Chapter 4

The Savings and Loan Crisis

The Savings and Loan Crisis

and Its Relationship

and Its Relationship

to Banking

to Banking

Introduction

No history of banking in the 1980s would be complete without a discussion of the

concurrent crisis in the savings and loan (S&L) industry. A review of the S&L debacle (as

it is commonly known today) provides several important lessons for financial-institution

regulators. Moreover, legislation enacted in response to the crisis substantially reformed

both bank and thrift regulation and dramatically altered the FDICs operations.

The causes of this debacle and the events surrounding its resolution have been docu-

mented and analyzed in great detail by academics, governmental bodies, former bank and

thrift regulators, and journalists. Although the FDIC had a role in monitoring events as they

unfolded and, indeed, played an important part in the eventual cleanup, until 1989 S&Ls

were regulated by the Federal Home Loan Bank Board (FHLBB, or Bank Board) and in-

sured by the Federal Savings and Loan Insurance Corporation (FSLIC) within a legislative

and historical framework separate from the one that surrounded commercial banks. This

chapter provides only an overview of the savings and loan crisis during the 1980s, with an

emphasis on its relationship to the banking crises of the decade. The discussion also high-

lights the differences in the regulatory structures and practices of the two industries that af-

fected how, and how well, failing institutions were handled by their respective deposit

insurers.

A brief overview of insolvencies in the S&L industry between 1980 and 1982, caused

by historically high interest rates, is followed by a review of the federal regulatory structure

and supervisory environment for S&Ls. The governments response to the early S&L crisis

is then examined in greater detail, as are the dramatic developments that succeeded this re-

sponse. The corresponding competitive effects on commercial banks during the middle to

late 1980s are outlined. Finally, the resolution and lessons learned are summarized.

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

168 History of the EightiesLessons for the Future

1

U.S. League of Savings Institutions, Savings and Loan Sourcebook, (1982), 37. It should be noted that during the 1980s, the

state-sponsored insurance programs either collapsed or were abandoned.

2

For a discussion of these issues, see Chapter 6.

The S&L Industry, 19801982

In 1980, the FSLIC insured approximately 4,000 state- and federally chartered sav-

ings and loan institutions with total assets of $604 billion. The vast majority of these assets

were held in traditional S&L mortgage-related investments. Another 590 S&Ls with assets

of $12.2 billion were insured by state-sponsored insurance programs in Maryland, Massa-

chusetts, North Carolina, Ohio, and Pennsylvania.

1

One-fifth of the federally insured S&Ls,

controlling 27 percent of total assets, were permanent stock associations, while the remain-

ing institutions in the industry were mutually owned. Like mutual savings banks, S&Ls

were losing money because of upwardly spiraling interest rates and asset/liability mis-

match.

2

Net S&L income, which totaled $781 million in 1980, fell to negative $4.6 billion

and $4.1 billion in 1981 and 1982 (see table 4.1).

During the first three years of the decade, 118 S&Ls with $43 billion in assets failed,

costing the FSLIC an estimated $3.5 billion to resolve. In comparison, during the previous

45 years, only 143 S&Ls with $4.5 billion in assets had failed, costing the agency $306 mil-

lion. From 1980 to 1982 there were also 493 voluntary mergers and 259 supervisory merg-

ers of savings and loan institutions (see table 4.2). The latter were technical failures but

Table 4.1

Selected Statistics, FSLIC-Insured Savings and Loans, 19801989

($Billions)

Number Total Net Tangible Tangible Capital/ No. Insolvent Assets in FSLIC

Year of S&Ls Assets Income Capital Total Assets S&Ls* Insolvent S&Ls* Reserves

1980 3,993 $ 604 $ 0.8 $32 5.3% 43 $ 0.4 $ 6.5

1981 3,751 640 −4.6 25 4.0 112 28.5 6.2

1982 3,287 686 −4.1 4 0.5 415 220.0 6.3

1983 3,146 814 1.9 4 0.4 515 284.6 6.4

1984 3,136 976 1.0 3 0.3 695 360.2 5.6

1985 3,246 1,068 3.7 8 0.8 705 358.3 4.6

1986 3,220 1,162 0.1 14 1.2 672 343.1 −6.3

1987 3,147 1,249 −7.8 9 0.7 672 353.8 −13.7

1988 2,949 1,349 −13.4 22 1.6 508 297.3 −75.0

1989 2,878 1,252 −17.6 10 0.8 516 290.8 NA

* Based on tangible-capital-to-assets ratio.

Chapter 4 The Savings and Loan Crisis and Its Relationship to Banking

History of the EightiesLessons for the Future 169

Table 4.2

S&L Failures, 19801988

($Thousands)

Number of Estimated Supervisory Voluntary

Year Failures Total Assets Cost Mergers Mergers

1980 11 $ 1,348,908 $ 158,193 21 63

1981 34 19,590,802 1,887,709 54 215

1982 73 22,161,187 1,499,584 184 215

1983 51 13,202,823 418,425 34 83

1984 26 5,567,036 886,518 14 31

1985 54 22,573,962 7,420,153 10 47

1986 65 17,566,995 9,130,022 5 45

1987 59 15,045,096 5,666,729 5 74

1988 190 98,082,879 46,688,466 6 25

Sources: FDIC; and Barth, The Great Savings and Loan Debacle, 3233.

3

Tangible net worth is defined as net worth excluding goodwill and other intangible assets. In an accounting framework,

goodwill is an intangible asset created when one firm acquires another. It represents the difference between the purchase

price and the market value of the acquired firms assets. The treatment of goodwill in supervisory mergers of S&Ls is dis-

cussed in more detail below.

4

This estimate is based on the assumption that the liabilities of insolvent institutions exceeded their tangible assets by 10 per-

cent. National Commission on Financial Institution Reform, Recovery and Enforcement, Origin and Causes of the S&L De-

bacle: A Blueprint for Reform: A Report to the President and Congress of the United States (1993), 44, 79.

5

In its audit of the Resolution Trust Corporations 1994 and 1995 financial statements, the U.S. General Accounting Office

estimated the total direct and indirect cost of resolving the savings and loan crisis at $160.1 billion. This figure includes

funds provided by both taxpayers and private sources. See U.S. General Accounting Office, Financial Audit: Resolution

Trust Corporations 1995 and 1994 Financial Statements (1996), 13.

resulted in no cost to the FSLIC. Despite this heightened resolution activity, at year-end

1982 there were still 415 S&Ls, with total assets of $220 billion, that were insolvent based

on the book value of their tangible net worth.

3

In fact, tangible net worth for the entire S&L

industry was virtually zero, having fallen from 5.3 percent of assets in 1980 to only 0.5 per-

cent of assets in 1982. The National Commission on Financial Institution Reform, Recov-

ery and Enforcement estimated in 1993 that it would have cost the FSLIC approximately

$25 billion to close these insolvent institutions in early 1983.

4

Although this is far less than

the ultimate cost of the savings and loan crisiscurrently estimated at approximately $160

billionit was nonetheless about four times the $6.3 billion in reserves held by the FSLIC

at year-end 1982.

5

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

170 History of the EightiesLessons for the Future

6

William K. Black, Examination/Supervision/Enforcement of S&Ls, 19791992 (1993), 2.

7

James R. Adams referred to the FSLIC and the Bank Board as the doormats of financial regulation (The Big Fix: Inside

the S&L Scandal: How an Unholy Alliance of Politics and Money Destroyed Americas Banking System [1990], 40). See also

Martin E. Lowy, High Rollers: Inside the Savings and Loan Debacle (1991), 11112; Norman Strunk and Fred Case, Where

Deregulation Went Wrong: A Look at the Causes behind Savings and Loan Failures in the 1980s (1988), 12045; and Black,

Examination/Supervision/Enforcement.

Federal Regulatory Structure and Supervisory Environment

Federal regulation of the savings and loan industry developed under a legislative

framework separate from that for commercial banks and mutual savings banks. Legislation

for S&Ls was driven by the public policy goal of encouraging home ownership. It began

with the Federal Home Loan Bank Act of 1932, which established the Federal Home Loan

Bank System as a source of liquidity and low-cost financing for S&Ls. This system com-

prised 12 regional Home Loan Banks under the supervision of the FHLBB. The regional

Banks were federally sponsored but were owned by their thrift-institution members through

stock holdings. The following year, the Home Owners Loan Act of 1933 empowered the

FHLBB to charter and regulate federal savings and loan associations. Historically, the Bank

Board promoted expansion of the S&L industry to ensure the availability of home mortgage

loans. Finally, the National Housing Act of 1934 created the FSLIC to provide federal de-

posit insurance for S&Ls similar to what the FDIC provided for commercial banks and mu-

tual savings banks. However, in contrast to the FDIC, which was established as an

independent agency, the FSLIC was placed under the authority of the FHLBB. Therefore,

for commercial banks and mutual savings banks the chartering and insurance functions

were kept separate, whereas for federally chartered S&Ls the two functions were housed

within the same agency.

For a variety of reasons, the FHLBBs examination, supervision, and enforcement

practices were traditionally weaker than those of the federal banking agencies. Before the

1980s, savings and loan associations had limited powers and relatively few failures, and the

FHLBB was a small agency overseeing an industry that performed a type of public service.

Moreover, FHLBB examiners were subject, unlike their counterparts at sister agencies, to

stringent OMB and OPM limits on allowable personnel and compensation.

6

It should be

noted that the S&L examination process and staff were adequate to supervise the traditional

S&L operation, but they were not designed to function in the complex new environment of

the 1980s in which the industry had a whole new array of powers. Accordingly, when much

of the S&L industry faced insolvency in the early 1980s, the FHLBBs examination force

was understaffed, poorly trained for the new environment, and limited in its responsibilities

and resources.

7

Qualified examiners had been hard to hire and hard to retain (a government-

wide hiring freeze in 198081 had compounded these problems). The banking agencies

generally recruited the highest-quality candidates at all levels because they paid salaries 20

Chapter 4 The Savings and Loan Crisis and Its Relationship to Banking

History of the EightiesLessons for the Future 171

8

Black, Examination/Supervision/Enforcement, 2.

9

Ibid., 11.

to 30 percent higher than those the FHLBB could offer. In 1984, the average FHLBB ex-

aminers salary was $24,775; this figure was $30,764, $32,505, and $37,900 at the Office

of the Comptroller of the Currency, the FDIC, and the Federal Reserve Board, respectively.

8

And retention was a problem because experienced examiners were regularly recruited by

the S&L industry, which offered far greater remuneration than the FHLBB could. Further-

more, FHLBB training resources were constrained by budget limitations and by a lack of

seasoned examiners available to instruct less-experienced ones.

The Bank Boards examination and supervision functions were organized differently

from those in the banking agencies. The examinations of S&Ls were conducted completely

separately from the supervisory function. Examiners were hired by and reported to the Of-

fice of Examination and Supervision of the Bank Board (OES). The supervisory personnel,

with authority for the System, resided within the Federal Home Loan Bank System and, in

effect, reported only to the president of the local FHLB. Thus, in contrast to the banking

agencies, no agency had a single, direct line of responsibility for a troubled institution.

Regulators interviewed for this study noted that the examination philosophy was to

identify adherence to rules and regulations, not adherence to general principles of safety

and soundness. Because most S&L assets were fixed-rate home mortgages, credit-quality

problems were rare. Loan evaluations were appraisal driven, and in the past the value of

collateral had consistently appreciated. Thus, losses on home mortgages were rare, even in

the event of foreclosure. Nevertheless, not until 1987 did S&L examiners have the author-

ity either to classify assets according to likelihood of repayment or to force institutions to

reserve for losses on a timely basis. Moreover, examiner recommendations were often not

followed up by supervisory personnel.

Supervisory oversight of the S&L industry was both decentralized and split from the

examination function. The FHLBB designated each regional Federal Home Loan Bank

president as the Principal Supervisory Agent (PSA) for that region; senior Bank staff acted

as supervisory agents. However, field examiners reported to the FHLBB in Washington

rather than to the regional PSA, and the regional PSA effectively reported to no one. In fact,

according to one insider, the regional Federal Home Loan Banks operated like indepen-

dent duchies.

9

Because the regional Banks were owned by the institutions they supervised,

the potential for conflicts of interest was quite strong. In any event, supervisory agents did

not receive exam reports until after they had undergone multiple layers of reviewsome-

times months after the as of date.

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

172 History of the EightiesLessons for the Future

10

Ibid., 12.

11

They included the power to issue a cease-and-desist order (C&D) requiring an institution to cease unsafe and unsound prac-

tices or other rules violations, and the power to issue a removal-and-prohibition order (R&P) against an employee, officer,

or director, permanently removing the person from employment in the S&L industry.

12

Quoted from p. 2 of Norman Strunks memorandum to Bill OConnell, attached as exhibit 3 in Black, Examination/Super-

vision/Enforcement.

This system generated mistrust and disrespect between the S&L examiners, who were

federal employees, and the supervisory agents, who were employees of the privately owned

regional Banks. Supervisory agents and PSAs were compensated at levels far above those

of the FHLBB staff, and while examiners suspected the supervisors of being overpaid in-

dustry friends, supervisory agents and PSAs viewed the Bank Board examiners as low

paid, heavy drinking specialists in trivial details.

10

Clearly, even the most diligent S&L ex-

aminer faced considerable difficulties in reporting negative findings and in seeing those

findings acted upon.

Although the FHLBB legally had enforcement powers similar to those of the banking

agencies, it used these powers much less frequently.

11

The S&L supervisory environment

simply was not conducive to prompt corrective enforcement actions. As indicated above,

S&Ls were traditionally highly regulated institutions, and before the 1980s the industry had

exhibited few problems of mismanagement. The industrys significant involvement in its

own supervision stemmed from its favorable image and protected status with lawmakers.

As one S&L lobbyist later wrote: When we [the U.S. League of Savings Institutions] par-

ticipated in the writing of the supervisory law, hindsight shows that we probably gave the

business too much protection against unwarranted supervisory action (emphasis added).

12

Because enforcement was a lengthy process if contested by the institution, the Bank

Board preferred either to use voluntary supervisory agreements or to rely on the states to

use their powers. More important, the lack of resources and the limited number of enforce-

ment attorneys (generally only five through 1984) led the FHLBB to adopt policies that

made it unlikely an institution would contest a case. For example, enforcement staff would

compromise on the terms of a cease-and-desist order, pursue only the strongest cases, and

generallybecause of lack of precedentsavoid cases alleging unsafe and unsound prac-

tices. Unfortunately, these policies undermined the effectiveness of both contemporary and

future enforcement actions.

Government Response to Early Crisis: Deregulation

The vast number of actual and threatened insolvencies of savings and loan associa-

tions in the early 1980s was predictable because of the interest-rate mismatch of the insti-

tutions balance sheets. What followed, however, was a patchwork of misguided policies

that set the stage for massive taxpayer losses to come. In hindsight, the government proved

Chapter 4 The Savings and Loan Crisis and Its Relationship to Banking

History of the EightiesLessons for the Future 173

13

National Commission, Origins and Causes of the S&L Debacle, 32.

14

Mehles action has been described as a remarkable step (Kathleen Day, S&L Hell: The People and the Politics behind the

$1 Trillion Savings and Loan Scandal [1993], 93).

15

Sanford Rose, The Fruits of Canalization, American Banker (November 2, 1981), 1.

16

In contrast, commercial banks were required to have a percentage of assets, a larger base than insured deposits, as a capital

cushion. For the bank capital requirements, see section on capital adequacy in Chapter 2.

17

James R. Barth, The Great Savings and Loan Debacle (1991), 54.

18

National Commission, Origins and Causes of the S&L Debacle, 3536.

singularly ill-prepared to deal with the S&L crisis.

13

The primary problem was the lack of

real FSLIC resources available to close insolvent S&Ls. In addition, many government of-

ficials believed that the insolvencies were only on paper, caused by unprecedented inter-

est-rate levels that would soon be corrected. This line of reasoning complemented the view

that as long as an institution had the cash to continue to operate, it should not be closed. For-

mer Assistant Secretary of the Treasury Roger Mehle even testified to that effect when a

failed savings and loan sued the Bank Board.

14

Although Mehle maintained he was testify-

ing as a private citizen, on other occasions he did take the position that thrifts did not have

a serious problem, because their income came in the form of mortgage payments whereas

most of their expenses were in the form of interest credited to savings accounts but not

withdrawn. Mehle stated, I wish my income was in cash and my expenses in the form of

bookkeeping entries.

15

Most political, legislative, and regulatory decisions in the early 1980s were imbued

with a spirit of deregulation. The prevailing view was that S&Ls should be granted regula-

tory forbearance until interest rates returned to normal levels, when thrifts would be able to

restructure their portfolios with new asset powers. To forestall actual insolvency, therefore,

the FHLBB lowered net worth requirements for federally insured savings and loan associ-

ations from 5 percent of insured accounts to 4 percent in November 1980 and to 3 percent

in January 1982.

16

At the same time, the existing 20-year phase-in rule for meeting the net

worth requirement, and the 5-year-averaging rule for computing the deposit base, were re-

tained. The phase-in rule meant that S&Ls less than 20 years old had capital requirements

even lower than 3 percent. This made chartering de novo federal stock institutions very at-

tractive because the required $2.0 million initial capital investment could be leveraged into

$1.3 billion in assets by the end of the first year in operation.

17

The 5-year-averaging rule,

too, encouraged rapid deposit growth at S&Ls, because the net worth requirement was

based not on the institutions existing deposits but on the average of the previous five

years.

18

Reported capital was further augmented by the use of regulatory accounting principles

(RAP) that were considerably more lax than generally accepted accounting principles

(GAAP). However, where GAAP was more lenient than RAP, the Bank Board adopted the

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

174 History of the EightiesLessons for the Future

19

Supervisory goodwill was created when a healthy S&L acquired an insolvent one, with or without financial assistance from

the FSLIC. It is known as supervisory goodwill because the FHLBB allowed it to be included as an asset for capital pur-

poses. For a more in-depth discussion of goodwill accounting, see National Commission, Origins and Causes of the S&L

Debacle, 3839, and Lowy, High Rollers, 3841.

20

An example of a typical transaction will help to explain the relevance of this change. The assets and liabilities of the thrift

would be marked-to-market, and since interest rates were very high, this usually resulted in the mortgage assets of the

thrift being valued at a discount. For example, a $100,000 loan paying 8 percent might have been marked down to $80,000

so that it was paying a market rate. However, the liabilities of the institution were generally valued at near book, so a

$100,000 deposit was still worth $100,000. Even if the acquirer paid nothing for the thrift, the acquirer was taking on an as-

set worth $80,000 and a liability of $100,000, a $20,000 shortfall. This would be recorded as an asset called goodwill with

a value of $20,000. One should note that the borrower would still have a $100,000 loan outstanding and would be expected

to pay back the entire loan balance. The $20,000 would be booked as an off-balance-sheet item called a discount. The ac-

counting profession considered the goodwill and the discount two independent entries.

After the merger, the goodwill would be amortized as an expense over a set period. The discount would be accreted

to income over the life of the loan, usually around 10 years. Under RAP accounting, before June 1982, goodwill was amor-

tized over the same 10-year period. Afterward, the accounting picture changed dramatically. Under GAAP, the goodwill

could be amortized over as many as 40 years. The expenses for the amortization of goodwill would be much lower than the

income from the accretion of the discount for many years. This allowed thrift institutions to literally manufacture earn-

ings and capital by acquiring other thrift institutions (Office of Thrift Supervision Director Timothy Ryan, testifying be-

fore the U.S. House Committee on Banking, Finance and Urban Affairs, Subcommittee on General Oversight and

Investigations, Capital Requirements for Thrifts As They Apply to Supervisory Goodwill: Hearing, 102d Cong., 1st sess.,

1991, 31).

former. As of September 1981, troubled S&Ls could issue income capital certificates that

the FSLIC purchased with cash, or more likely with notes, and they were included in net

worth calculations. That same month, the FHLBB began permitting deferred losses on the

sale of assets when the loss resulted from adverse changes in interest rates. Thrifts were al-

lowed to spread the recognition of the loss over a ten-year period, while the unamortized

portion of the loss was carried as an asset. Then in late 1982, the FHLBB began counting

appraised equity capital as a part of reserves. Appraised equity capital allowed S&Ls to rec-

ognize an increase in the market value of their premises.

Perhaps the most far-reaching regulatory change affecting net worth was the liberal-

ization of the accounting rules for supervisory goodwill.

19

Effective in July 1982, the Bank

Board eliminated the existing ten-year amortization restriction on goodwill, thereby allow-

ing S&Ls to use the general GAAP standard of no more than 40 years in effect at the time.

This change was intended to encourage healthy S&Ls to take over insolvent institutions,

whose liabilities far exceeded the market value of their assets, without the FSLICs having

to compensate the acquirer for the entire negative net worth of the insolvent institution.

20

Not surprisingly, between June 1982 and December 1983 goodwill rose from a total of $7.9

billion to $22 billion, the latter amount representing 67 percent of total RAP capital. The

FHLBB also actively encouraged use of this accounting treatment as a low-cost method of

Chapter 4 The Savings and Loan Crisis and Its Relationship to Banking

History of the EightiesLessons for the Future 175

21

Recognizing that the use of supervisory goodwill had contributed to the magnitude of the thrift crisis, Congress legislated

a five-year phaseout of goodwill that had been created on or before April 12, 1989. This change, and tighter capital re-

quirements for thrifts, rapidly forced a number of S&Ls into insolvency or near-insolvency. Many of these institutions sued

the federal government, and on July 1, 1996, the Supreme Court ruled in favor of three of them in United States v. Winstar

Corp. See, for example, Linda Greenhouse, High Court Finds Rule Shift by U.S. Did Harm to S&Ls, The New York Times

(July 2, 1996), A3; and Paul M. Barrett, High Court Backs S&Ls on Accounting, Declines to Hear Affirmative-Action

Case, The Wall Street Journal (July 2, 1996), 1.

22

National Commission, Origins and Causes of the S&L Debacle, 37.

23

In addition, the Economic Recovery Tax Act of 1981 contributed to the boom in commercial real estate projects. For a de-

tailed description of all of these laws, see Chapters 2 and 3.

24

Public Law 97-320, § 202(d).

resolving troubled institutions. Unfortunately, like other Bank Board policies that resulted

in the overstatement of capital, the liberal treatment of supervisory goodwill restricted the

FHLBBs ability to crack down on thinly capitalized or insolvent institutions, because en-

forcement actions were based on regulatory and not tangible capital.

21

The Bank Board also attempted to attract new capital to the industry, and it did so by

liberalizing ownership restrictions for stock-held institutions in April 1982. That change

proved to have a dramatic effect on the S&L industry.

22

Traditionally, federally chartered

stock associations were required to have a minimum of 400 stockholders. No individual

could own more than 10 percent of an institutions outstanding stock, and no controlling

group more than 25 percent. Moreover, 75 percent of stockholders had to reside or do busi-

ness in the S&Ls market area. The elimination of these restrictions, coupled with the re-

laxed capital requirements and the ability to acquire an institution by contributing in-kind

capital (stock, land, or other real estate), invited new owners into the industry. With a min-

imal amount of capital, an S&L could be owned and operated with a high leverage ratio and

in that way could generate a high return on capital.

Legislative actions in the early 1980s were designed to aid the S&L industry but in

fact increased the eventual cost of the crisis. The two principal laws passed were the De-

pository Institutions Deregulation and Monetary Control Act of 1980 (DIDMCA) and the

GarnSt Germain Depository Institutions Act of 1982 (GarnSt Germain).

23

DIDMCA re-

duced net worth requirements and GarnSt Germain wrote capital forbearance into law.

DIDMCA replaced the previous statutory net worth requirement of 5 percent of insured ac-

counts with a range of 36 percent of insured accounts, the exact percentage to be deter-

mined by the Bank Board. GarnSt Germain went even further in loosening capital

requirements for thrifts by stating simply that S&Ls will provide adequate reserves in a

form satisfactory to the Corporation [FSLIC], to be established in regulation made by the

Corporation.

24

GarnSt Germain also authorized the FHLBB to implement a Net Worth

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

176 History of the EightiesLessons for the Future

25

The National Commission attributed the greater success of the FDICs forbearance policy to several factors, including a

more limited use of accounting gimmicks and growth restrictions for savings banks (National Commission, Origins and

Causes of the S&L Debacle, 32, 37). For a comparison of the two Net Worth Certificate Programs, see U.S. General Ac-

counting Office, Net Worth Certificate Programs: Their Design, Major Differences, and Early Implementation (1984).

26

For details on the debate over deregulation, see Chapter 6.

27

Moral hazard refers to the incentives that insured institutions have to engage in higher-risk activities than they would

without deposit insurance; deposit insurance means, as well, that insured depositors have no compelling reason to monitor

the institutions operations. The National Commission on Financial Institution Reform, Recovery and Enforcement con-

cluded that federal deposit insurance at institutions with substantial risk was a fundamental condition necessary for col-

lapse and that [r]aising the insurance limit from $40,000 to $100,000 exacerbated the problem (National Commission,

Origins and Causes of the S&L Debacle, 56). For further discussion of the increase in the deposit insurance limit, see

Chapter 2.

28

Lawrence J. White, The S&L Debacle: Public Policy Lessons for Bank and Thrift Regulation (1991), 73.

Certificate Program for S&Ls. (Ironically, this form of capital forbearance was used more

extensively and more effectively by the FDIC for mutual savings banks.)

25

These two laws also made a number of other significant changes affecting thrift insti-

tutions, including giving them new and expanded investment powers and eliminating de-

posit interest-rate ceilings. But although such deregulation had been recommended since

the early 1970s,

26

when finally enacted it failed to give attention to corresponding recom-

mendations for deposit insurance reform and stronger supervision. Particularly dangerous

in view of these omissions were the expanded authority of federally chartered S&Ls to

make acquisition, development, and construction (ADC) loans, enacted in DIDMCA, and

the subsequent elimination in GarnSt Germain of the previous statutory limit on loan-to-

value ratios. These changes allowed S&Ls to make high-risk loans to developers for 100

percent of a projects appraised value.

DIDMCA also increased federal deposit insurance to $100,000 per account, a major

adjustment from the previous limit of $40,000 per account. The increase in the federal de-

posit insurance level and the phaseout of deposit interest-rate controls were designed to al-

leviate disintermediation, or the flow of deposits out of financial institutions into money

market mutual funds and other investments. However, the increase in insured liabilities

added substantially to the potential costs of resolving failed financial institutions, and has

been cited as exacerbating the moral-hazard problem much discussed throughout the

1980s.

27

Deregulation of asset powers at the federal level prompted a number of states to enact

similar, or even more liberal, legislation. This competition in laxity has been attributed to

a conscious effort by state legislatures to retain and attract state-chartered institutions that

otherwise might apply for federal charters, thereby reducing the statesregulatory roles and

fee collections.

28

An oft-cited example is Californias Nolan bill, enacted in 1982 after

Chapter 4 The Savings and Loan Crisis and Its Relationship to Banking

History of the EightiesLessons for the Future 177

29

From 1980 to 1982 the number of state-chartered S&Ls in California fell from 126 with $82 billion in assets to 107 with

less than $30 billion (Barth, The Great Savings and Loan Debacle, 55). Day notes that funding for Californias supervi-

sory department diminished proportionatelystaff fell from 178 in 1978 to only 44 in 1983 (Day, S&L Hell, 124).

30

Strunk and Case, Where Deregulation Went Wrong, 59, and for examples of liberal state laws, 6066.

31

For a discussion of Reaganomics and the early years of the thrift crisis, see Day, S&L Hell, 7381; and Lowy, High Rollers,

2026.

32

Strunk and Case, Where Deregulation Went Wrong, 141. It is important to note, as discussed in Chapter 12, that the bank-

ing agencies themselves believed the number of exams could be reduced through greater reliance on computers and off-site

monitoring.

many of the states largest thrifts converted to federal charters.

29

Effective January 1, 1983,

state-chartered S&Ls in California had unlimited authority to invest in service corporations

and in real estate. Another state notable for its liberalizing legislation was Florida, whose

state-chartered thrift industry was virtually nonexistent before the enactment of a series

of liberal laws between 1980 and 1984.

30

Supervision of these institutions remained under

the states controller and remained weak. California and Florida, along with Texas, had

some of the nations most liberal state laws for thrifts. Unfortunately, as is detailed below,

the more liberal powers afforded by some states to their S&Ls added significantly to the

losses that eventually had to be made good by the federal government.

Finally, it should be noted that the Reagan administration was more directly involved

with the regulation of S&Ls than with the regulation of the banking industry. In other

words, the FDIC and the Federal Reserve System traditionally had more political indepen-

dence than the FHLBB (and therefore than the FSLIC). During the early years of the ad-

ministration, responsibility for the unfolding thrift crisis lay with the Cabinet Council on

Economic Affairs, chaired by Treasury Secretary Donald Regan. Its members included se-

nior officials from OMB and the White House. Firm believers in Reaganomics, this

group crafted the policies of deregulation and forbearance and adamantly opposed any gov-

ernmental cash expenditures to resolve the S&L problem.

31

Furthermore, the administration

did not want to alarm the public unduly by closing a large number of S&Ls. Therefore, the

Treasury Department and OMB urged the Bank Board to use FSLIC notes and other forms

of forbearance that did not have the immediate effect of increasing the federal deficit.

The free-market philosophy of the Reagan administration also called for a reduction

in the size of the federal government and less public intervention in the private sector. As a

result, during the first half of the 1980s the federal banking and thrift agencies were en-

couraged to reduce examination staff, even though these agencies were funded by the insti-

tutions they regulated and not by the taxpayers. This pressure to downsize particularly

affected the FHLBB, whose budget and staff size were closely monitored by OMB and sub-

jected to the congressional appropriations process.

32

The free-market philosophy affected

not only regulatory and supervisory matters but also thrift and bank chartering decisions.

Before the 1980s, new charters had been granted on the basis of community need. Under the

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

178 History of the EightiesLessons for the Future

33

Day, S&L Hell, 100. For further discussion of these issues, see Chapter 2, the section on entry.

34

National Council of Savings Institutions, 1986 National Fact Book of Savings Institutions (1986), 10, 16; and FDIC, His-

torical Statistics on Banking: A Statistical History of the United States Banking Industry 19341992 (1993), 21921.

Reagan administration, the FHLBB and the Office of the Comptroller of the Currency ap-

proved any application as long as the owners hired competent management and provided

a sound business plan.

33

The devastating consequences of adding many new institutions to

the marketplace, expanding the powers of thrifts, decontrolling interest rates, and increas-

ing deposit insurance coverage, coupled with reducing regulatory standards and scrutiny,

were not foreseen.

Developments after Deregulation

The savings and loan industry changed swiftly and dramatically after the deregulation

of asset powers and interest rates. The period from year-end 1982 to year-end 1985 was

characterized by extremely rapid growth, as the industry responded to the new regulatory

and legislative climate. Total S&L assets increased from $686 billion to $1,068 billion, or

by 56 percentmore than twice the growth rate at savings banks and commercial banks

(approximately 24 percent). As discussed below, S&L growth was fueled by an influx of de-

posits (often via money brokers) into institutions willing to pay above-market interest rates.

In 1983 and 1984, more than $120 billion in net new money flowed into savings and loan

associations.

34

With money flowing so plentifully, risk takers gravitated toward the S&L industry, al-

tering ownership characteristics. Although more than a few of these new owners engaged in

Table 4.3

Number of Newly Chartered FSLIC-Insured S&Ls, 19801986

Year State-Chartered Federally Chartered Total

1980 63 5 68

1981 21 4 25

1982 23 3 26

1983 36 11 47

1984 68 65 133

1985 45 43 88

1986 13 14 27

TOTAL 348 144 492

Source: Lawrence White, The S&L Debacle, 106.

Note: Excludes state-chartered thrifts that converted from state-sponsored insurance funds to the FSLIC.

Chapter 4 The Savings and Loan Crisis and Its Relationship to Banking

History of the EightiesLessons for the Future 179

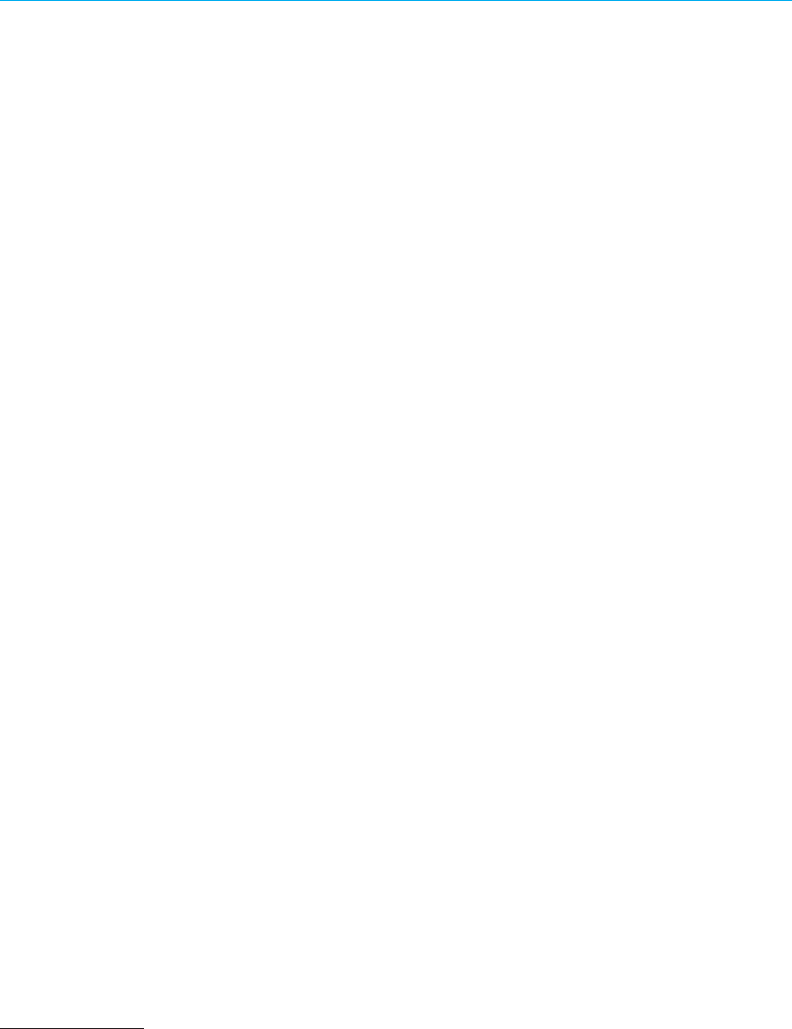

Figure 4.1

PercentageofS&L Assets in Mortgage Loans,

1978–1986

1978 1979 1980 1981 1982 1983 1984 1985 1986

60

70

80

Percent

highly publicized cases of fraudulent activity, many others were just greedy.

35

Sharp entre-

preneurs realized the large potential profit from owning an S&L, whose charter now al-

lowed a wide range of investment opportunities without the corresponding regulation of

commercial banks. Little capital was required to purchase or start an S&L, and the growth

potential was great. A variety of nonbankers entered the S&L industry, ranging from den-

tists, with no experience in owning financial institutions, to real estate developers, who had

serious conflicts of interest. To gain entry into the S&L industry, one either acquired control

of existing institutions (many of which had converted from mutual to stock) or started de

novo institutions. Between 1980 and 1986 nearly 500 new S&L charters were issued (see

table 4.3), with more than 200 of these issued in just two years1984 and 1985. In 1981

stock S&Ls had constituted 21 percent of the industry; in 1986 they constituted 38 percent

and controlled 64 percent of the industrys total assets.

Another major change resulting from deregulation was that, beginning in 1982, S&L

investment portfolios rapidly shifted away from traditional home mortgage financing and

into new activities. This shift was made possible by the influx of deposits and also by sales

of existing mortgage loans. By 1986, only 56 percent of total assets at savings and loan as-

sociations were in mortgage loans, compared with 78 percent in 1981 (see figure 4.1). In

35

National Commission, Origins and Causes of the S&L Debacle, 47.

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

180 History of the EightiesLessons for the Future

36

In January 1985, the Bank Board adopted a rule restricting direct investments by FSLIC-insured thrifts to 10 percent of as-

sets unless permission was granted to exceed that level.

37

National Commission, Origins and Causes of the S&L Debacle, 43.

38

See, for example, Strunk and Case, Where Deregulation Went Wrong, 5760; National Commission, Origins and Causes of

the S&L Debacle, 48; and Day, S&L Hell, 124.

39

White, The S&L Debacle, 8990.

40

One of the major themes of Martin Lowys book (High Rollers) is that thrifts were able to buy political favor in order to

keep regulators from interfering in their operations.

some states, direct investments in real estate, equity securities, service corporations, and op-

erating subsidiaries were allowed with virtually no limitations.

36

S&Ls invested in every-

thing from casinos to fast-food franchises, ski resorts, and windmill farms. Other new

investments included junk bonds, arbitrage schemes, and derivative instruments. It is im-

portant to note, however, that while windmill farms and other exotic investments made for

interesting reading, high-risk development loans and the resultant mortgages on the same

properties were most likely the principal cause for thrift failures after 1982. A large per-

centage of S&L assets was devoted to acquisition, development, and construction (ADC)

loans; these were very attractive because of their favorable accounting treatment and the

potential for future profit if the projects were successful. As discussed below, the entry of

so many S&Ls into commercial real estate lending helped fuel boom-to-bust real estate cy-

cles in several regions of the country.

In 1983, even when a sharp drop in interest rates returned many traditional S&Ls to

profitability, 10 percent of the industry was still insolvent on a GAAP basis and 35 percent

of the industrys assets were controlled by S&Ls that were insolvent on a tangible basis

yet these institutions were permitted to grow along with the rest of the industry, and to sub-

stitute credit risk for interest-rate risk. The high-growth period between 1982 and 1985 was

also the period when examination and supervision were weakest.

37

States that had enacted

liberal S&L laws, such as California, Florida, and Texas, were soft on supervision; and in

some cases, state-chartered institutions had close political ties to elected officials and to a

states regulators.

38

In the Southwest, existing weaknesses in the Bank Boards supervision

of federally chartered S&Ls were compounded by the relocation in September 1983 of the

Ninth District of the Federal Home Loan Bank System from Little Rock, Arkansas, to Dal-

las, Texas. The number of examinations in the district fell by one-third and remained low

during the critical years of 1984 and 1985.

39

Moreover, after it was realized in 1984 that a

number of fast-growing S&Ls were dangerously abusing their new powers, the FHLBBs

attempts to crack down were bitterly opposed by the industry, the administration, and those

key members of Congress who had been persuaded by S&L operators and real estate de-

velopers that regulators had become Gestapo-like and heavy-handed.

40

Nevertheless,

in late 1984 the Bank Board began to tighten the S&L regulatory system by imposing a

number of regulations designed to (a) curb rapid growth and direct investments by thrifts

Chapter 4 The Savings and Loan Crisis and Its Relationship to Banking

History of the EightiesLessons for the Future 181

41

For a chronological listing of these regulations, see, for example, National Commission, Origins and Causes of the S&L De-

bacle, 9899; and Barth, The Great Savings and Loan Debacle, 13032, 13741.

42

For a listing of RAP-insolvent and tangible-insolvent thrifts from 1981 to 1987, see White, The S&L Debacle, 114.

43

Eugenie D. Short and Kenneth J. Robinson, Deposit Insurance Reform in the Post-FIRREA Environment: Lessons from the

Texas Deposit Market, Federal Reserve Bank of Dallas Financial Industry Studies Working Paper (December 1990), 3.

with low net worth, (b) increase net worth standards, and (c) reform accounting practices.

41

In 1985, the FHLBB took the unusual step of transferring its examination staff to the Fed-

eral Home Loan Banks in order to become independent of OMBs restrictions on pay and

staffing levels.

Although these measures would help control future abuses, they could not reverse the

losses already incurred and those that would soon result from rapid declines in overbuilt

real estate markets. Furthermore, the FHLBB was trapped by its own policies: the agency

had to wait until an institution was insolvent under the relatively lax RAP before taking ac-

tion, and accounting distortions favored high-growth S&Ls that continued to report healthy

returns on assets and regulatory net worth. Independent of these problems, the FSLIC, with

reserves of only $5.6 billion at year-end 1984, did not have the resources to close even the

RAP-insolvent institutions, which at that time numbered 71 with assets of $14.8 billion.

42

Within two years, these figures had ballooned to 225 institutions with assets of $68.1 bil-

lion, largely as a result of the deflated southwestern economy. The Southwests problems

caused severe losses in the commercial banking industry as well (and are discussed in

Chapter 9). In fact, the unfolding S&L crisis in general, not just in the Southwest, negatively

affected the banking industry.

Competitive Effects on the Banking Industry

Enactment of GarnSt Germain and the deregulation of asset powers by several key

states led many S&Ls to change their operating strategies. These changes substantially in-

tensified the competitive environment of commercial banks and placed downward pressure

on bank profitability. Although in a free-market economy competition is normally consid-

ered healthy, regulatory forbearance in the thrift industry and moral hazard created market -

place distortions that penalized well-run financial institutions.

43

On the liability side of the

balance sheet, the bidding up of deposit interest rates by aggressive and/or insolvent S&Ls

increased the cost of funds, adversely affecting both commercial banks and conservatively

run thrifts. On the asset side of the balance sheet, commercial banks were negatively influ-

enced by the entrance of inexperienced and, in some cases, rogue S&Ls into commercial

and real estate lending.

The genesis of the bidding up of deposit interest rates was the S&L industrys dra-

matic growth between 1982 and 1985. This growth was facilitated by a flood of deposits

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

182 History of the EightiesLessons for the Future

44

In a repurchase agreement, a thrift would sell mortgages or mortgage-backed securities to an investment banking firm and

promise to repurchase them at a future date and higher price. These transactions were essentially collateralized borrow-

ing (White, The S&L Debacle, 88).

45

Strunk and Case, Where Deregulation Went Wrong, 105.

46

It should be noted that not all highfliers were located in Texas. American Diversified Savings Bank of Lodi, California,

grew from $11 million in 1982 to $978 million in 1985, while Bloomfield Savings and Loan of Birmingham, Michigan,

grew during the same period from $2 million to $676 million.

47

Lowy, High Rollers, 105, 127.

48

The MCP was designed to remove owners and managers of the worst-run insolvent institutions. Essentially, the FHLBB

would structure a pass-through receivership, recharter the S&L as a federal mutual association, and consign a group of man-

agers to run it. Between 1985 and 1988, the Bank Board placed over 100 S&Ls in the program.

into institutions willing to pay above-market interest rates to attract money to invest in new

activities. S&Ls would advertise their rates both locally and nationally, use in-house

money desks, or get in touch with brokerage firms that were happy to help move money

in large bundles to thrifts that were seeking to grow. In June 1984, when thrifts with annual

growth rates of less than 15 percent had more than 80 percent of their liabilities in tradi-

tional retail deposits (generally in accounts of less than $100,000), the comparable figure

for thrifts growing at rates in excess of 50 percent per year was only 59 percent. This latter

group relied more heavily on large-denomination deposits and repurchase agreements,

which together accounted for more than 28 percent of their liabilities.

44

Growth among thrifts was particularly strong in the Sunbelt and in states whose

economies were energy related and booming in the early 1980s. These included Arizona,

Arkansas, California, Kansas, Oklahoma, and Texas. Texas S&Ls were among the most ag-

gressive growers. Assets at the states thrifts increased by 117 percent between 1982 and

1985, a rate twice the national average.

45

This growth was concentrated in a number of

small but fast-growing institutions known as highfliers. One of the most egregious of these,

Empire Savings & Loan Association of Mesquite, grew between 1981 and 1983 from ap-

proximately $13 million in assets to more than $300 million.

46

When Empire failed in

March 1984, large certificates of deposit accounted for more than 90 percent of liabilities.

To attract this hot money, Empire and other Texas S&Ls paid about 100 basis points (1

percent) more than commercial banks for certificates of deposit.

47

After Empire Savings & Loan failed, the FHLBB imposed a regulation restricting

growth at undercapitalized thrifts to a rate equal to the interest credited on existing deposits.

S&Ls that met their net worth requirements could not grow at rates exceeding 25 percent

per year without supervisory approval. As a result, industry-wide asset growth dropped

from nearly 20 percent in 1984 to less than 10 percent in 1985. However, additional pres-

sure on deposit interest rates came from thrifts that were insolvent but still operating, such

as those in the FHLBBs Management Consignment Program (MCP).

48

For as the true con-

Chapter 4 The Savings and Loan Crisis and Its Relationship to Banking

History of the EightiesLessons for the Future 183

49

Elijah Brewer and Thomas H. Mondschean (The Impact of S&L Failures and Regulatory Changes on the CD Market, 1987-

1991) noted a significant relationship between deposit interest-rate premiums (that is, the spread over comparable Treasury

bill rates) and the capital-to-assets ratio and measures of S&L risk exposure for both wholesale and retail deposits. In the

case of wholesale deposits (over $100,000), the premium was attributed to risk compensation for uninsured depositors. In

the case of retail or fully insured deposits, the premium was attributed to moral hazard, or the incentive for insolvent

S&Ls, with nothing to lose, to bid up rates in a gamble for resurrection.

50

The Federal Reserve Bank of Dallas published several studies on the Texas premium. See, for example, Eugenie D. Short

and Jeffery W. Gunther, The Texas Thrift Situation: Implications for the Texas Financial Industry (1988).

51

Texas Marketers Battle High Rates and Bad Publicity, Savings Institutions (September 1988): 84.

52

Short and Robinson, Deposit Insurance Reform in the Post-FIRREA Environment, 10.

53

The Southwest Plan sought to consolidate and shrink the Texas thrift industry by allowing groups of insolvent thrifts to be

acquired. To conserve cash, the FSLIC used notes and other forms of future payments, such as yield maintenance and cap-

ital loss coverage. The FSLIC also heavily advertised the tax advantages of acquiring an insolvent thrift before the end of

1988, when the law allowing S&L losses to offset other taxes would expire. The Southwest Plan became controversial be-

cause for wealthy acquirers it allowed substantial tax benefits to accrue but required little capital investment.

dition of the S&L industry became common knowledge, these institutions had to pay higher

rates than solvent institutions to attract and retain deposits.

49

Because Texas S&Ls had been among the most aggressive growers, the situation there

was particularly acute. By year-end 1987, insolvent Texas S&Ls accounted for 44 percent

of the assets in all RAP-insolvent S&Ls in the country, and the unprofitable Texas thrifts ac-

counted for 62 percent of all losses nationwide. The troubled condition of the states thrift

industry resulted in higher interest rates for all financial institutions in Texas: to maintain

their funding base, even well-capitalized banks and thrifts had to pay the so-called Texas

premium, estimated to be 50 basis points or more.

50

The ensuing bidding wars between sol-

vent and insolvent financial institutions resulted in a situation that was just out of control,

according to a Texas thrift executive.

51

The higher operating expenses associated with the

Texas premium not only increased the cost of resolving insolvent S&Ls but also weakened

the financial condition of healthier institutions.

Deposit premiums paid by Texas banks and thrifts peaked in mid-1987 and declined

thereafter in response to regulatory actions to resolve troubled institutions, so that by year-

end 1989, the average cost of deposits at Texas banks was only eight basis points higher

than in the rest of the United States.

52

One of those regulatory actions was a program that

the Federal Home Loan Bank of Dallas initiated in 1988 replacing high-cost deposits in in-

solvent Texas thrifts with lower-cost deposits gathered from solvent thrifts. Another was the

FHLBBs merging of some of the top rate payers as part of its Southwest Plan.

53

However,

because of continuing uncertainty about the FSLICs ability to close insolvent thrifts, the

deposit premium for these institutions rose throughout 1989, until Congress passed the Fi-

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

184 History of the EightiesLessons for the Future

54

The U.S. General Accounting Office declared the FSLIC insolvent on the basis of its contingent liabilities at year-end 1986.

In 1987, Congress passed the Competitive Equality Banking Act of 1987, which authorized the FSLIC to borrow up to

$10.825 billion but placed a $3.75 billion limit on borrowing in any 12-month period. For a discussion of this legislation,

see White, The S&L Debacle, 102103.

55

Ibid.

56

These topics are discussed in greater detail in Chapters 3 and 9.

57

William K. Black, Cash Cow Examples (1993).

58

Lowy, High Rollers, 77.

nancial Institutions Reform, Recovery, and Enforcement Act of 1989 (FIRREA).

54

Once

regulators had the money to pay down high-cost deposits and take over insolvent institu-

tions, deposit premiums quickly declined.

After deregulation, commercial banks also faced competitive pressure from S&Ls on

the asset side of the balance sheet. Much of the growth in S&L assets between 1982 and

1985 was concentrated in commercial real estate lending. During that period the proportion

of total thrift assets invested in commercial mortgage loans and land loans rose from 7.4

percent to 12.1 percentan increase of $78.6 billion. By June 1984 aggressive thrifts,

growing at annual rates greater than 50 percent, already had 16.6 percent of their assets in

these two categories.

55

Real estate lending and investing were potentially very lucrative for

S&Ls. Changes in the federal tax code for real estate investments in 1981 and favorable ex-

pectations regarding oil prices led to a boom in commercial real estate projects, especially

in the Southwest.

56

Because S&Ls were allowed to take an equity interest in real estate de-

velopment projects, they stood to share in the upside of a booming market. Additionally, in-

terest rates on construction loans are much higher than on other forms of lending; and

regulatory accounting practices allowed S&Ls to book loan origination fees as current in-

come, even though these amounts were actually included in the loan to the borrower. For

example, a borrower might have requested a $1 million loan for two years for a housing de-

velopment; the institution might have charged four points for the original loan and 12 per-

cent annual interest. However, instead of requiring the borrower to pay the interest

($240,000) and the fee ($40,000), the S&L would have included these two items in the orig-

inal amount of the loan (which would have increased to $1.28 million), and paid the insti-

tution out of the loan proceeds.

There are many notorious examples of how this system was abused by unscrupulous

S&L owners reporting high current income on ADC loans while milking the institution of

cash in the form of dividends, high salaries, and other benefits.

57

A rapidly growing S&L

could hide impending defaults and losses by booking new ADC loans. The rush into con-

struction lending by S&Ls was such that among the fastest growers, loan fees accounted

for substantially all net income in the crucial years 1983 and 1984.

58

Moreover, although

the majority of S&Ls were not fraud-ridden, few had the management expertise necessary

Chapter 4 The Savings and Loan Crisis and Its Relationship to Banking

History of the EightiesLessons for the Future 185

59

Strunk and Case, Where Deregulation Went Wrong, 101.

60

Most accounts of the S&L debacle have noted this trend. It has been variously attributed to inexperience, fraud, rapid

growth, and the need to invest in high-risk ventures due to higher money costs.

61

Changes in commercial bank underwriting standards during the 1980s are discussed in greater detail in Chapter 3.

62

Eric I. Hemel, Deregulation and Supervision Go Together, Outlook of the Federal Home Loan Bank System (Novem-

ber/December 1985): 10.

63

Mindy Fetterman, NCNB Chairman Hugh McColl Touts His High-Rises Success, Despite Bankings Towering Real-

Estate Woes, USA Today (May 28, 1991), 1B.

for dealing with the new lending opportunities, particularly the inherently risky ADC lend-

ing. In many cases, prudent underwriting standards were not observed, and the necessary

documents and controls were not put in place. Lending on construction projects was ap-

praisal driven and was often based on the overly optimistic assumption that property val-

ues would continue to rise.

59

S&Ls sometimes loaned the entire amount up front, including

interest, fees, and even payments to developers, but did not check to ensure that projects

were being completed as planned. Moreover, S&L ADC loans frequently were nonre-

course: the borrower was not required to sign a legally binding personal guarantee.

S&Ls entered the commercial real estate lending arena at a time when banks were in-

creasing their own investments in commercial real estate loans, having lost many of their

traditional corporate clients to the commercial-paper and bond markets. At the same time,

chartering activity of de novo banks and thrifts was high. The result was simply a matter of

too many lenders chasing too few loans. The rush of new competitors, all eager to lend to

developers, had a negative effect on existing commercial banks, on their underwriting stan-

dards, and on the quality of their loans. Field examiners and bank regulators have noted that

in the 1980s borrowers could generate bidding wars between banks and S&Ls. Everyone

wanted to lend money and everyone wanted to grow. Although for the most part S&Ls lent

to lesser-qualified borrowers,

60

their presence in the marketplace contributed to the overall

decline in bank lending standards during the 1980s.

61

As S&Ls used lax underwriting stan-

dards to lure customers away from commercial banks, the banks began to imitate such S&L

practices as the up-front fee structure, interest reserves, and the small amount of equity in-

vestment by developers. This contamination effect has been called a variation of Gre-

shams Law that bad money drives out good. In this variation, risk-hungry institutions will

force careful institutions into taking greater risks as well.

62

Or in the words of Hugh Mc-

Coll, chairman of NCNB (now NationsBank): We may have the wisest underwriting pol-

icy (for loans) in the world. But if your next-door neighbor has a poor policy, it can cause

oversupply of space and crush even your wisest decision.

63

Competitive pressures from S&Ls were felt most acutely in states with a large num-

ber of aggressive and/or insolvent thrifts. Interviews with regional supervisory personnel

have indicated that Arizona, California, Florida, and Texas were states where banks were

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

186 History of the EightiesLessons for the Future

64

See Jennifer L. Eccles and John P. OKeefe, Understanding the Experience of Converted New England Savings Banks,

FDIC Banking Review 8, no. 1 (1995): 117. The New England crisis is also discussed in Chapter 10.

65

For a detailed summary of the laws provisions, see Encyclopedia of Banking and Finance, ed. Charles J. Woelfel, 10th ed.

(1994), 44652. For a review and critique of FIRREA, see also White, The S&L Debacle, 17693.

particularly affected by S&L lending practices. Additionally, the flood of mutual-to-stock

conversions of savings banks in New England during the middle to late 1980s contributed

to the boom-to-bust real estate cycle there.

64

Clearly, competition from savings and loans

did not cause the various crises experienced by the commercial banking industry during the

1980s; these crises would have occurred regardless of the thrift situation. But the channel-

ing of large volumes of deposits into high-risk institutions that speculated in real estate de-

velopment did create marketplace distortions. These high-risk, speculating institutions

raised the cost of funds marketwide and encouraged risk taking by competitors. The flow of

capital was directed to geographic areas, like Texas, where real estate was being developed

far beyond the markets ability to absorb it. This oversupply contributed to the eventual bust

in real estate values and slowed economic recovery. In hindsight, the go-go mentality in

certain regions of the country during the 1980s affected not only banks and S&Ls but also

their regulators, who were slow to understand that some markets were being extravagantly

overbuilt.

Resolution of the Crisis

Throughout the decade, losses in the S&L industry continued to mount as the decline

in real estate values deepened and affected various regions of the country. Efforts to recap-

italize the FSLIC in 1986 and 1987 were bitterly fought by the industry, which had consid-

erable influence with members of Congress. Although the Competitive Equality Banking

Act of 1987 provided the FSLIC with resources to resolve insolvent institutions, the amount

was clearly inadequate. Nevertheless, under the new FHLBB chairman, Danny Wall, the

FSLIC resolved 222 S&Ls, with assets of $116 billion, in 1988. These transactions were ef-

fected with minimal cash outlays and maximum use of notes, guarantees, and tax advan-

tages, all of which made these transactions more expensive than they would have been had

the FSLIC had adequate funds. But despite these resolutions, at year-end 1988 there were

still 250 S&Ls, with $80.8 billion in assets, that were insolvent based on regulatory ac-

counting principles. Resolution of the S&L crisis did not really begin until February 6,

1989, when newly inaugurated President George Bush announced his proposed program,

whose basic components were enacted later that year in FIRREA.

65

It is amazing that such

a monumental crisis, and one given top priority by the new administration, had been virtu-

ally ignored as an issue during the 1988 presidential campaign. This invisibility has been at-

tributed partly to Chairman Walls successful effort to downplay the problem during 1988,

partly to the continued reluctance to admit that taxpayer dollars would be required, and

Chapter 4 The Savings and Loan Crisis and Its Relationship to Banking

History of the EightiesLessons for the Future 187

66

Day, S&L Hell, 29596.

67

U.S. General Accounting Office, Financial Audit, 13.

partly to the fact that members of both political parties were vulnerable to criticism for their

role in the crisis.

66

It must be concluded that the savings and loan crisis reflected a massive public policy

failure. The final cost of resolving failed S&Ls is estimated at just over $160 billion, in-

cluding $132 billion from federal taxpayers

67

and much of this cost could have been

avoided if the government had had the political will to recognize its obligation to depositors

in the early 1980s, rather than viewing the situation as an industry bailout. Believing that

the marketplace would provide its own discipline, the government used rapid deregulation

and forbearance instead of taking steps to protect depositors. The government guarantee of

insured deposits nonetheless exposed U.S. taxpayers to the risk of losswhile the profits

made possible by deregulation and forbearance would accrue to the owners and managers

of the savings and loans.

The S&L crisis overlapped several regional banking crises in the 1980s and at first

was similar to the crisis involving mutual savings banks (MSBs). However, in contrast to

the FSLIC, the FDIC had both the money to close failing MSBs and the regulatory will to

put others on a tight leash, while allowing some forbearance in the form of the Net Worth

Certificate Program. To be sure, some MSBs later got into trouble with poor investments

and failed, but the cost of these failures pales in comparison with the cost of the failures in

the S&L industry, which was encouraged to grow and engage in risky activities with little

supervision. When the Bank Board realized that its strategies had failed, it attempted to cor-

rect the problem through regulation. In contrast, federal bank regulators used supervisory

tools and enforcement actions to limit growth and raise capital levels at commercial banks

and mutual savings banks. But both banks and S&Ls, and their regulators, got caught up in

boom-to-bust real estate cycles.

In the 1980s, a go-go mentality prevailed, along with the belief in many regions that

the economies in those regions were recession proof. In both the Southwest and New Eng-

land, the high-growth strategy pursued by many S&Ls increased the competition for de-

posits and therefore raised interest expense for both banks and thrifts. This situation

persisted and worsened as deeply insolvent S&Ls remained open because the FSLIC lacked

reserves. Banks also faced competitive pressures from the thrifts that aggressively entered

commercial mortgage lending markets and aggravated the risk taking already present in

commercial banking.

In response to the problems that arose in the 1980s, Congress enacted two major

pieces of legislation, both of which affected the FDIC. One was FIRREA, which abolished

An Examination of the Banking Crises of the 1980s and Early 1990s Volume I

188 History of the EightiesLessons for the Future

the FHLBB and the FSLIC and gave the FDIC initial responsibility for managing the Res-

olution Trust Corporation (RTC) and permanent responsibility for operating the new Sav-

ings Association Insurance Fund (SAIF). The other, passed in response not only to the

problems of the 1980s but also to the S&L-caused taxpayer losses and the FDICs near in-

solvency in the early 1990s, was the Federal Deposit Insurance Corporation Improvement

Act of 1991 (FDICIA), which dramatically changed the agencys operations.

Conclusion

The regulatory lessons of the S&L disaster are many. First and foremost is the need for

strong and effective supervision of insured depository institutions, particularly if they are

given new or expanded powers or are experiencing rapid growth. Second, this can be ac-

complished only if the industry does not have too much influence over its regulators and if

the regulators have the ability to hire, train, and retain qualified staff. In this regard, the

bank regulatory agencies need to remain politically independent. Third, the regulators need

adequate financial resources. Although the Federal Home Loan Bank System was too close

to the industry it regulated during the early years of the crisis and its policies greatly con-

tributed to the problem, the Bank Board had been given far too few resources to supervise

effectively an industry that was allowed vast new powers. Fourth, the S&L crisis highlights

the importance of promptly closing insolvent, insured financial institutions in order to min-

imize potential losses to the deposit insurance fund and to ensure a more efficient financial

marketplace. Finally, resolution of failing financial institutions requires that the deposit in-

surance fund be strongly capitalized with real reserves, not just federal guarantees.