is a country’s

consolidated balance sheet, and if the government takes on more debt, this action would flow

through to private agents, who would in turn take on less (Barro 1974). On the other side was an

increasing focus on the side effects of fiscal stimulus in terms of higher interest rates and reduced

private investment (Ball and Mankiw 1995). In fact, one argument was that the 1990 and 1993

fiscal consolidations in the United States were actually expansionary (Blinder and Yellen 2001),

an argument that was subsequently generalized (Alesina and Ardagna 2010).

3

Changes to monetary policy rules could affect the frequency with which the effective lower bound is binding

(Goodfriend 2016; Williams 2016). But my argument applies to the degree that these policy rules have not changed;

to the degree that changing them is costly, so more active fiscal policy could obviate the need to incur those costs; or

to the degree that, even with the new rules, monetary policy still has limitations or side effects.

6

However, an increasing body of evidence has found that fiscal expansion can have large positive

effects, with a number of papers predating what I call the New View. Some of the evidence is

historical. On the revenue side, Romer and Romer (2010) examine exogenous tax changes in the

U.S. since World War II and find resulting multipliers as high as 3, mostly due to the effects of

the actual changes, rather than news of changes, on investment. On the spending side, studies

that focus on historical exogenous (unpredicted) changes in U.S. government expenditure find

output multipliers ranging from 0.6 to 1.2 (Ramey and Shapiro 1998; Blanchard and Perotti

2002; Ramey 2011).

Some of the evidence for the efficacy of fiscal stimulus comes from more recent episodes.

Studies based on more recent data on Federal defense spending associated with the Recovery Act

detect multipliers over 1 in some scenarios (Nakamura and Steinsson 2014). Consumer-level

microeconomic data from the 2001 and 2008 U.S. tax credits show evidence that liquidity-

constrained households spent a sizable fraction of that rebate (Parker et al. 2013). Some

convincing evidence that gets around the endogeneity of fiscal decisions in the aggregate data by

studying the State-level effects of effectively random elements of the 2009 Recovery Act in the

United States also finds sizable effects from fiscal stimulus (Chodorow-Reich et al. 2012).

In theory, when monetary policy is at the effective lower bound, fiscal policy may even be more

effective than previously realized. This is because monetary policy will not partially offset fiscal

policy through either an interest-rate channel or an exchange-rate channel. In fact, fiscal policy

could even crowd in additional private investment to the degree that expanded aggregate demand

raises growth rates and thus increases investment growth, as predicted by the standard

accelerator model for investment that has done a reasonably good job explaining recent trends in

investment (IMF 2015; OECD 2015).

Also, when monetary accommodation is constrained by the effective lower bound in an economy

with a large output gap, fiscal expansion can expand private investment by raising inflation

expectations, which would lower real interest rates (Hall 2009; Christiano, Eichenbaum, and

Rebelo 2011;Woodford 2011). The reaction function of monetary policy is important, as some

(for example, Woodford 2011) have argued that a monetary authority that reverts to a Taylor-

type rule during fiscal expansion will significantly reduce fiscal multipliers.

Moreover, even if over the medium term fiscal policy does lead to higher equilibrium interest

rates, this may actually belong on the plus side the ledger rather than the minus side, given that a

higher equilibrium interest rate will offset some of the negative effects of secular stagnation,

raising the neutral rate and thus creating more room for conventional countercyclical monetary

policy (Summers 2014).

Principle 3: Fiscal Stimulus Is Less Constrained by Fiscal Space than Previously Appreciated

As the notions that conventional monetary policy faces constraints and that fiscal policy is more

effective than previously appreciated become increasingly harder to dispute, the arguments

against fiscal stimulus have increasingly relied on the claim that however effective fiscal

7

expansion may be in theory, in practice there is limited or no fiscal space for countercyclical

fiscal policy. This claim stems in part from an idea that the sovereign debt crisis in Europe was

solely the result of irresponsible government spending. This may have been the case in certain

countries, but governments have also faced non-fiscal issues like property bubbles or banking

insolvency. In fact, there is no correlation between countries whose debt-to-GDP ratio rose prior

to the crisis and those that saw their sovereign spreads spike during 2011. The spikes in debt in

places like Ireland and Spain were far more a result of the crisis than a cause (Shambaugh 2012).

The concern with the medium- and long-term deficit underlying concerns about fiscal space is

certainly valid, and is particularly important given slower growth and demographic pressures.

But the need for immediate austerity does not follow. While not every country has the same

degree of fiscal space, the tendency today is toward being excessively cautious in the name of

fiscal responsibility. Let me expand on these three arguments for this view:

First, the growth associated with fiscal stimulus can improve fiscal sustainability. The key metric

for debt sustainability is not the absolute level of debt, but debt scaled by the size of the

economy. To the degree that fiscal stimulus is more effective when monetary policy is

constrained, it may raise output more than it raises debt—thus reducing the debt-to-GDP ratio

and improving fiscal sustainability (DeLong and Summers 2012; Gaspar, Obstfeld, and Sahay

2016; OECD 2016).

In some of the literature, these results are based solely on the demand-side stimulus, assuming a

monetary policy reaction function that does not tighten policy in response to the fiscal stimulus,

possibly because it had previously been constrained. Note that, to the degree that expanded

demand raises inflation towards its target, it could also help with debt sustainability because

nominal output is the relevant denominator for debt.

But the results are even stronger when the supply-side effects of well-crafted government

investments are considered (IMF 2014). The standard interpretation is that the larger economy

that results from infrastructure investment will result in additional tax revenue. An alternative

interpretation is that increased maintenance expenditures today will reduce maintenance costs in

the future and, assuming these maintenance costs grow faster than real interest rates, increased

investment today would reduce the amount of deferred maintenance passed on to future

generations, improving the government’s balance sheet in net-present-value terms by swapping

an implicit liability (deferred maintenance) for a smaller explicit liability (public debt).

While the particular result that fiscal expansion by itself will reduce the debt-to-GDP ratio

depends on particular parameters and assumptions, the fact that different models find similar

results suggests that the idea that fiscal expansion can improve fiscal sustainability is worth

taking seriously. And at the very least the real cost of fiscal stimulus is less than the headline

numbers would suggest.

In some respects, this argument may be even more important in high-debt economies like Japan

and Italy. This is because changes in the debt-to-GDP ratio depend on two factors: (i) the

difference between interest rates and the growth rate (strictly speaking, r minus g multiplied by

the debt-to-GDP ratio) and (ii) the primary balance (the difference between revenue and non-

8

interest spending). The larger the debt is, the more changes in r – g dwarf the primary balance in

the determination of debt dynamics—and so policies that raise g without triggering concerns that

raise r by even more can be especially effective in improving sustainability.

4

A key condition for this to be true, and one that should not be taken for granted in all

circumstances, is that interest rates do not rise more than growth rates. To some degree this is

under the control of policymakers—both fiscal policymakers, who can make short-run fiscal

expansion even more effective by pairing it with longer-run fiscal consolidation, and monetary

policymakers, who may choose to accommodate fiscal expansion. Even absent the ideal fiscal

package, this argument seems to be consistent with the perceptions of financial markets. For

example, Japan’s two delays of its consumption tax increase sent yields on government bonds

down, not up—since markets expected that the resulting stronger growth would make repayment

of the debt easier in the future. In many cases in Europe in the last eight years, downgrades to

sovereign debt ratings have come with warnings of growth prospects, not spending

irresponsibility. Markets seem well aware that growth is needed to make finances sustainable in

the future. This is consistent with the historical experience of the United States, where nominal

growth, and not fiscal consolidation, have been critical for establishing debt sustainability (Hall

and Sargent 2011).

Second, even to the degree that stimulus adds to the debt, views as to the optimal level of debt

itself need to be updated in a world where many countries have made progress on future pension

and health liabilities, interest rates appear persistently lower, and the demand for safe assets

appears higher.

Public debt has risen across the advanced economies. But in assessing fiscal exposure it is

important to not rely too much on public debt alone, which is essentially a backward-looking

measure that records cumulative deficits to date. Forward-looking measures like the fiscal gap

and an understanding of contingent liabilities are important. In the United States, projections of

the fiscal gap by the Congressional Budget Office and the Office of Management and Budget

have fallen in the last six years largely due to a combination of legislation raising revenues and

cutting spending and projections for slower health cost growth. These changes—and the fact that

they have such important impacts on future debt sustainability—highlight that a focus on current

deficits or on whether investments in long-run productivity today are affordable misses the fact

that stimulus or education and infrastructure spending typically pale in comparison to health and

pension spending when considering long-run budget sustainability.

4

Some have argued that higher growth has only a limited effect on fiscal sustainability because it automatically

leads to higher pensions and greater spending in other areas (for example, faster growth could raise wages more

quickly, increasing the cost of providing government-funded healthcare). But even for pensions, the elasticity of

present-value spending with respect to growth is considerably less than one—because of lags in when benefits

adjust—and pensions are just a portion of overall government spending. So only a portion of the additional revenues

associated with the higher growth rate would be offset by the additional spending it triggered.

9

Of the advanced economies tracked by the IMF for which data are available, nearly three-

quarters have smaller expected increases in pension and health costs between 2010 and 2030

according to the latest projections than according to projections from 2011 (IMF 2011; IMF

2016b). In addition, many countries have also cut other spending and/or raised revenue as a share

of GDP. While most countries continue to have a long-run fiscal challenge, on a going-forward

basis the magnitude of the challenge tends to be smaller than what was expected five years ago.

In some cases, however, changes in contingent liabilities—like private debt that could become

public debt in the event of a crisis—would also need to be factored in, although no good

estimates of changes in these are available.

Moreover, the optimal stock of government debt as a share of the economy depends on the rate at

which these liabilities are discounted. While economists do not have a fully convincing

quantification of the optimal level of government debt, if interest rates are permanently lower

than previously expected, then the optimal stock of debt should be higher (Elmendorf and

Sheiner 2016).

5

This is especially true to the degree that countries are borrowing in their own

currency and/or are able to lock in very long-term debt at very low interest rates.

Furthermore, changes in risk perceptions about privately created debt and regulatory changes on

the types and quality of assets on banking balance sheets have left the world in a safe-asset

shortage. Financial markets today demand more safe assets and are even willing to pay for the

right to possess them, as demonstrated by the continuing purchase of government bonds despite

low interest rates. In part, we have learned that some assets we thought were safe, or that were

rated triple-A, were in fact less safe than assumed. As these assets ceased to be seen as safe, this

put more pressure on the supply of the remaining assets that were considered safe. Fiscal

stimulus, paid for through the issuance of longer-term bonds, could mitigate this apparent

shortage of safe assets (Caballero, Farhi, and Gourinchas 2016).

Based on current interest rates, capital markets judge that borrowing by most countries at this

point would be safe. Low interest rates have also resulted in relatively low interest payments as a

share of GDP across most major advanced economies, as shown in Figure 3.

5

Declines in expected growth rates lower the optimal stock of government debt. But interest rate expectations have

come down considerably more than growth expectations, consistent with the fact that interest rate forecasts had a

large, systematic bias towards being too high for several decades while growth forecasts were generally unbiased.

10

Figure 3

Finally, to the degree the first and second points are true, that is sufficient to justify the existence

of fiscal space. But even if they are not correct, the answer to the question of which countries

have fiscal space is any country that has a credible political system that is capable of making

firm, long-term commitments, since upfront fiscal expansion can be combined with medium- and

long-term fiscal consolidation.

Not every country has a political system that is capable of making credible commitments about

the future trajectory of fiscal policy. But the ones that do can create more fiscal space by

combining short-term expansion with medium- and long-term consolidation. Ideally the

consolidation would be enacted simultaneously with the expansion and would be credible—for

instance, phasing in gradually in a plausible manner rather than creating a cliff that ultimately

gets pushed out further. For example, the 1983 Social Security pension reforms in the United

States that gradually raised the Normal Retirement Age from 65 to 67 phased in between 2000 to

2022, an increase that has been implemented with little attention and no controversy. Recently,

the United States has taken steps that have cut long-term health costs while raising long-term

revenue. And, as noted above, many advanced economies have also lowered their long-term

spending increases and have raised revenue levels.

Principle 4: It May be Desirable to Pursue Sustained Fiscal Expansion

The Old View of fiscal policy left many economists, especially more academic ones, skeptical of

any role for discretionary countercyclical fiscal policy. To the degree that economists allowed for

a role for discretionary fiscal policy, it was for limited fiscal expansion focused on very short

periods of time. The logic was that fiscal policy could actually have a more immediate effect on

the economy than monetary policy and thus potentially fill a hole in aggregate demand

(Elmendorf and Furman 2008). For example, in 2008 the United States started sending electronic

payments to households less than three months after the stimulus was enacted and in 2009

reduced tax withholding was implemented within a month and a half of the passage of the

Canada

2017

France

Germany

Italy

Japan

UK

United States

-2

0

2

4

6

8

10

12

1960 1970 1980

1990 2000 2010 2020

Net Interest Payments on Government Debt

Percent of GDP

11

Recovery Act. In contrast, a variety of standard models show that monetary policy takes several

quarters to have a substantial impact and more than a year and a half to have its maximum

impact (Ramey 2016).

The New View of fiscal policy, based on the empirical and analytical observations above, places

more weight on sustained fiscal policy, especially if it is conducted through effectively allocated

investments. Sustained fiscal policy may be necessary because the global economic climate may

be showing symptoms of persistently inadequate demand dragging on growth and inflation.

Sustained fiscal policy can play a critical role not only in demand but also in expanding

productivity and aggregate supply going forward. In fact, to the degree that the return on projects

substantially exceeds the government’s borrowing costs then sustained increases in government

investment would be justified regardless of the situation facing aggregate demand. IMF

researchers found that a permanent increase in government investment of 1 percent of GDP

increases growth through permanently increasing investment and consumption. Furthermore, this

fiscal spending creates future fiscal space through increasing government revenue and reducing

the debt-to-GDP ratio, as shown in Figures 4a and 4b (Gaspar, Obstfeld, and Sahay 2016).

Figure 4a

Figure 4b

Investments in innovation may have even higher long-run payoffs, with the IMF finding that an

expansion of research and development (R&D) with an annual fiscal cost of 0.4 percent of GDP

can raise the long-run output level by 5 percent in advanced economies (IMF 2016a).

Moreover, the IMF’s framework is not stochastic. As discussed earlier, in addition to these

deterministic effects the higher equilibrium interest rates associated with sustained increases in

demand can create more room for conventional monetary policy in combatting future downturns.

Even with these results, however, there is still an argument for paying for research or

infrastructure spending both because it could result in even more medium- and long-term deficit

reduction and because well-designed financing mechanisms—for example, the fee on oil as

proposed by the Obama Administration—could also improve the utilization of infrastructure. But

to the degree the political system generates a choice between unfinanced investments or no

0.0

0.4

0.8

1.2

1.6

2.0

0 2 4 6 8 10

Effect

of Permanent Increase in Government Investment on

Real GDP

Percent Deviation from Baseline

Number of Years

-2.0

-1.6

-1.2

-0.8

-0.4

0.0

0.4

0 2 4 6 8 10

Effect of Permanent Increase in Government Investment on

Government Debt-to-GDP Ratio

Percent Deviation from Baseline

Number of Years

12

investments, as long as the investments are allocated at least reasonably effectively the former is

likely to dominate the later.

Principle 5: Fiscal Policy Can Have Positive Global Spillovers—And Can Be Even More

Effective With Global Coordination

An implication of the argument by Eggertsson et al. (2016) is that in a world characterized by

inadequate demand and low interest rates, shocks to demand can spill even more swiftly and

strongly across borders. Normally, a demand contraction in one country, caused by fiscal

consolidation for example, will spill into others through shrinking imports, resulting in less

demand for foreign goods. Usually that country’s currency will depreciate, giving their exports

an advantage, and thus resulting in a current account surplus. The demand shock affects the other

countries, leading to lower interest rates, possibly lower saving rates or higher investment rates,

but it does not need to directly affect overall GDP. If other countries have room for monetary

easing, those countries can easily offset the reduction in demand, which among other things

would shift exchange rates and temper the movements of the current account.

However, at the effective lower bound, policies that lead to large current account surpluses

cannot be offset with monetary policy in other countries. Thus, a fiscal contraction abroad spills

more directly into GDP. Note, the demand shock from fiscal consolidation has likely been more

significant in the euro area, where the single market makes these spillovers even more direct and

members cannot rely on the mitigating effects of exchange rates and monetary policy.

Fiscal expansions can have large positive spillovers, especially when they are internationally

coordinated. A fiscal expansion can increase demand in both the domestic economy and the

economies of its trade partners. To the extent that business investment has been held back by low

GDP growth, and in particular low global GDP growth, a coordinated expansion could also lift

investment, further buoying the world economy.

IMF researchers find that countries or regions engaging in an individual permanent fiscal

expansion worth 1 percent of GDP face rising deficits and debt levels. However, when stimulus

is coordinated across all regions, additional growth reached at least 1 percent in each region,

cumulating to an additional 2.3 percent in global growth, while the debt-to-GDP ratio reduced

everywhere (Gaspar, Obstfeld, and Sahay 2016). This strengthens the case for mutual reliance on

fiscal policy that undergirds, for example, the G-20’s inclusion of fiscal policy as one of three

tools for strengthening growth (G-20 2016).

The New View in Practice in the United States and the Euro Area

Economic opinion, including among both researchers and policy-oriented bodies, is increasingly

shifting towards this New View of fiscal policy. This has led to some odd role reversals.

Historically, the canonical situation was that irresponsible policymakers wanted to increase

deficit spending, but they were restrained by international institutions like the IMF and the

13

OECD. Nowadays, we sometimes have the opposite situation—with those institutions, at least in

the abstract, pushing fiscal stimulus while national authorities are more reluctant to embrace it.

One source of the reluctance that some policymakers have to implement the New View of fiscal

policy is substantive disagreement with its principles. But in the case of the United States and

Europe, there are other institutional issues as well. In the United States, we have relatively weak

automatic stabilizers that place much of the burden for fiscal stimulus on a political system that

can be sclerotic on fiscal policy at best. In the case of the euro area, the macroeconomic

institutions themselves were built consistent with the Old View of fiscal policy and will require

reform and institutional change to work in a world characterized by the New View. I will discuss

these two areas in turn.

The United States

In the United States, we acted quickly and substantially starting in 2008 and accelerating greatly

in 2009 to institute discretionary countercyclical fiscal policy. From 2009 to 2012, the United

States passed more than a dozen expansionary fiscal measures that included a combination of

individual tax cuts; business tax incentives; investments in infrastructure, energy, and research;

relief for State and local governments; and expanded transfer payments. In total, these measures

delivered $1.4 trillion of discretionary fiscal stimulus, or an average of 2 percent of GDP over

that four-year period. Together with automatic stabilizers, the total fiscal stimulus averaged 4

percent of GDP over that period. In total, as measured by the change in the primary balance as a

share of GDP, the United States had more fiscal stimulus than the euro area in each year from

2009 to 2012 (Furman 2016). But then, contrary to the Administration’s proposals, the stimulus

was abruptly withdrawn in 2013.

Fiscal fatigue—in a political, but not economic sense—played a role in this premature

withdrawal of stimulus. Take the case of the emergency extension of unemployment insurance

benefits to allow jobseekers to receive benefits for more than six months. Consistent with

practice in past recessions, Congress passed extended benefits on a bipartisan basis in June 2008

when the unemployment rate was 5.3 percent, and the long-term unemployment rate (defined as

those unemployed six months or more) was 1.0 percent. But Congress then allowed extended

benefits to expire at the end of 2013, when the unemployment rate was 6.7 and the long-term

unemployment was 2.5 percent, well above what they were when extended benefits were

initiated in the first place. At least in part this was because many legislators felt that benefit

outlays had been too high for too long and so wanted them to end. Of course, an optimal strategy

is to make unemployment benefit rules dependent on the economic situation, not arbitrary

periods of time. In particular, it is optimal to have benefits for longer when the unemployment

rate is higher, since to the degree moral hazard is an issue for unemployment insurance, it is less

of an issue when the unemployment rate is higher (Kroft and Notowidigdo 2016).

The United States has a political system in which fiscal changes can be difficult to implement

given the frequency of divided government and procedural rules in the Senate. At the same time,

the United States’ automatic fiscal stabilizers are relatively weak compared to other countries’,

largely because government spending is a smaller share of our economy, as Figure 5 shows.

14

Figure 5

In recent years, the United States has improved its automatic stabilizers by making the fiscal

system more progressive and establishing universal health insurance—so in a downturn, more

Americans would get financial assistance for health insurance. But additional automatic

stabilizers would be warranted. In particular, stabilizers focused on providing resources to people

when they are most likely to spend them—which corresponds to the provision of insurance to

help cash-constrained households smooth their consumption—would be especially useful. One

such measure would be to automatically extend unemployment insurance when the

unemployment rate is high or rising, as proposed in the President’s Fiscal Year 2017 Budget.

Additional “semi-automatic” stabilizers that are not based on individual circumstances but

triggered off of economic circumstances are worth seriously considering.

In particular, more thought is needed about the changing role that State and local budget policies

play in the business cycle. In the wake of the Great Recession, State and local government

spending contracted, deepening the recession and slowing the recovery. As Figure 6 shows, this

fiscal consolidation was in contrast to the experience of earlier business cycles.

AUS

AUT

BEL

CAN

CHE

DEU

DNK

ESP

FIN

FRA

GBR

GRC

IRL

ITA

JPN

KOR

LUX

NLD

NOR

NZL

PRT

SWE

USA

0.0

0.1

0.2

0.3

0.4

0.5

0.6

20 30

40 50 60

Government Size and the Cyclical Semi-Elasticity

of Automatic Stabilizers

Elasticity (Automatic Stabilizers)

Government Size (Spending to GDP Ratio)

15

Figure 6

The Federal Government has considerably more capacity to both insure against idiosyncratic

risks to particular States and to borrow in recessions than do subnational governments, as a result

both of current laws (all but one U.S. State has balanced budget requirements) and of financial

market perceptions. Moreover, State and local governments rationally do not take into account

the positive spillovers from their policies and, left to their own devices, will undertake too little

stimulus. In addition, while it might make sense to agree ex ante to share risks when no one State

knows what risks it will face, such a deal is impossible ex post after the shocks have been

realized. Finally, the arguments I made earlier about financial market confidence being partly

based on the expectation of higher growth leading to more fiscal sustainability do not apply with

as much force to smaller, more local areas, which bear the full cost of the additional debt

incurred in stimulus but get only a fraction of the economic benefits.

For all of the reasons, it makes sense for the affirmative fiscal response in the United States to

remain primarily at the Federal level. But more thought may be needed to understand whether

the pro-cyclical subnational fiscal policy in the wake of the Great Recession that moved in the

opposite direction from the expansionary Federal response is likely to become the norm going

forward and, if so, what role Federal policy could have in counteracting it.

The Euro Area

The institutional structure of the euro area reflects the Old View of fiscal policy. There is no

entity with the responsibility to manage macroeconomic policy at the euro area level other than

the European Central Bank (ECB). Thus, shocks that affect the entire euro area or that have

important spillovers can be addressed by monetary policy alone. Additionally, to the degree there

is coordination, it is asymmetric—with a Stability and Growth Pact (SGP) that can compel

deficit reduction but cannot compel fiscal expansion. This institutional framework exacerbates

what were already distorted incentives at the national level to undertake too little expansionary

fiscal policy when it is needed or to use contractionary fiscal policy when it is inappropriate,

1975

1982

1991

2001

Current Cycle

(2009:Q2 Trough)

Average

Excluding

Current Cycle

80

90

100

110

120

130

-20 -15 -10 -5 Trough 5 10 15 20 25

Real State and Local Government Purchases During Recoveries

Index, Business

-Cycle Trough = 100

16

since neither euro area countries themselves nor financial markets purchasing their debt take into

account the spillovers their fiscal policy has on their neighbors.

In a theoretical world where shocks are best handled by monetary policy and the role of fiscal

policy is both to handle idiosyncratic shocks at the country, but not European level, and also to

reduce the deficit, this set of institutions may be adequate. But if monetary policy can run into

limits where fiscal policy is needed as a supporting macroeconomic policy tool at the European

level, or if shocks are persistent enough that fiscal policy must be deployed in more than a short

burst, the current euro area fiscal institutions act as barriers to effective policy.

Moreover, the SGP is focused on current deficits and debt—without systematically incorporating

future liabilities. In a world where fiscal policy is not expected to play a role in supporting

aggregate demand, this may be the best way to design the rule. While in economic theory, the

time path of the deficit matters less than its present value, in political-economy practice back-

loaded deficit reduction risks being gameable. But if there is an important role for fiscal policy in

supporting aggregate demand, as suggested by the New View, then it may be worth trading off

some risk of gaming to allow countries to undertake a much superior fiscal policy that would

combine short-run expansion with long-run consolidation. Moreover, focusing on long-term

liabilities may also encourage fiscal discipline in ways that a backward-looking rule would not.

In the most recent set of crises in the euro area, budget policies interacted with the fact that

financial rescues were at the country level, such that countries in financial crisis had to

exacerbate problems by making fiscal cuts which weakened the economy and fed back to

weakening banks and hence the budget even more. The European institutional structure seemed

to amplify shocks rather than dampen them (Shambaugh 2012). A number of countries,

particularly Spain and Ireland, have made sizable budget cuts despite having high unemployment

rates and interest rates already at zero. There is ample evidence that these cuts deepened these

countries’ recessions. Some progress has been made on the financial institutions—though legacy

issues persist—but the holes on the fiscal side remain.

The economically preferable solution to this problem would be to undertake more

countercyclical fiscal policy at the euro area level—for example, automatic stabilizers like

unemployment insurance benefits; meaningful increases in infrastructure funding through, for

example, the European Investment Bank; or simply more coordinated fiscal policy either through

a revision of the SGP or the establishment of a new multilateral agreement. Such steps would

respond optimally to the large spillovers of country-level fiscal policy, would reflect the even

greater fiscal space at the European level, would provide a mutual insurance system against

shocks that disproportionately affect certain areas, and would also look at fiscal sustainability on

a more forward-looking basis that would include credit for long-term fiscal consolidations.

Absent greater fiscal mutualization, the euro area already has much stronger automatic stabilizers

than the United States. Tax rates are higher, such that a downturn automatically leads to larger

reductions in government revenues, and social safety nets are usually more generous, such that

downturns are met with larger increases in spending. Taxes and social transfers in Europe were

important to softening the effect of the recession both in terms of growth and of income

inequality (OECD 2013). In fact, public transfers contributed most to growth in places hit hardest

17

by the recession. The challenge is less about strengthening automatic stabilizers within

countries—although that would be welcome—and more about making sure that they are not

undone by pro-cyclical discretionary fiscal policy that is required by the SGP. If more of the

stabilizers were funded at the euro area level, it would reduce the budget pressure on individual

member states when they face an asymmetric downturn.

Conclusion

The New View of fiscal policy is increasingly being accepted in economic policy circles. More

and more policymakers appreciate that fiscal policy is a critical complement to monetary policy

and that we have used it too little, especially given its effectiveness and given the greater fiscal

space we had relative to eight years ago. In addition, more and more researchers have found that

additional public investments may be justified on purely supply-side grounds if its rate of return

substantially exceeds the government’s borrowing costs.

In many cases, the ideal policy would be short-term expansion combined with medium- and

long-term consolidation. Infrastructure or research spending may still reduce the debt-to-GDP

ratio if it is not paid for, but given the large medium- and long-term debt it may be even better

economically to pay for it and have even more deficit reduction. Nevertheless, the weight of the

theory and evidence suggests that we should not let the perfect be the enemy of the good, and if

the only way to undertake additional investment is without financing it then it would still be

worth doing.

In practice, optimal or even good policy is dependent on the country and the circumstances, but

in general the bias of thinking among economists and research by international institutions is

increasingly towards more discretionary fiscal policy. At the same time, too many policymakers

are still too often biased towards less. A better understanding can help remedy some of that gap,

but it is no substitute for the institutional changes needed to underpin such a change. I have tried

to point out some of what these might be in my discussion today but, again, the exact changes

will depend on a broader set of considerations than the macroeconomic ones that have been my

focus today.

18

Notes to Figures

Figure 1

Source: National sources via Haver Analytics.

Figure 2

Note: Forecasts are those reported by Blue Chip Economic Indicators in March of the given

calendar year, the median of over fifty private-sector economists.

Source: Blue Chip Economic Indicators.

Figure 3

Source: Organisation for Economic Co-operation and Development.

Figures 4a and 4b

Source: Gaspar, Obstfeld, and Sahay (2016).

Figure 5

Source: Fatás and Mihov (2012).

Figure 6

Source: Bureau of Economic Analysis, National Income and Product Accounts; CEA

calculations.

19

References

Alesina, Alberto and Silvia Ardagna. 2010. “Large Changes in Fiscal Policy: Taxes versus

Spending.” Tax Policy and the Economy 24: 35-68.

Ball, Laurence and N. Gregory Mankiw. 1995. “What Do Budget Deficits Do?” Federal Reserve

Bank of Kansas City, Economic Policy Symposium – Jackson Hole: 95-119.

Barro, Robert J. 1974. "Are Government Bonds Net Wealth?" Journal of Political Economy 82

(6): 1095-1117.

Blanchard, Olivier and Roberto Perotti. 2002. “An Empirical Characterization of the Dynamic

Effects of Changes in Government Spending and Taxes on Output.” Quarterly Journal of

Economics 117 (4): 1329-1368.

Bernanke, Ben S. 2013. “Semiannual Monetary Policy Report to the Congress.” Testimony

Before the Committee on Banking, Housing, and Urban Affairs, U.S. Senate. February 26.

Blinder, Alan S. 2004. “The Quiet Revolution: Central Banking Goes Modern.” New Haven:

Yale University Press.

______. 2016. “Fiscal Policy Reconsidered.” The Hamilton Project. The Hamilton Project Policy

Proposal 2016-05.

Blinder, Alan S. and Robert M. Solow. 1973. “Does Fiscal Policy Matter?” Journal of Public

Economics 2 (4): 319-337.

Blinder, Alan S. and Janet L. Yellen. 2001. The Fabulous Decade: Macroeconomic Lessons from

the 1990s. New York: Century Foundation Press.

Caballero, Ricardo J., Emmanuel Farhi, and Pierre-Olivier Gourinchas. 2015. “Global

Imbalances and Currency Wars at the ZLB.” NBER Working Paper No. 21670.

Chodorow-Reich, Gabriel, Laura Feiveson, Zachary Liscow and William Gui Woolston. 2012.

“Does State Fiscal Relief during Recessions Increase Employment? Evidence from the American

Recovery and Reinvestment Act.” American Economic Journal: Economic Policy 4 (3): 118-

145.

Christiano, Lawrence, Martin Eichenbaum, and Sergio Rebelo. 2011. “When is the Government

Spending Multiplier Large?” Journal of Political Economy 119(1): 78-121.

Council of Economic Advisers (CEA). 2015. “Long-Term Interest Rates: A Survey.” Report.

DeLong, J. Bradford and Lawrence H. Summers. 2012. “Fiscal Policy in a Depressed Economy.”

Brookings Papers on Economic Activity 43 (1): 233-297.

20

Dordal-i-Carreras, Marc, Olivier Coibion, Yuriy Gorodnichenko, and Johannes Wieland. 2016.

“Infrequent but Long-Lived Zero-Bound Episodes and the Optimal Rate of Inflation.” Annual

Review of Economics 8 (1).

Eggertsson, Gauti B. Neil R. Mehrota, Sanjay R. Singh, and Lawrence H. Summers. 2016. “A

Contagious Malady? Open Economy Dimensions of Secular Stagnation.” NBER Working Paper

No. 22299.

El-Erian, Mohamed A. 2016. The Only Game in Town: Central Banks, Instability, and Avoiding

the Next Collapse. New York: Random House.

Elmendorf, Douglas and Jason Furman. 2008. “If, When, How: A Primer on Fiscal Stimulus.”

The Hamilton Project.

Elmendorf, Douglas and Louise Sheiner. 2016. “Federal Budget Policy with an Aging

Population and Persistently Low Interest Rates.” Hutchins Center on Fiscal and Monetary Policy

Working Paper No. 18. The Brookings Institution.

Fatás, Antonio and Ilian Mihov. 2012. “Fiscal Policy as a Stabilization Tool.” B.E. Journal of

Macroeconomics 12 (3).

Friedman, Milton. 1953. Essays in Positive Economics. Chicago: University of Chicago Press.

Furman, Jason. 2014. “The Global Economy: Demand, Supply and Interdependence.” Remarks

at Globes Israel Business Conference.

______. 2016. “Demand and Supply: Learning from the United States and Japan.” Remarks at

ESRI International Conference 2016.

G-20. 2016. “Communiqué: G-20 Finance Ministers and Central Bank Governors Meeting.” July

23-24.

Gaspar, Vitor, Maurice Obstfeld, and Ratna Sahay. 2016. “Macroeconomic Management When

Policy Space is Constrained: A Comprehensive, Consistent and Coordinated Approach to

Economic Policy.” IMF Staff Discussion Note.

Goodfriend, Marvin. 2016. “The Case for Unencumbering Interest Rate Policy at the Zero

Bound.” Federal Reserve Bank of Kansas City, Economic Policy Symposium – Jackson Hole.

Hall, Robert E. 2009. “By How Much Does GDP Rise if the Government Buys More Output?”

Brookings Papers on Economic Activity 40 (2): 183-249.

Hall, George J. and Thomas J. Sargent. 2011. “Interest Rate Risk and Other Determinants of

Post-WWII US Government Debt/GDP Dynamics.” American Economic Journal:

Macroeconomics 3 (3): 192-214

21

Holston, Kathryn, Thomas Laubach, and John C. William. 2016. “Measuring the Natural Rate of

Interest: International Trends and Determinants.” Federal Reserve Bank of San Francisco

Working Paper No. 2016-11.

International Monetary Fund (IMF). 2011. “Shifting Gears: Tackling Challenges on the Road to

Fiscal Adjustment.” Fiscal Monitor, April 2011.

______. 2014. “Chapter 3: Is It Time for an Infrastructure Push? The Macroeconomic Effects of

Public Investment.” World Economic Outlook, October 2014.

______. 2015. “Chapter 4: Private Investment: What’s the Holdup?” World Economic Outlook,

April 2015.

______. 2016a. “Chapter 2: Fiscal Policies for Innovation and Growth.” Fiscal Monitor, April

2016.

______. 2016b. “Debt: Use It Wisely.” Fiscal Monitor, October 2016.

Kroft, Kory and Matthew J. Notowidigdo. 2016. “Should Unemployment Insurance Vary with

the Unemployment Rate? Theory and Evidence. Review of Economic Studies 83 (3): 1092-1124.

Nakamura, Emi and Jon Steinsson. 2014. “Fiscal Stimulus in a Monetary Union: Evidence from

US Regions.” American Economic Review 104 (3): 753-792.

Organisation for Economic Co-operation and Development. 2013 (OECD). “Crisis Squeezes

Income and Puts Pressure on Inequality and Poverty in the OECD.” Report.

______. 2015. “Chapter 3: Lifting Investment for Higher Sustainable Growth.” OECD Economic

Outlook 2015. Paris: OECD Publishing.

______. 2016. “Interim Economic Outlook: Global Growth Warning: Weak Trade, Financial

Distortions.” Report.

Parker, Jonathan A., Nicholas S. Souleles, David S. Johnson, and Robert McClelland. 2013.

“Consumer Spending and the Economic Stimulus Payments of 2008.” American Economic

Review, American Economic Association 103(6): 2530-53.

Ramey, Valerie A. 2011. “Can Government Purchases Stimulate the Economy?” Journal of

Economic Literature 49 (3): 673-685.

______. “Macroeconomic Shocks and Their Propagation.” NBER Working Paper No. 21978.

Ramey, Valerie A. and Matthew D. Shapiro. 1998. “Costly Capital Reallocation and the Effects

of Government Spending.” Carnegie-Rochester Conference Series on Public Policy 48: 145-194.

22

Reifschneider, David and John C. Williams. 2000. “Three Lessons for Monetary Policy in a Low

Inflation Era.” Journal of Money, Credit, and Banking 32 (4): 936-966.

Romer, Christina D. and David H. Romer. 2010. “The Macroeconomic Effects of Tax Changes:

Estimates Based on a New Measure of Fiscal Shocks.” American Economic Review 100 (3): 763-

801.

Shambaugh, Jay C. 2012. “The Euro’s Three Crises.” Brookings Papers on Economic Activity 43

(1): 157-231.

Summers, Lawrence H. 2014. “U.S. Economic Prospects: Secular Stagnation, Hysteresis, and the

Zero Lower Bound.” Business Economics 49 (2): 65-73.

Taylor, John B. 2000. “Reassessing Discretionary Fiscal Policy.” Journal of Economic

Perspectives 14 (3): 21-36.

Teulings, Coen and Richard Baldwin, eds. 2014. Secular Stagnation: Facts, Causes and Cures.

London: Centre for Economic Policy Research

Williams, John C. 2016. “Monetary Policy in a Low R-Star World.” Federal Reserve Bank of

San Francisco Economic Letter No. 2016-23.

Woodford, Michael. 2011. “Simple Analytics of the Government Expenditure Multiplier.”

American Economic Journal: Macroeconomics 3 (1): 1-35.