WISCONSIN STANDARDS FOR

Personal Financial Literacy

Wisconsin Department of Public Instruction

WISCONSIN STANDARDS FOR

Personal Financial Literacy

Wisconsin Department of Public Instruction

Carolyn Stanford Taylor, State Superintendent

Madison, Wisconsin

Wisconsin Standards for Personal Financial Literacy ii

This publication is available from:

Wisconsin Department of Public Instruction

125 South Webster Street

Madison, WI 53703

(608) 266-8960

dpi.wi.gov/finance

May 2020 Wisconsin Department of Public Instruction

The Wisconsin Department of Public Instruction does not discriminate on the basis of sex, race, color, religion, creed, age, national origin,

ancestry, pregnancy, marital status or parental status, sexual orientation,; or ability and provides equal access to the Boy Scouts of America

and other designated youth groups.

Wisconsin Standards for Personal Financial Literacy iii

Table of Contents

Foreword ................................................................................................................................................................................................................................... iv

Acknowledgements ........................................................................................................................................................................................................... v

Section I: Wisconsin’s Approach to Academic Standards ........................................................................................................................... 1

Purpose of the Document ...................................................................................................................................................................... 2

What Are Academic Standards? .......................................................................................................................................................... 3

Relating the Academic Standards to All Students ......................................................................................................................... 4

Ensuring a Process for Student Success ........................................................................................................................................... 5

Section II: Wisconsin Standards for Personal Financial Literacy ............................................................................................................... 7

What is Personal Financial Literacy Education? ............................................................................................................................ 8

Wisconsin’s Approach to Standards in Personal Financial Literacy Education .................................................................. 9

Standards Structure ................................................................................................................................................................................ 10

Personal Financial Literacy Strands .................................................................................................................................................. 12

Wisconsin Standards for Personal Financial Literacy At-a-Glance ........................................................................................ 14

Standards, Learning Priorities, and Indicators ............................................................................................................................... 15

Definitions .................................................................................................................................................................................................. 16

Section III: Standards .................................................................................................................................................................................................... 17

Financial Mindset (FM) ........................................................................................................................................................................... 18

Education and Employment (EE) ........................................................................................................................................................ 24

Money Management (MM) ................................................................................................................................................................... 26

Saving and Investing (SI) ........................................................................................................................................................................ 29

Credit and Debt (CD) .............................................................................................................................................................................. 34

Risk Management and Insurance (RMI) ............................................................................................................................................ 38

Wisconsin Standards for Personal Financial Literacy iv

Foreword

On May 27, 2020, I formally adopted the Wisconsin Standards for Personal Financial Literacy. This revised set of

academic standards provides a foundational framework identifying what students should know, evaluate, and

communicate about money information and financial services. Topics include how students can select and

respond to life events and their effects on personal finances.

The Wisconsin Standards for Personal Financial Literacy were written by a committee of educators, professors, and

business people from across the state who shared their expertise in financial literacy education and teaching

from kindergarten through higher education. The writing committee outlined what content, practices, and ways

of thinking are critical for students to become responsible adults who make good financial decisions. The public and the State

Superintendent’s Academic Standards Review Council provided feedback for the writing committee to consider as part of Wisconsin’s

Academic Standards review and revision process.

The 2017 Wisconsin Act 94 requires school districts to adopt academic standards for financial literacy and incorporate instruction into the

curriculum in grades kindergarten through 12.

The Wisconsin Standards for Personal Financial Literacy are divided into six strands:

● Financial Mindset

● Education and Employment

● Money Management

● Saving and Investing

● Credit and Debt

● Risk Management and Insurance

These six strands combine to support the learning of personal financial literacy as students advance to the workplace or post-secondary

educational opportunities. The personal financial literacy skills and knowledge learned in Wisconsin schools support all students in becoming

college and career ready. Wisconsin communities are made stronger through these positive results for students.

The Wisconsin Department of Public Instruction will continue to build on this work to support implementation of the standards with

resources for the field. I am excited to share these revised Wisconsin Standards for Personal Financial Literacy.

Carolyn Stanford Taylor

State Superintendent

Wisconsin Standards for Personal Financial Literacy v

Acknowledgements

The Wisconsin Department of Public Instruction (DPI) wishes to acknowledge the ongoing work, commitment, and various contributions of

individuals to revise our state’s academic standards for Personal Financial Literacy. Thank you to the State Superintendent’s Standards

Review Council for their work and guidance through the standards process. A special thanks to the Personal Financial Literacy Writing

Committee for taking on this important project that will shape the classrooms of today and tomorrow. Thanks to the many staff members

across the division and other teams at DPI who have contributed their time and talent to this project. Finally, a special thanks to Wisconsin

educators, businesspeople, parents, and citizens who provided comment and feedback to drafts of these standards.

Wisconsin Standards for Personal Financial Literacy Writing Team

Co-Chairs: Joel Chrisler, Teacher, Sauk Prairie High School

Beth Ratway, Technical Assistance Consultant, American Institutes for Research

David Mancl, Director, Office of Financial Literacy

DPI Liaisons: Kris McDaniel, Social Studies Consultant

Diane Ryberg, Family & Consumer Sciences Education Consultant

Dave Thomas, Information Technology Education Consultant

Susan Becker

Barron Area School District

Amanda Beld

School District of West

Salem

Pam Brunclik

Wisconsin Indianhead

Technical College

Dee Dee Giovingo

Lake Geneva Schools

E-Ben Grisby

Green Bay Area Public

Schools

Jennifer Guenther

Economics WI/AIM Forward

Kerri Herrild

De Pere School District

Hoss Jager

Kenosha Unified School

District

Linda Killian-Baures

Independence School

District

Sara Kreibich

Somerset School District

Patrick Kubeny

School District of

Rhinelander

Wendy Lambrecht

School District of

Greenwood

Brett Lesniak

Stevens Point Area Public

School

Brandn Lindsey

Mequon Thiensville SD

Heather Long

Clintonville Public School

Distrct

Carrie Pierschalla

Merrill Area School District

Wisconsin Standards for Personal Financial Literacy vi

Jenny Rathke

WESTconsin Credit Union

Luc Richards

Howard-Suamico School

District

Andy Riechers

Belmont Community School

District

Rocio Santa

Milwaukee Milwaukee

Public School District

Tanya Schmidt

Oshkosh School District

Blia Schwahn

Eau Claire Area School

District

Amber Seitz

Wisconsin Bankers

Association

Delaine Stendahl

Whitehall School District

Angela Strick,

D C Everest Area School

District

Susan Turgeson

UW-Stevens Point

Erich Utrie

School District of Jefferson

Department of Public Instruction, Academic Standards

• John W. Johnson, Director, Literacy and Mathematics, and Director for Academic Standards

• Meri Annin, Lead Visual Communications Designer

• David McHugh, Strategic Planning and Professional Learning Consultant

Department of Public Instruction Leaders

• Scott Jones, Chief of Staff, Office of the State Superintendent

• Sheila Briggs, Assistant State Superintendent, Division of Academic Excellence

• Tamara Mouw, Director, Teaching and Learning Team

• Sharon Wendt, Director, Career and Technical Education Team

• Sara Baird, Assistant Director, Career and Technical Education Team

Section I

Wisconsin’s Approach to Academic Standards

Wisconsin Standards for Personal Financial Literacy 2

Purpose of the Document

The purpose of this guide is to improve Personal Financial Literacy education for students and for communities. The Wisconsin Department of

Public Instruction (DPI) has developed standards to assist Wisconsin educators and stakeholders in understanding, developing and

implementing financial literacy course offerings and curriculum in school districts across Wisconsin.

This publication provides a vision for student success and follows The Guiding Principles for Teaching and Learning

(2011). In brief, the principles

are:

1. Every student has the right to learn.

2. Instruction must be rigorous and relevant.

3. Purposeful assessment drives instruction and affects learning.

4. Learning is a collaborative responsibility.

5. Students bring strengths and experiences to learning.

6. Responsive environments engage learners.

Program leaders will find the guide valuable for making decisions about:

• Program structure and integration

• Curriculum redesign

• Staffing and staff development

• Scheduling and student grouping

• Facility organization

• Learning spaces and materials development

• Resource allocation and accountability

• Collaborative work with other units of the school, district and community

Wisconsin Standards for Personal Financial Literacy 3

What Are the Academic Standards?

Wisconsin Academic Standards specify what students should know and be able to do in the classroom. They serve as goals for teaching and

learning. Setting high standards enables students, parents, educators, and citizens to know what students should have learned at a given point

in time. In Wisconsin, all state standards serve as a model. Locally elected school boards adopt academic standards in each subject area to

best serve their local communities. We must ensure that all children have equal access to high-quality education programs. Clear statements

about what students must know and be able to do are essential in making sure our schools offer opportunities to get the knowledge and skills

necessary for success beyond the classroom.

Adopting these standards is voluntary. Districts may use the academic standards as guides for developing local grade-by-grade level

curriculum. Implementing standards may require some school districts to upgrade school and district curriculums. This may result in changes

in instructional methods and materials, local assessments, and professional development opportunities for the teaching and administrative

staff.

What is the Difference between Academic Standards and Curriculum?

Standards are statements about what students should know and be able to do, what they might be asked to do to give evidence of learning,

and how well they should be expected to know or do it. Curriculum is the program devised by local school districts used to prepare students

to meet standards. It consists of activities and lessons at each grade level, instructional materials, and various instructional techniques. In

short, standards define what is to be learned at certain points in time, and from a broad perspective, what performances will be accepted as

evidence that the learning has occurred. Curriculum specifies the details of the day-to-day schooling at the local level.

Developing the Academic Standards

DPI has a transparent and comprehensive process for reviewing and revising academic standards. The process begins with a notice of intent

to review an academic area with a public comment period. The State Superintendent’s Standards Review Council examines those comments

and may recommend revision or development of standards in that academic area. The state superintendent authorizes whether or not to

pursue a revision or development process. Following this, a state writing committee is formed to work on those standards for all grade levels.

That draft is then made available for open review to get feedback from the public, key stakeholders, educators, and the Legislature with

further review by the State Superintendent’s Standards Review Council. The state superintendent then determines adoption of the

standards.

Aligning for Student Success

To build and sustain schools that support every student in achieving success, educators must work together with families, community

members, and business partners to connect the most promising practices in the most meaningful contexts. The release of the Wisconsin

Wisconsin Standards for Personal Financial Literacy 4

Standards for Financial Literacy provides a set of important academic standards for school districts to implement. This is connected to a

larger vision of every child graduating college and career ready. Academic standards work together with other critical principles and efforts

to educate every child to graduate college and career ready. Here, the vision and set of Guiding Principles form the foundation for building a

supportive process for teaching and learning rigorous and relevant content. The following sections articulate this integrated approach to

increasing student success in Wisconsin schools and communities.

Relating the Academic Standards to All Students

Grade-level standards should allow ALL students to engage, access, and be assessed in ways that fit their strengths, needs, and interests. This

applies to the achievement of students with IEPs (individualized education plans), English learners, and gifted and talented pupils,

consistent

with all other students. Academic standards serve as the foundation for individualized programming decisions for all students.

Academic standards serve as a valuable basis for establishing concrete, meaningful goals as part of each student’s developmental progress

and demonstration of proficiency. Students with IEPs must be provided specially designed instruction that meets their individual needs. It is

expected that each individual student with an IEP will require unique services and supports matched to their strengths and needs in order to

close achievement gaps in grade-level standards. Alternate standards are only available for students with the most significant cognitive

disabilities.

Gifted and talented students may achieve well beyond the academic standards and move into advanced grade levels or into advanced

coursework.

Our Vision: Every Child a Graduate, College and Career Ready

We are committed to ensuring every child graduates from high school academically prepared and socially and emotionally competent. A

successful Wisconsin student is proficient in academic content and can apply their knowledge through skills such as critical thinking,

communication, collaboration, and creativity. The successful student will also possess critical habits such as perseverance, responsibility,

adaptability, and leadership. This vision for every child as a college and career ready graduate guides our beliefs and approaches to education

in Wisconsin.

Wisconsin Standards for Personal Financial Literacy 5

Guided by Principles

All educational initiatives are guided and impacted by important and often unstated attitudes or principles for teaching and learning. The

Guiding Principles for Teaching and Learning (2011) emerge from research and provide the touchstone for practices that truly affect the vision

of Every Child a Graduate Prepared for College and Career. When made transparent, these principles inform what happens in the classroom,

direct the implementation and evaluation of programs, and most importantly, remind us of our own beliefs and expectations for students.

Ensuring a Process for Student Success

For Wisconsin schools and districts, implementing the Framework for Equitable

Multi-Level Systems of Supports (2017) means providing equitable services, practices,

and resources to every learner based upon responsiveness to effective instruction

and intervention. In this system, high-quality instruction, strategic use of data, and

collaboration interact within a continuum of supports to facilitate learner success.

Schools provide varying types of supports with differing levels of intensity to

proactively and responsibly adjust to the needs of the whole child. These include

the knowledge, skills and habits learners need for success beyond high school,

including developmental, academic, behavioral, social, and emotional skills.

Connecting to Content: Wisconsin Academic Standards

Within this vision for increased student success, rigorous, internationally

benchmarked academic standards provide the content for high-quality curriculum

and instruction and for a strategic assessment system aligned to those standards.

With the adoption of the standards, Wisconsin has the tools to design curriculum,

instruction, and assessments to maximize student learning. The standards articulate what we teach so that educators can focus on how

instruction can best meet the needs of each student. When implemented within an equitable multi-level system of support, the standards can

help to ensure that every child will graduate college and career ready.

Wisconsin Standards for Personal Financial Literacy 6

References

The Guiding Principles for Teaching and Learning. 2011. Madison, WI: Wisconsin Department of Public Instruction. Retrieved from

https://dpi.wi.gov/standards/guiding-principles

.

Framework for Equitable Multi-Level Systems of Supports. 2017. Madison, WI: Wisconsin Department of Public Instruction. Retrieved from

https://dpi.wi.gov/rti

.

Section II

Wisconsin Standards for Personal Financial Literacy

Wisconsin Standards for Personal Financial Literacy 8

What is Personal Financial Literacy Education?

Personal financial literacy education is the focus on teaching students the ability to understand, evaluate, and communicate information about money

and financial services. This learning includes the selection of appropriate financial options, the ability to plan for the future, and the capability to

respond to life events and their effect on personal finances. The Wisconsin Standards for Personal Financial Literacy (the standards) are divided into six

strands:

● Financial Mindset

● Education and Employment

● Money Management

● Saving and Investing

● Credit and Debt

● Risk Management and Insurance

Each of these six strands is an important component to the whole of financial literacy. Topics of study could include things such as: verbal vs. written

contracts, the true cost of interest, goal setting, protection from loss, insurance, spending habits, bankruptcy, sources of credit, and investment options.

Wisconsin Standards for Personal Financial Literacy 9

Wisconsin’s Approach to Standards in Personal Financial Literacy

The Wisconsin Standards for Personal Financial Literacy were written by a committee of educators, professors, and business people from across the state.

The writing committee was tasked with outlining what content, practices, and ways of thinking are critical for students to become responsible adults

who make good financial decisions.

The foundational documents and support for the writing committee include:

● Economics and Personal Finance Standards of Learning (Virginia Department of Education, 2009);

● Financial Coaching Strategies (Division of Extension – University of Wisconsin-Madison, 2017);

● Financial Literacy Standards & Framework (National Financial Educators Council, 2018);

● Hands on Banking (Wells Fargo, 1999 - 2009);

● National Standards for Financial Literacy (Council for Economic Education, 2013);

● National Standards in K-12 Personal Finance Education (JumpStart Coalition for Personal Financial Literacy, 2017);

● Social & Emotional Learning Standards (Illinois State Board of Education, 2003);

● Social and Emotional Learning Competencies (Wisconsin Department of Public Instruction, 2018);

● Strands and Standards General Financial Literacy (Utah State Board of Education-Career & Technical Education, 2015);

● Take Charge Today (The University of Arizona, 2013);

● Wisconsin’s Vision for Entrepreneurship Education (Wisconsin Department of Public Instruction, 2009);

● Wisconsin Standards for Business & Information Technology (Wisconsin Department of Public Instruction, 2013);

● Wisconsin Standards for Family & Consumer Sciences (Wisconsin Department of Public Instruction, 2013);

● Wisconsin Standards for Information Technology Literacy (Wisconsin Department of Public Instruction, 2017);

● Wisconsin’s Model Academic Standards for Personal Financial Literacy (Wisconsin Department of Public Instruction, 2006);

● Wisconsin Standards for Social Studies (Wisconsin Department of Public Instruction, 2018).

Wisconsin Standards for Personal Financial Literacy 10

Standards Structure

• Discipline: Personal Financial Literacy

• Content Area (Strand): Financial Mindset

• Standard: Broad statement that tells what students are

expected to know or be able to do

• Learning Priority: Breaks down the broad statement into

manageable learning pieces

• Performance Indicator by Grade Band: Measurable degree to

which a standard has been developed and/or met

How to read the standards codes for a performance indicator:

“Content areas” for Personal Financial Literacy in this code structure include:

● FM - Financial Mindset

● EE - Education and Employment

● MM - Money Management

● SI - Saving and Investing

● CD - Credit and Debt

● RMI - Risk Management and Insurance

Wisconsin Standards for Personal Financial Literacy 11

Grade Bands

All Wisconsin academic standards are formatted to a common template to support educators in reading and interpreting them. Most of these standards are developed

around grade bands.

Grade bands of K-2, 3-5, 6-8, and 9-12 align to typical elementary (e), intermediate (i), middle (m), and high school (h) levels. Each row of learning priorities shows a

progression of indicators across the grade bands.

Some performance indicator boxes are intentionally left blank where it is not developmentally appropriate to teach a particular personal financial literacy topic at that

grade band level.

Wisconsin Standards for Personal Financial Literacy 12

Personal Financial Literacy Strands

Financial Mindset

Financial mindset is a combination of the values, emotions, attitudes, behaviors, and external influences that lead to mental habits for thinking about and responding to

any financial circumstances; the financial mindset offers the “why,” where the other strands outline the “how.” An individual’s financial mindset is usually influenced by

previous financial experiences; however, self-awareness of influences can play a significant role in future decisions. The increasing scope of financial choices makes it

essential that students know their resources, rights, and responsibilities as consumers. This includes an understanding of the role of contextual factors in decision

making as well as the role of advertising, sales techniques, consumer laws, and consumer organizations. The ability to analyze opportunity costs, value, and benefits of

products and services is an essential skill for consumers. The reality and potential for building an intentional financial mindset includes the need for a sense of

responsibility to the broader community.

Education and Employment

Education and employment is establishing short-range and long-range financial goals as an essential part of financial literacy. This process begins while a person is in

school and continues throughout life. A clear understanding of the interconnectedness of educational attainment, career choice, entrepreneurial attitudes, and

economic conditions will help to shape goals and increase the likelihood of reaching them.

Money Management

Money management is the foundation of being financially responsible. Learning how to plan, develop, use, and maintain a personal budget is the first step in being able

to make quality financial choices and decisions. Proactive money management skills, setting financial goals, and understanding effective cash flow strategies are the

next steps that allow students to be responsible consumers. Financial institutions and service providers play a significant role in supporting our lifelong learning about

money management.

Saving and Investing

Saving and investing is the relationship among financial institutions, investment options, avenues for financial research, the economic history, performance of

investments, and the appropriate application of basic economic principles. Using information from these and other sources will lead to wiser financial planning

decisions for individuals and families.

Credit and Debt

Credit and debt is the role and responsibility regarding how people incur debt and seek credit for major purchases such as a home, car, education, and business. The

ability to choose the most advantageous sources and forms for financing has long-term benefits. It is essential to make informed decisions when incurring debt,

understand the true costs of credit, and develop skills for managing existing debt.

Risk Management and Insurance

Risk management and insurance is how people address unexpected financial losses or needs, which can affect the financial status of an individual or family for years. In

addition to avoiding unreasonable risks in saving and investing, contemporary economics also requires that insurance, including life, property, health, liability, and

disability be part of financial planning for individuals and families.

Wisconsin Standards for Personal Financial Literacy 13

Wisconsin Standards for Personal Financial Literacy At-a-Glance

Students will...

Financial Mindset

1. Develop strategies to make intentional financial decisions throughout their lifespan.

2. Analyze how financial psychology impacts financial well-being.

3. Establish digital awareness to enhance their financial mindset.

Education and Employment

1. Compare the effect of personal income on their goals.

2. Evaluate the impact of lifelong learning on one’s ability to function effectively in a diverse and changing economy.

Money Management

1. Demonstrate their ability to use money management skills and strategies.

2. Utilize financial institutions and service providers to support money management.

Saving and Investing

1. Explore savings concepts and apply this knowledge to attain financial security.

2. Explore investing concepts and apply this knowledge to attain financial security.

Credit and Debt

1. Examine the benefits and costs of using credit.

2. Interpret lending options and consumer rights and responsibilities.

Risk Management and Insurance

1. Contrast different types of risk and how it could affect financial decisions.

2. Assess possible choices to protect against financial risk.

Wisconsin Standards for Personal Financial Literacy 14

Standards, Learning Priorities, and Indicators for Wisconsin Standards for Personal Financial Literacy

The Wisconsin Standards for Personal Financial Literacy outline what students should know and be able to do upon graduation from a Wisconsin public high school to

prepare for future studies, career, and community life. The standards are divided into six strands: Financial Mindset; Education and Employment; Money Management;

Saving and Investing; Credit and Debt; and Risk Management and Insurance. Each strand has two or three standards that are divided into learning priorities and

performance indicators across four grade bands.

The knowledge and skills set forth in the Wisconsin personal financial literacy strands and standards cross all grade levels and disciplines. A comprehensive,

developmentally appropriate pre-kindergarten through grade 12 program can promote personal financial literacy throughout numerous curricular areas, including

Business and Information Technology, Family and Consumer Sciences, Mathematics, and Social Studies. Educators from all grade levels can use the financial literacy

standards to align instruction and create grade-specific curricula and activities designed to instill within students a desire to be financially literate. The standards are

intended to help schools develop a comprehensive K-12 program that provides the knowledge and skills to establish sound financial habits.

The strands in personal financial literacy are meant to be used together; the strands were purposely condensed to avoid duplication. It will be helpful to educators and

district leaders conducting a curriculum review to unpack the standards in every strand to see where they are best met in the local district. Research studies have

shown that students recall and understand themes and topics better when strands are integrated and not taught in isolation.

Wisconsin Standards for Personal Financial Literacy 15

Definitions

The use of “i.e.” and “e.g.” in the indicators is in the manner of the original Latin. The abbreviation “i.e.”, from the Latin id est, means “that is”, and is used as a definition

(required information). The abbreviation “e.g.” is from the Latin exempli gratia, and means “for example” (suggested information). Definitions marked with “*” are taken

from Wisconsin’s Model Academic Standards for Personal Financial Literacy (2006).

*Capital: One of three credit scoring factors representing the value of owned personal items including savings, investments, and property.

*Cost-benefit analysis, risk-reward relationship: Tool used to choose among alternatives that involves weighing the cost of a product or service against the benefit it

will provide.

*Diversification: Distributing funds among different types of investments to minimize overall risk.

Entrepreneurship: Creating something new or developing ideas or projects; not following prescribed paths and thinking outside the box. Visit Wisconsin’s Vision for

Entrepreneurship Education for additional information.

Fiduciary: A person (or a business like a bank or stock brokerage) who has the power and obligation to act for another (often called the beneficiary) under

circumstances which require total trust, good faith and honesty. (Legal Dictionary, dictionary.law.com, accessed 01/09/2020)

Investment vehicle: A product used by investors in an attempt to gain positive returns. Investment vehicles have a range of regulation, jurisdiction, and risk that may

influence the likelihood of being included in an investment portfolio due to investor’s knowledge, skills, tolerance, goals, and financial capability. (Investopedia,

investopedia.com, accessed 01/09/2020)

Investment strategy: Guides an investor's decisions based on goals, risk tolerance, and future needs for capital. Some investment strategies seek rapid growth where

an investor focuses on capital appreciation, or they can follow a low-risk strategy where the focus is on wealth protection. (Investopedia, investopedia.com, accessed

01/09/2020)

*Net worth: The difference between a person’s assets and liabilities.

*Opportunity cost: Whenever choices are made, the cost of something expressed in terms of what had to be given up to obtain it. The resources used to satisfy one

goal that cannot be used for another (i.e., weighing of one alternative against another rather than merely considering the cash price or value of a specific good or

service).

*Pay yourself first: Disciplined saving or setting aside money as a regular part of the budget for later spending or investing.

*Philanthropy: A personal foundation, or corporate interest in helping others, especially through gifts to charities or endowments to institutions.

Wisconsin Standards for Personal Financial Literacy 16

*Social Security: The federal government’s basic program for providing income when earnings are reduced or stopped because of retirement or disability. Income is

also provided to families when the working parent(s) dies and underage children are a part of the family.

Section III

Discipline: Personal Financial Literacy (PFL) Standards

Wisconsin Standards for Personal Financial Literacy 18

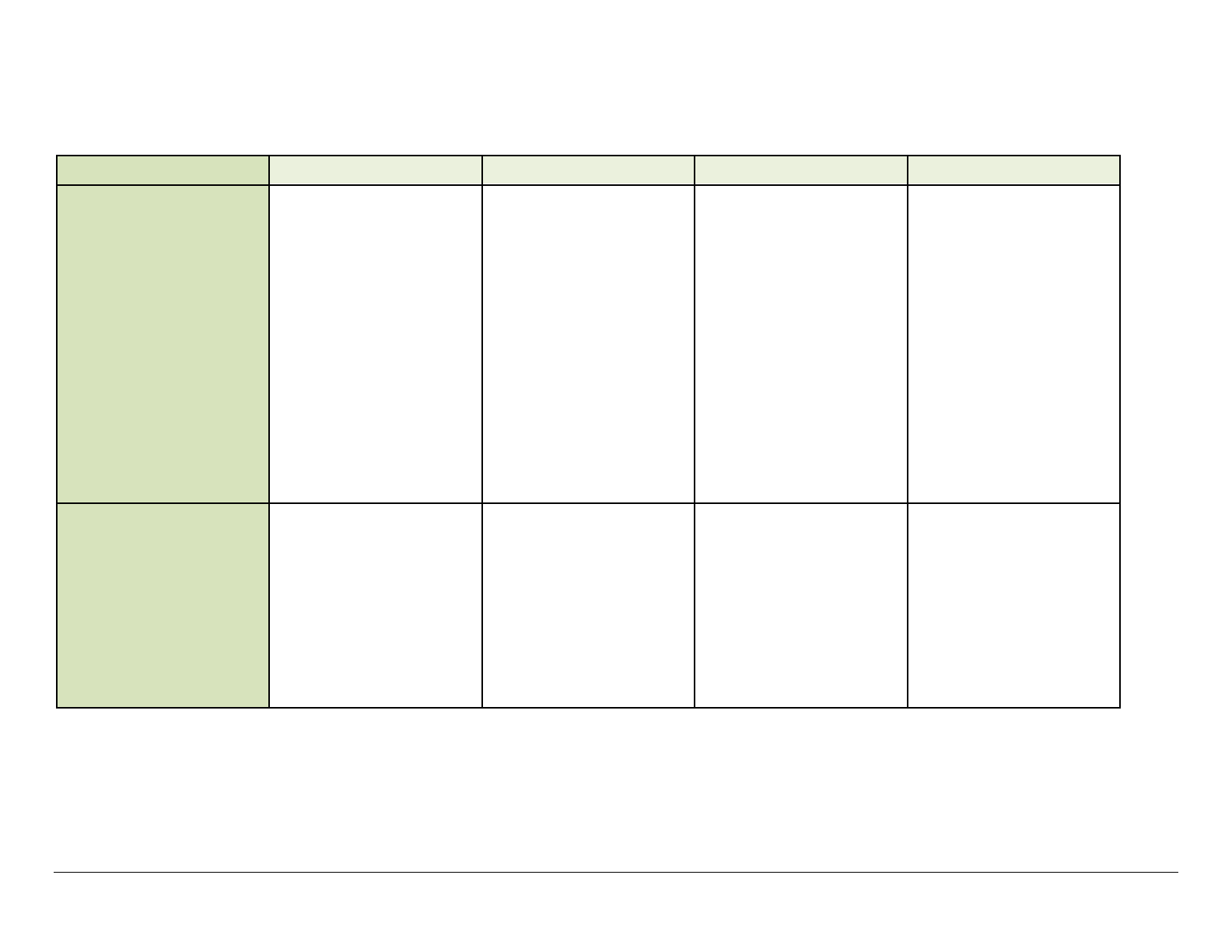

Content Area: Financial Mindset (FM)

Standard PFL.FM1: Students will develop strategies to make intentional financial decisions throughout their lifespan.

Performance Indicators (by Grade Band)

Learning Priority K-2 (e) 3-5 (i) 6-8 (m) 9-12 (h)

FM1.a: Critical Consumer

FM1.a.e

Differentiate between buyers

(consumers) and sellers

(producers).

List traits of being a

responsible consumer (e.g.,

look at the price or compare

the value of items).

Define advertising and list

places advertisements can be

found.

FM1.a.i

Describe the steps in making

a purchase (i.e., consumer

buying process).

Identify items that can be

used in making consumer

decisions (e.g., comparison

shopping skills regarding

price or substitutes).

Predict the motives of a sales

claim and explain how

consumers would verify

information delivered

through a range of

advertisements (e.g., digital,

print, audio, or

product/service reviews).

FM1.a.m

Analyze the roles of

consumers and producers in

financial markets.

Distinguish between the

rights and responsibilities of

buyers and sellers under

consumer protection laws.

Evaluate the influence on

demographic groups of

advertising and the media on

decision making and

spending.

FM1.a.h

Summarize consumer rights,

responsibilities, protections

and consumer vigilance (e.g.,

contesting incorrect billing or

registering a consumer

complaint).

Analyze and apply multiple

sources of information when

making consumer decisions

(e.g., advertisements,

reviews, interest rates,

applicable fees, consumer

movements, or choice).

Analyze the financial impact

of advertising including

techniques, potential for

deception along with the

influence of promotions,

packaging, and placement.

Wisconsin Standards for Personal Financial Literacy 19

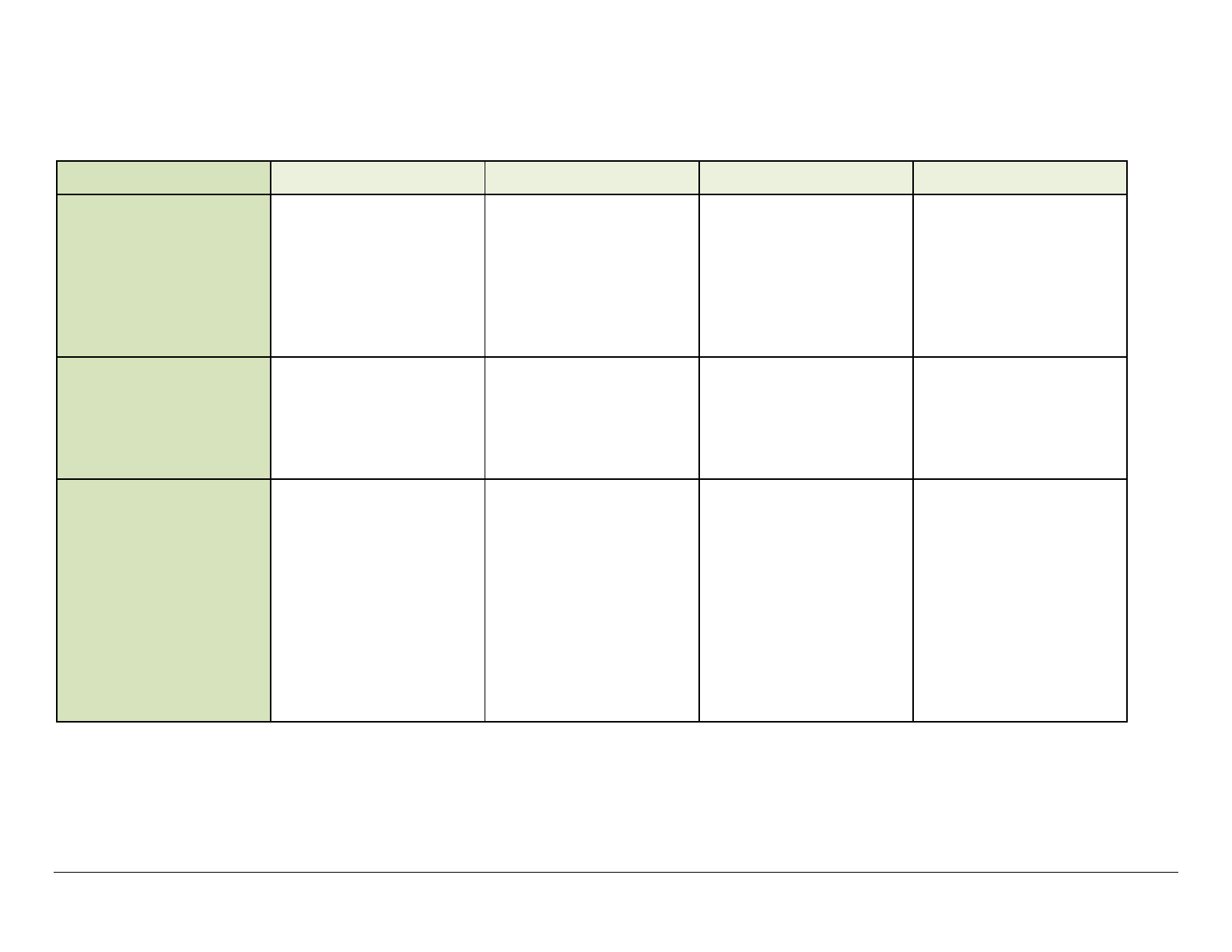

Content Area: Financial Mindset (FM)

Standard PFL.FM1: Students will develop strategies to make intentional financial decisions throughout their lifespan. (cont’d)

Performance Indicators (by Grade Band)

Learning Priority K-2 (e) 3-5 (i) 6-8 (m) 9-12 (h)

FM1.b: Functions and

Structure of Money

FM1.b.e

Categorize types of money

(e.g., coins or bills), and

explain why money is used.

FM1.b.i

Describe the role of money in

everyday life.

FM1.b.m

Differentiate between the

functions of money as a

medium of exchange (e.g.,

money accepted in exchange

for goods or services), store

of value (e.g., retention of

money’s value for future

exchanges), and a unit of

account (e.g., stated unit of

measurement to simplify

transactional exchanges in

contrast to bartering).

FM1.b.h

Evaluate the functions and

value of money in the United

States (e.g., how the value is

based upon the strength and

credit of the

government/issuing body).

Identify the function of the

foreign exchange market to

establish a relative value of

different currencies and the

process that changes in

currency values may have on

purchasing power in

relationship to the cost of

goods and services in a global

marketplace.

FM1.c: Opportunity Costs

FM1.c.e

Differentiate between a want

and a need.

FM1.c.i

Compare and contrast the

costs and benefits of a

decision.

Explain that choices may

have long-term unintended

consequences.

FM1.c.m

Predict the opportunity costs

of various decisions.

Explain why the opportunity

cost might differ from person

to person or in different

situations (e.g., auto or

housing).

Contrast cost-benefit and

opportunity cost.

FM1.c.h

Perform a cost-benefit

analysis on a real-world

situation.

Wisconsin Standards for Personal Financial Literacy 20

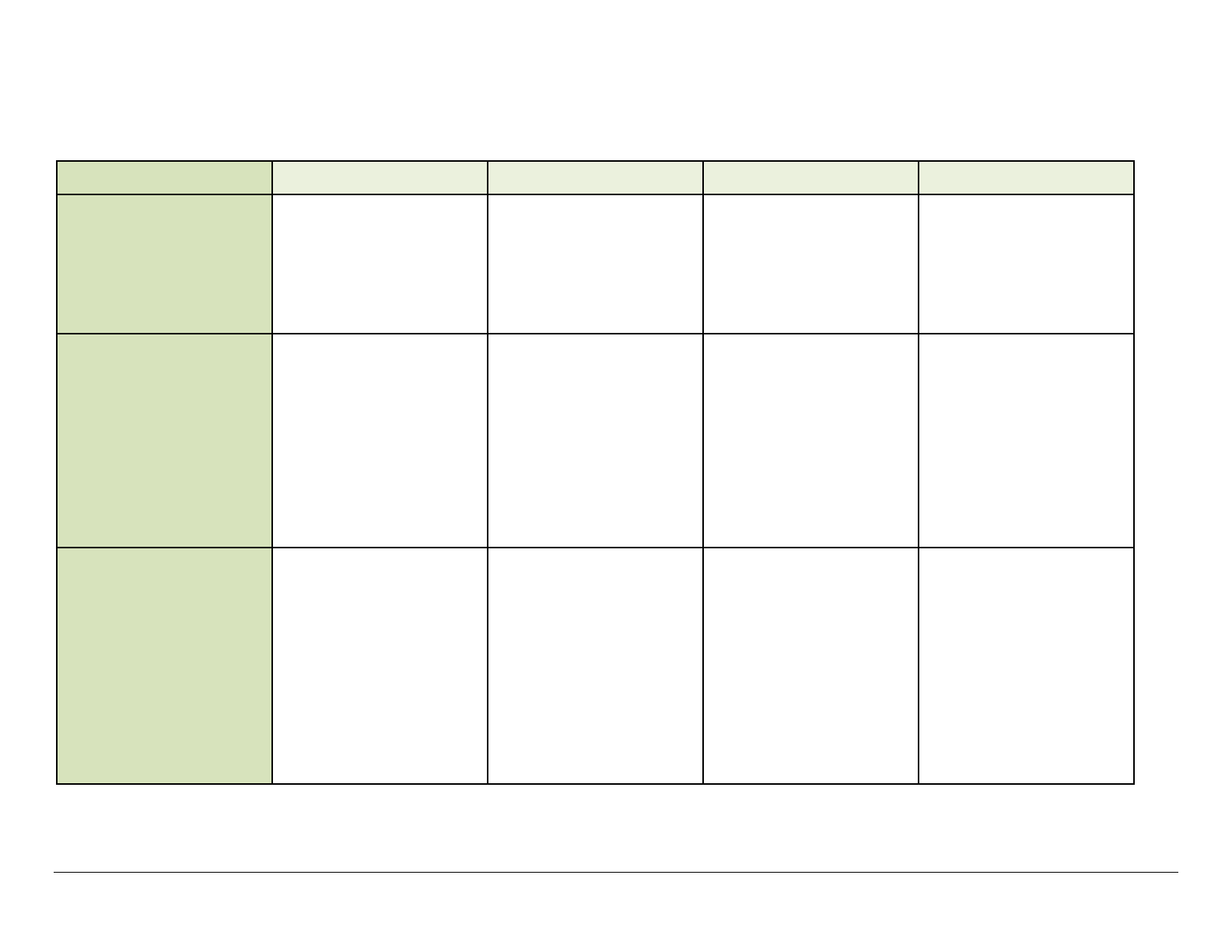

Content Area: Financial Mindset (FM)

Standard PFL.FM2: Students will analyze how aspects of financial psychology impact financial well-being.

Performance Indicators (by Grade Band)

NOTE: This standard continued on next page.

Learning Priority K-2 (e) 3-5 (i) 6-8 (m) 9-12 (h)

FM2.a: Values and

Behavior

FM2.a.e

Identify why people decide to

earn, save, spend, or give

money.

FM2.a.i

Examine different cultural

perspectives and behaviors

regarding financial values and

goals across communities.

FM2.a.m

Analyze different cultural

perspectives and behaviors

regarding financial values and

goals across communities.

FM2.a.h

Assess the impact of

individual values and

behaviors on financial

decisions and goals.

FM2.b: Emotional

Influences

FM2.b.e

Identify how emotions may

be the same or different from

other people.

FM2.b.i

Describe how emotions

impact financial decisions.

FM2.b.m

Describe financial situations

that trigger various emotions.

Summarize how emotions

may interfere with the

achievement of financial

goals.

FM2.b.h

Evaluate strategies

individuals use to manage

emotions impacting financial

decisions.

FM2.c: External Influences

FM2.c.e

Identify external influences

(e.g., peers, family, or

community) that may affect

what someone wants.

FM2.c.i

Explain ways financial

decisions are influenced by

external factors.

FM2.c.m

Differentiate how positive

and negative external

influences (e.g., peers or

marketing) impact financial

decisions in a society with

frictionless transactions (e.g.,

pre-stored payment

information, no signature

required, or biometrics).

FM2.c.h

Critique a financial plan and

identify areas that may have

been influenced by external

sources.

FM2.d: Financial Goals

FM2.d.e

Identify the importance of a

financial goal (e.g., purchasing

a bicycle or toy).

FM2.d.i

Describe elements of a goal

development strategy (e.g.,

SMART - specific,

measurable, attainable,

relevant, and time-bound).

FM2.d.m

Analyze long-term and short-

term financial goals utilizing

elements of goal

development strategies.

FM2.d.h

Distinguish how an

investment plan that

incorporates a goal

development strategy

reflects various life factors

(e.g., age, personal values,

income, liabilities, assets,

goals, family size, risk

tolerance, or net worth).

Wisconsin Standards for Personal Financial Literacy 21

Content Area: Financial Mindset (FM)

Standard PFL.FM2: Students will analyze how aspects of financial psychology impact financial well-being. (cont’d)

Performance Indicators (by Grade Band)

Learning Priority

K-2 (e)

3-5 (i)

6-8 (m)

9-12 (h)

FM2.e: Civic Engagement

and Philanthropy (e.g.,

giving back, volunteering,

donation, or charity)

FM2.e.e

Recognize ways to give back

(e.g., donating to a charity or

volunteering) in our

classroom, school,

community, state, tribal

nation, country, and in the

world.

FM2.e.i

Describe the benefits of

charitable giving,

volunteerism, and charities in

our classroom, school,

community, state, tribal

nation, country, and in the

world.

FM2.e.m

Research individuals or

organizations that give back

and describe their impact on

the local, state, tribal nation,

country, or world.

FM2.e.h

Describe how to incorporate

philanthropic opportunities

into personal financial goals.

Wisconsin Standards for Personal Financial Literacy 22

Content Area: Financial Mindset (FM)

Standard PFL.FM3: Students will establish digital awareness to enhance their financial mindset.

Performance Indicators (by Grade Band)

Learning Priority K-2 (e) 3-5 (i) 6-8 (m) 9-12 (h)

FM3.a: Online and Account

Security

FM3.a.e

Explain the importance of an

online password, and identify

reasons to use a password.

FM3.a.i

Compare and contrast strong

and weak online passwords,

and identify criteria for a

strong password.

Identify information that we

protect with a password.

Identify what personally

identifiable information (PII)

is private and should not be

shared with others (digitally).

FM3.a.m

Evaluate alternatives to

account passwords (e.g., facial

or fingerprint recognition, or

sign-in through social media

accounts).

Explore methods of managing

and protecting passwords for

multiple accounts.

Identify possible motives

behind data breaches.

Describe ways to determine if

a person’s identity has been

compromised.

FM3.a.h

Choose an effective means to

manage and protect

passwords for multiple online

accounts.

Develop strategies to guard

against and respond to

malicious threats including

viruses, phishing, and identity

theft, and recognize the

importance of security

protocols.

Research ways online

transactions, online banking,

email scams, and

telemarketing calls can make

a person vulnerable to

identity theft.

FM3.b: Digital Footprint

FM3.b.e

Define sources of digital

information and storage (e.g.,

Internet, World Wide Web,

and personal devices).

FM3.b.i

Describe ways a person

leaves a financial digital

footprint.

Explore under supervision

information a person can

obtain online about other

individuals.

FM3.b.m

Compare and contrast active

and passive financial digital

footprints.

Illustrate how a financial

digital footprint can be used

by others.

FM3.b.h

Assess actions and data as

beneficial or detrimental to a

financial digital footprint.

Strategize ways to optimize a

financial digital footprint.

NOTE: This standard continued on next page.

Wisconsin Standards for Personal Financial Literacy 23

Content Area: Financial Mindset (FM)

Standard PFL.FM3: Students will establish digital awareness to enhance their financial mindset. (cont’d)

Performance Indicators (by Grade Band)

Learning Priority

K-2 (e)

3-5 (i)

6-8 (m)

9-12 (h)

FM3.c: Digital Resources

FM3.c.e

List websites or mobile apps

and identify what types of

information people access

online.

FM3.c.i

Determine criteria to identify

safe websites and apps.

FM3.c.m

Explain restrictions on why

websites and mobile apps

may be legally restricted

based upon age (e.g., Family

Educational Rights and

Privacy Act).

Evaluate how financial

applications are utilized to

support financial transactions

(e.g., access financial

information, direct deposit,

bill pay, transfers, or

balancing a checking account).

FM3.c.h

Appraise a user agreement

for common financial

websites and applications.

Evaluate benefits and costs of

exclusively online banking.

Wisconsin Standards for Personal Financial Literacy 24

Content Area: Education and Employment (EE)

Standard: PFL.EE1: Students will compare the effect of personal income on their goals.

Performance Indicators (by Grade Band)

Learning Priority K-2 (e) 3-5 (i) 6-8 (m) 9-12 (h)

EE1.a: Career

Development

EE1.a.e

Explain behaviors and

decisions that reflect

interests, likes, and dislikes.

Describe why people work

and how aspects of the work

environment affect their life.

EE1.a.i

Build an ongoing awareness

of personal abilities, skills,

interests, and motivation, and

determine how these fit with

a chosen career pathway.

Compare and contrast

occupations relative to

personal interests, aptitudes,

and potential earnings (i.e.,

military service,

apprenticeship, skilled trades,

and professional

occupations).

EE1.a.m

Assess personal strengths

(e.g., skills, knowledge, and

experience), aptitudes, and

passions related to potential

future careers.

Create a plan to reach future

career goals taking into

account personal interests,

aptitudes, and potential

earnings.

EE1.a.h

Prioritize potential

occupations based upon the

results of a career assessment

or interest inventory.

Create a career development

plan relative to personal

interests, aptitudes, and

potential earnings.

Explain how career

development goals fit with

personal skills and attributes,

current activities, and

postsecondary plan.

EE1.a: Deductions and

Taxes

EE1.a.e

Summarize goods and

services that the government

provides (e.g., roads, schools,

or police).

EE1.a.i

List reasons a government

taxes people.

EE1.a.m

Identify payroll taxes that are

deducted from a paycheck.

EE1.a.h

Evaluate a paycheck and how

payroll taxes along with other

deductions (e.g., insurance,

retirement account, or

flexible spending account for

parking, childcare, and health)

decrease net income.

Analyze the impact of tax

liability on income including

potential deductions and

credits that will impact state

and federal income tax.

Evaluate types of taxes (e.g.,

progressive or regressive)

and earned benefits with

eligibility criteria (e.g., Social

Security, Medicare, or

Medicaid).

Understand and follow the

requirements of filing income

taxes.

EE1.b: Types of

Compensation

EE1.b.e

Identify ways people earn

money.

EE1.b.i

Describe the ways people are

compensated.

Identify reasons people earn

different amounts of money.

EE1.b.m

Evaluate specific examples of

intrinsic and extrinsic

rewards for a specific career

(e.g., salary, flexibility, family

time, or goodwill).

Compare and contrast

employment choices based on

intrinsic and extrinsic factors

(e.g., salary, flexibility, family

time, or goodwill).

EE1.b.h

Assess ways workers are

compensated in different

industries and sectors (i.e.,

fringe benefits, wages,

pension plan, hourly or

salaried).

Wisconsin Standards for Personal Financial Literacy 25

Content Area: Education and Employment (EE)

Standard: PFL.EE2: Students will evaluate the impact of lifelong learning on one’s ability to function effectively in a diverse and changing

economy.

Performance Indicators (by Grade Band)

Learning Priority K-2 (e) 3-5 (i) 6-8 (m) 9-12 (h)

EE2.a: Post-Secondary

Education, Skills, and

Training

EE2.a.e

Identify skills needed for

different types of jobs.

Discover the different skills

associated with various job or

career fields (e.g., what skills

are needed to be a plumber,

teacher, dentist, firefighter or

store manager).

EE2.a.i

Assess different types of jobs,

based on the skills associated

with each job.

Interpret career information.

EE2.a.m

Compare the benefits and

costs of a variety of post-

secondary education and

training options.

Assess data on the lifetime

earnings of workers with

different levels of education

or training.

Explain cost and benefit

factors such as earning

potential, the total cost of

education or training, and

career opportunities within a

chosen career pathway.

EE2.a.h

Assess how people’s

willingness and ability to plan

for the future affects their

decision to increase their

education or job training in a

dynamic and changing labor

market.

Compare the employment

rates of workers with

different skills.

Evaluate the return on

investment of the

preparation requirements for

different career pathways.

EE2.b: Emerging

Employment and

Education Trends

EE2.b.e

Categorize jobs as high

demand or low demand.

Describe how specific jobs or

career fields have changed

over time.

EE2.b.i

Explain how economic, social,

and technological changes

can impact employment

trends and markets.

Contrast jobs versus careers.

EE2.b.m

Assess and interpret

resources that can be used to

evaluate emerging

employment trends and

markets (e.g., U.S. Bureau of

Labor Statistics, state

agencies, or job search

engines).

EE2.b.h

Research and identify a job or

field that may be high

demand in the future based

on emerging technologies.

Assess employment trends

and how those will impact

future career paths.

Wisconsin Standards for Personal Financial Literacy 26

Content Area: Money Management (MM)

Standard PFL.MM1: Students will demonstrate their ability to use money management skills and strategies.

Performance Indicators (by Grade Band)

Learning Priority K-2 (e) 3-5 (i) 6-8 (m) 9-12 (h)

MM1.a: Budgeting

MM1.a.e

Explain the importance of a

budget.

MM1.a.i

Provide examples of

household expenses and

sources of income.

MM1.a.m

Construct a basic budget,

including allocating spending

and savings that spans for a

week or a month.

MM1.a.h

Prepare a budget or spending

plan that depicts varying

sources of income, a planned

saving strategy, taxes, and

other sources of fixed and

variable spending.

MM1.b: Financial

Management

MM1.b.e

Identify that there are three

ways you can use money -

save, spend, and give.

MM1.b.i

Identify age-appropriate ways

to save, spend, and give

money.

Identify the personal

information necessary to

establish a financial account

(e.g., personal details, contact

information, and social

security number).

MM1.b.m

Plan for ways to save, spend,

and give money.

Compare responsible saving,

spending, and charitable

habits.

Identify various organizations

or places that provide

financial resource support to

individuals or families.

Classify the personal

eligibility criteria to establish

a financial account (e.g., age,

residency, or amount of

deposit).

MM1.b.h

Compare and contrast

different sources of active and

passive income, savings, and

investment vehicles.

Develop and critique short-

term and long-term personal

financial plans.

Evaluate circumstances when

an individual may want to

grant representation or

consult for financial advice

with a financial advisor,

attorney, tax advisor, or

financial planner.

Summarize factors to

consider when seeking

financial advice and services.

NOTE: This standard continued on next page.

Wisconsin Standards for Personal Financial Literacy 27

Content Area: Money Management (MM)

Standard PFL.MM2: Students will utilize financial institutions and service providers to support money management. (cont’d)

Performance Indicators (by Grade Band)

Learning Priority K-2 (e) 3-5 (i) 6-8 (m) 9-12 (h)

MM2.a: Financial

Institutions and Service

Providers

MM2.a.e

Identify financial institutions

within the community.

MM2.a.i

Identify the services and

resources that financial

institutions provide

consumers.

MM2.a.m

Describe and evaluate the

benefits and risks of basic

financial institution services.

MM2.a.h

Compare financial

institutions and service

providers (e.g., banks, credit

unions, investment and

brokerage firms, mortgage

brokers, payday lenders,

online financial institutions,

or loan agencies).

Analyze the reasons for

regulation and the roles of

financial regulators [e.g.,

Federal Deposit Insurance

Corporation (FDIC), National

Credit Union Administration

(NCUA), Consumer Finance

Protection Bureau (CFPB),

Federal Reserve, Office of the

Comptroller of the Currency

(OCC), or Wisconsin

Department of Financial

Institutions (WDFI),

Wisconsin Office of the

Commissioner of Insurance

(WOCI), Wisconsin

Department of Agriculture,

Trade, and Consumer

Protection (WDATCP)].

NOTE: This standard continued on next page.

Wisconsin Standards for Personal Financial Literacy 28

Content Area: Money Management (MM)

Standard PFL.MM2: Students will utilize financial institutions and service providers to support money management. (cont’d)

Performance Indicators (by Grade Band)

MM2.b: Payment Types

MM2.b.e

Recognize that items of value,

including money, can be

earned and exchanged for

goods and services.

MM2.b.i

Investigate multiple ways to

pay for goods and services.

Compare digital banking

methods and cash payments

for purchasing goods and

services.

Identify methods to prove

income has been received and

payment has been made.

MM2.b.m

Compare features of digital

banking in online banking, bill

pay, transfers, and checking

account transactions.

Compare the use of cash,

debit cards, credit cards,

checks, and other modern

forms of payment.

Determine how pre-

authorized payments impact

account balances.

Recognize the importance of

retaining records of financial

transactions.

MM2.b.h

Assess the advantages and

disadvantages of digital

banking (e.g., online banking,

bill pay, transfers, or checking

account transactions).

Summarize the tax and legal

implications that require you

to maintain personal records

of significant financial

transactions.

MM2.c: Alternative

Financial Currency

MM2.c.e

Describe how paying for

goods and services online is

still using real money.

MM2.c.i

Differentiate between debit-

and credit-types of financial

currency.

MM2.c.m

Analyze online and mobile

systems or applications that

permit consumers to acquire

items or transfer money.

MM2.c.h

Compare online and mobile

systems or applications used

as a means of alternative

currency.

Wisconsin Standards for Personal Financial Literacy 29

Content Area: Saving and Investing (SI)

Standard PFL.SI1: Students will explore savings concepts and apply this knowledge to attain financial security.

Performance Indicators (by Grade Band)

Learning Priority K-2 (e) 3-5 (i) 6-8 (m) 9-12 (h)

SI1.a: Saving Principles

SI1.a.e

Identify an experience of

waiting to have enough

money to buy something.

SI1.a.i

Describe reasons why people

save money.

Explain the phrase pay

yourself first.

SI1.a.m

Compare and contrast places

that can be used to save

money.

Describe ways to decrease

expenses in order to increase

savings.

Compare pay yourself first to

living paycheck to paycheck.

Explain why saving is a

prerequisite to investing.

SI1.a.h

Demonstrate how to manage

savings accounts- both

manually and electronically,

including reconciliation.

Determine the opportunity

cost in relation to a saving

plan (e.g., inflation or taxes).

Compare and contrast the

benefits of pay yourself first

and living paycheck to

paycheck strategies on

financial outcomes.

SI1.b: Savings Types and

Features

SI1.b.e

Identify places where

something valuable would be

secure.

SI1.b.i

Describe why a person

deposits money into a

financial institution.

Describe characteristics of a

secure savings account.

SI1.b.m

Analyze the benefits of

depositing money into a

financial institution.

Compare and contrast

savings versus checking and

debit accounts.

SI1.b.h

Compare and contrast

characteristics of basic

savings options (e.g., savings

accounts, money market

accounts, or certificates of

deposit).

Explain the impact of

electronic funds transfer

(EFT) services on savings

accounts.

NOTE: This standard continued on next page.

Wisconsin Standards for Personal Financial Literacy 30

Content Area: Saving and Investing (SI)

Standard PFL.SI1: Students will explore savings concepts and apply this knowledge to attain financial security. (cont’d)

Performance Indicators (by Grade Band)

SI1.c: Saving Goal Planning

SI1.c.e

Describe strategies to save

money.

SI1.c.i

Identify steps to reach a

savings goal.

Explain how people make

spending and saving choices

to meet personal savings

goals.

SI1.c.m

Create a savings plan to

reach short- and long-term

personal saving goals.

Analyze how life changes or

changes in circumstances can

affect a personal savings goal.

SI1.c.h

Determine the best options

to achieve specific short- and

long-term personal saving

goals.

Compare and contrast

financial services and

products to achieve personal

saving goals.

SI1.d: Saving Risk and

Reward

SI1.d.e

Explain how choices we make

now affect what we get in the

future.

Explain how financial

institutions help people make

choices about how to save

money.

SI1.d.i

Compare types of risks and

rewards when saving (e.g., no

loss of principal, interest-

bearing).

SI1.d.m

Define simple and compound

interest.

Analyze the relationship

between opportunity cost

and reward.

SI1.d.h

Compare and contrast the

opportunity cost and reward

of basic saving options (e.g.,

savings accounts, money

market accounts, or

certificates of deposit).

Evaluate the effect of

compound interest on

savings options.

SI1.e: Role of Government

in Saving

SI1.e.i

Identify the role that law

enforcement has to protect

personal financial assets.

SI1.e.m

Recognize the limit of the

Federal Deposit Insurance

Corporation (FDIC) and

National Credit Union

Administration (NCUA)

coverage of financial

accounts.

SI1.e.h

Explain the role that

government agencies play in

protecting deposits (e.g.,

Federal Deposit Insurance

Corporation (FDIC), National

Credit Union Administration

(NCUA)).

Wisconsin Standards for Personal Financial Literacy 31

Content Area: Saving and Investing (SI)

Standard PFL.SI2: Students will explore investing concepts and apply this knowledge to attain financial security.

Performance Indicators (by Grade Band)

Learning Priority K-2 (e) 3-5 (i) 6-8 (m) 9-12 (h)

SI2.a: Investing Principles

SI2.a.e

Explain how gathering items

of value may build net worth.

SI2.a.i

Describe the difference

between saving and

investing.

Describe reasons why people

invest their money.

SI2.a.m

Explain the difference

between income and net

worth.

Compare and contrast

methods to increase net

worth.

Examine the time value of

money (TVM) and the

variables that affect time

value of money.

SI2.a.h

Explain the role of revenue

generating assets in building

net worth (e.g., real estate or

entrepreneurship).

Evaluate the effect of

compounding earned interest

on investments.

Compute time value of

money (TVM) principles (e.g.,

compound interest or Rule of

72).

Evaluate the reliability and

trustworthiness of digital

investment banking.

SI2.b: Investing Types and

Features

SI2.b.e

Differentiate between

owning something of value,

keeping money in a financial

institution, or giving money

to someone else in return for

future value.

SI2.b.i

Identify different investing

choices (e.g., collectibles,

stocks, bonds, or mutual

funds).

Predict financial outcomes

based on investing choices.

SI2.b.m

Explore investing choices

(e.g., collectibles, stocks,

bonds, or mutual funds)

which can produce income or

growth.

Identify the differences

between banks, credit unions,

and investment firms.

SI2.b.h

Describe a range of

investment vehicles (short-

term and long-term) for

buying and selling

investments.

Explain the concept of asset

allocation, associated fees,

and their effect on the rate of

return.

Differentiate between

different types of long-term

retirement investments [e.g.,

IRA, Roth IRA, 401(k), or

403(b)].

NOTE: This standard continued on next page.

Wisconsin Standards for Personal Financial Literacy 32

Content Area: Saving and Investing (SI)

Standard PFL.SI2: Students will explore investing concepts and apply this knowledge to attain financial security. (cont’d)

Performance Indicators (by Grade Band)

SI2.c: Investing Goal

Planning

SI2.c.e

Identify the difference

between short-term and

long-term (e.g., today versus

Saturday versus the future or

elementary versus middle

school versus high school).

SI2.c.i

Explain reasons why people

invest for future personal

financial goals.

Develop short- and long-term

personal investing goals.

Explain that people make

spending, saving, and

investing choices to meet

personal financial goals.

SI2.c.m

Create a prioritized list of

short- and long-term

personal financial investment

goals and suggest methods to

achieve those goals.

Compare games of chance

with investing methods for

financial planning.

Examine the role of investing

for retirement.

Investigate the role of a

financial planner.

Analyze the difference

between dividends and

capital gains.

Identify factors that influence

financial investment planning

(e.g., age, income, liabilities,

assets, goals, family size, or

risk tolerance).

SI2.c.h

Create personal criteria for

investment planning.

Analyze financial investment

services according to

personal criteria for

investment planning.

Assess various means of

building net worth.

Justify how paying yourself

first early and often

influences positive progress

toward long-term financial

planning goals.

Evaluate factors that

influence financial

investment planning (e.g.,

age, income, liabilities, assets,

goals, family size, or risk

tolerance).

Develop an investment plan

to meet individual short- and

long-term financial

investment goals.

NOTE: This standard continued on next page.

Wisconsin Standards for Personal Financial Literacy 33

Content Area: Saving and Investing (SI)

Standard PFL.SI2: Students will explore investing concepts and apply this knowledge to attain financial security. (cont’d)

Performance Indicators (by Grade Band)

SI2.d: Investing Risks and

Rewards

SI2.d.e

Identify how items of value

may fluctuate over time.

SI2.d.i

Give examples of investing

risks and rewards.

Explain why there are

different types of interest

(e.g., simple or compound).

Compare rewards when

investing.

SI2.d.m

Compare and contrast types

of risk for investing.

Choose personal risk

tolerance for investments.

Compare and contrast levels

of investment risk and levels

of investment rewards.

SI2.d.h

Compare the risk, return, and

liquidity of various

investment alternatives

contrasting a range of short-

term and long-term

investment strategies.

Identify financial risks,

including inflation, deflation,

and recession.

Assess the long-term

investment potential

associated with the stock

market, focusing on

fundamentals such as

diversification, risk-reward,

dollar cost averaging, and

investor behavior.

SI2.e: Role of Government

in Investing

SI2.e.i

Explain how federal and state

regulators help protect

investors.

Identify investment options

that are tax free.

SI2.e.m

Investigate reliable

government and industry

sources to locate background

information about a local

person who provides

investment advice.

Examine the tax rate on

short-term and long-term

investments.

Analyze the benefits of tax-

advantaged investments for

young people.

SI2.e.h

Determine information,

assistance, and protection that

individual investors can receive

(e.g., Securities and Exchange

Commission, Financial Industry

Regulatory Authority, Consumer

Financial Protection Bureau, or

State Securities Administrators).

Compare and contrast the

advantages of taxable, tax

deferred and tax-advantaged

investments for new savers,

including Roth IRAs and

employer-sponsored retirement

vehicles.

Assess fiduciary responsibilities

and due diligence of financial

professionals.

Wisconsin Standards for Personal Financial Literacy 34

Content Area: Credit and Debt (CD)

Standard PFL.CD1: Students will examine the benefits and costs of using credit.

Performance Indicators (by Grade Band)

Learning Priority K-2 (e) 3-5 (i) 6-8 (m) 9-12 (h)

CD1.a: Benefits of Using

Credit

CD1.a.e

Explain why something

borrowed must be returned.

CD1.a.i

Identify situations when

people might pay for certain

items in small amounts over

time.

Summarize the advantages

and disadvantages of using

credit.

CD1.a.m

Assess whether a specific

purchase justifies the use of

credit.

CD1.a.e

Analyze uses of credit that

provide financial and

personal benefits.

Predict why someone would

make a purchase using credit

instead of cash.

CD1.b: Costs of Using

Credit

CD1.b.e

Explain the difference

between buying and

borrowing.

CD1.b.i

Summarize the advantages

and disadvantages of using

credit.

CD1.b.m

Assess whether a specific

purchase justifies the use of

credit.

CD1.b.h

Assess the total cost of

incurring a loan (e.g., various

rates of interest, loan

origination fee, early payback,

or length of term).

CD1.c: Interest and Fees

CD1.c.e

Explain how people can

borrow money or an item if

they promise to return it.

CD1.c.i

Compare the differences

between income and

expenses.

Calculate cost of late fees

over a given time period.

CD1.c.m

Compare options for

payment on credit cards.

Demonstrate balance sheet

concepts (e.g., debit and

credit).

Compute the amount of

interest paid over time when

using credit.

Compare advantages and

disadvantages of various debt

payment methods.

CD1.c.h

Evaluate options for payment

on credit cards and the

consequences of each option.

Compare different debt

payment methods.

Calculate the total cost of

repaying a loan under various

rates of interest and over

different time periods.

NOTE: This standard continued on next page.

Wisconsin Standards for Personal Financial Literacy 35

Content Area: Credit and Debt (CD)

Standard PFL.CD1: Students will examine the benefits and costs of using credit. (cont’d)

Performance Indicators (by Grade Band)

Learning Priority

K-2 (e)

3-5 (i)

6-8 (m)

9-12 (h)

CD1.d: Debt Resolution

CD1.d.e

Identify actions a borrower

can take to satisfy a lender

when a borrowed item cannot

be repaid, is lost, or damaged.

Explain who can assist in

solving problems (e.g.,

parents, teachers, or

counselors).

CD1.d.i

Recognize consequences of

overspending when

borrowing, and reflect on

what may need to be

sacrificed to resolve a debt.

Recognize appropriate

people who could discuss

financial issues.

CD1.d.m

Identify indicators of

excessive debt.

Predict possible

consequences of excessive

debt or bankruptcy.

Explain credit coaching and

appropriate times to utilize it.

CD1.d.h

Examine services that

consumer credit counseling

agencies offer.

Examine how consumers

apply financial coaching to

various situations.

Investigate the purpose and

types of bankruptcy,

including its possible negative

effects on assets,

employability, credit

availability, cost of credit, and

lenders.

Explore strategies that may

be used to avoid bankruptcy

and what debt may not be

discharged through

bankruptcy.

Investigate common life

situations that lead to

financial difficulty and

bankruptcy.

Evaluate the methods that

debt collectors take in

recovering collateral from

borrowers.

Wisconsin Standards for Personal Financial Literacy 36

Content Area: Credit and Debt (CD)

Standard: PFL.CD2: Students will interpret lending options, consumer rights, and responsibilities.

Performance Indicators (by Grade Band)

Learning Priority K-2 (e) 3-5 (i) 6-8 (m) 9-12 (h)

CD2.a: Credit Products and

Services

CD2.a.e

Identify different forms of

payment methods (e.g.,

online, cash, debit card, credit

card, or loan).

Identify people from whom a

person could borrow an item.

CD2.a.i

Compare and give examples

of goods and services.

Explore situations where

people might pay for certain

items over time.

Examine why financial

institutions lend money.

Explain why using a credit

card is a form of borrowing.

Identify the sources of credit.

CD2.a.m

Compare the benefits and

costs of spending decisions

when selecting products or

services.

Differentiate between a

credit card, charge card, and

debit card.

Assess whether a specific

purchase justifies the use of

credit.

Evaluate potential

consequences of using easy

access credit.

Identify the financial benefits

and services of different

types of lending institutions.

CD2.a.h

Analyze the impact of using a

credit card versus debit card

as it relates to money

management.

Compare various types of

student loans, repayment

options, and alternatives of

paying for post-secondary

education or training.

Differentiate between

adjustable- and fixed-rate

debt.

Analyze the effect of debt on

a person’s net worth.

Calculate the most cost-

effective option for paying for

transportation.

CD2.b: High-Cost

Alternative Lending

CD2.b.i

Provide examples of

predatory lending practices

(e.g., deception, coercion,

misleading, exploitation, and

other unethical actions

toward an individual who

does not need, does not want,

or can’t afford the loan).