i

Uniform CPA Examination Blueprints

Uniform CPA Examination

®

Blueprints

Approved by the Board of Examiners

American Institute of CPAs

Oct. 23, 2020

Effective date: July 1, 2021

1

Uniform CPA Examination Blueprints

Table of contents

Uniform CPA Examination Blueprints

2 Introduction: Uniform CPA Examination Blueprints

AUD1 Auditing and Attestation (AUD)

AUD2 Section introduction

AUD6 Summary blueprint

AUD7 Area I — Ethics, Professional Responsibilities

and General Principles

AUD11 Area II — Assessing Risk and Developing

a Planned Response

AUD17 Area III — Performing Further Procedures

and Obtaining Evidence

AUD22 Area IV — Forming Conclusions and Reporting

BEC1 Business Environment and Concepts (BEC)

BEC2 Section introduction

BEC6 Summary blueprint

BEC7 Area I — Enterprise Risk Management, Internal Controls

and Business Processes

BEC10 Area II — Economics

BEC12 Area III — Financial Management

BEC14 Area IV — Information Technology

BEC17 Area V — Operations Management

FAR1 Financial Accounting and Reporting (FAR)

FAR2 Section introduction

FAR6 Summary blueprint

FAR7 Area I — Conceptual Framework, Standard-Setting

and Financial Reporting

FAR13 Area II — Select Financial Statement Accounts

FAR19 Area III — Select Transactions

FAR24 Area IV — State and Local Governments

REG1 Regulation (REG)

REG2 Section introduction

REG5 Summary blueprint

REG6 Area I — Ethics, Professional Responsibilities

and Federal Tax Procedures

REG8 Area II — Business Law

REG11 Area III — Federal Taxation of Property Transactions

REG14 Area IV — Federal Taxation of Individuals

REG16 Area V — Federal Taxation of Entities

2

Uniform CPA Examination Blueprints

The Uniform CPA Examination (the Exam) is comprised of four sections, each

four hours long: Auditing and Attestation (AUD), Business Environment and

Concepts (BEC), Financial Accounting and Reporting (FAR) and Regulation (REG).

The table below presents the design of the Exam by section, section time and

question type.

The table below presents the scoring weight of multiple-choice questions

(MCQs), task-based simulations (TBSs) and written communication for each

Exam section.

The AICPA has adopted a skill framework for the Exam based on the revised

Bloom’s Taxonomy of Educational Objectives. Bloom’s Taxonomy classies a

continuum of skills that students can be expected to learn and demonstrate.

Approximately 570 representative tasks that are critical to a newly licensed

CPA’s role in protecting the public interest have been identied. The

representative tasks combine both the applicable content knowledge and skills

required in the context of the work of a newly licensed CPA. Based on the nature

of a task, one of four skill levels, derived from the revised Bloom’s Taxonomy,

was assigned to each of the tasks, as follows:

Introduction

Uniform CPA Examination Blueprints

Section

Section

time

Multiple-choice

questions (MCQs)

Task-based

simulations (TBSs)

Written

communication

AUD 4 hours 72 8 —

BEC 4 hours 62 4 3

FAR 4 hours 66 8 —

REG 4 hours 76 8 —

Score weighting

Section

Multiple-choice

questions (MCQs)

Task-based

simulations (TBSs)

Written

communication

AUD 50% 50% —

BEC 50% 35% 15%

FAR 50% 50% —

REG 50% 50% —

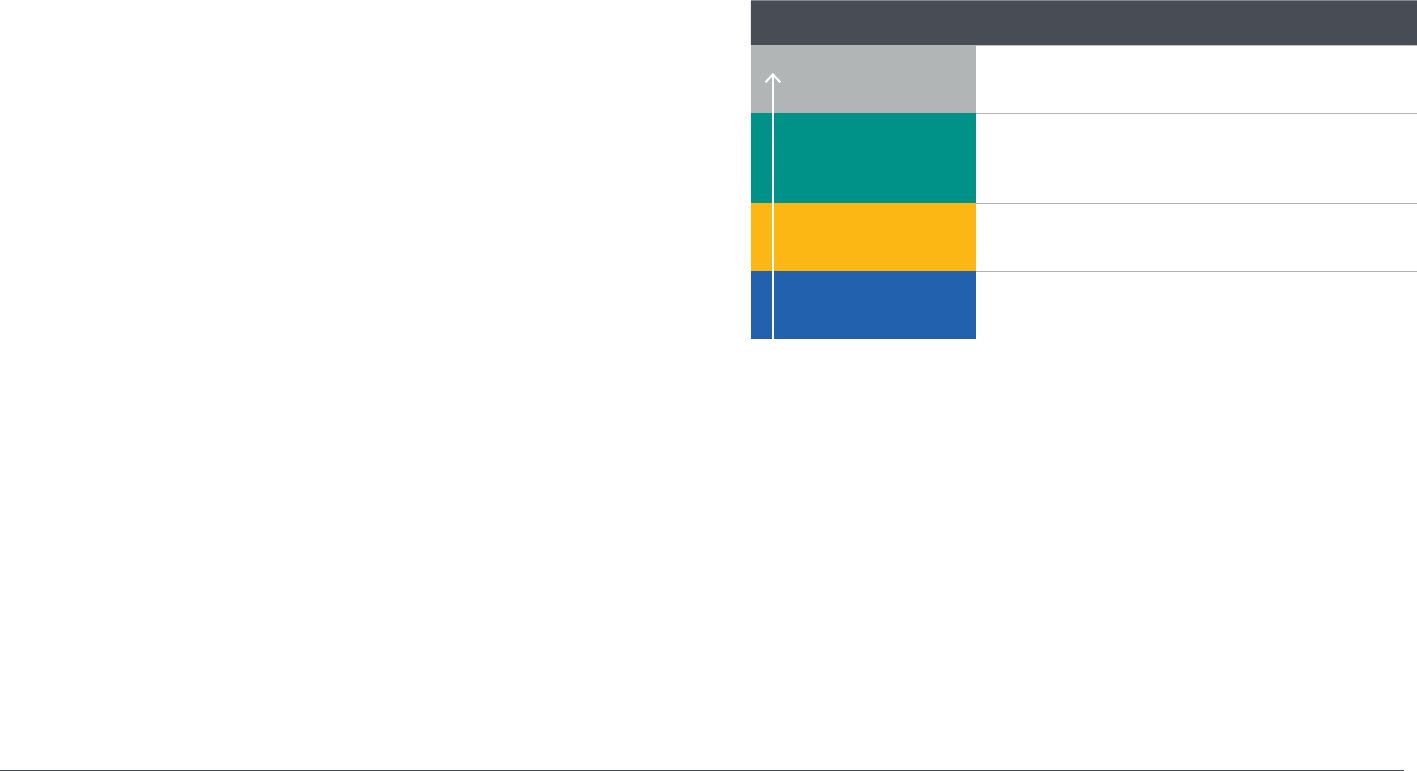

Skill levels

Evaluation

The examination or assessment of problems, and

use of judgment to draw conclusions.

Analysis

The examination and study of the interrelationships

of separate areas in order to identify causes and nd

evidence to support inferences.

Application

The use or demonstration of knowledge, concepts

or techniques.

Remembering and

Understanding

The perception and comprehension of the

signicance of an area utilizing knowledge gained.

Introduction

3

Uniform CPA Examination Blueprints

The skill levels to be assessed on each section of the Exam are included in the

table below.

*Includes written communication

The purpose of the blueprint is to:

• Document the minimum level of knowledge and skills necessary for initial

licensure.

• Assist candidates in preparing for the Exam by outlining the knowledge and

skills that may be tested.

• Apprise educators about the knowledge and skills candidates will need to

function as newly licensed CPAs.

• Guide the development of Exam questions.

The tasks in the blueprints are representative and are not intended to be (nor

should they be viewed as) an all-inclusive list of tasks that may be tested on

the Exam. It also should be noted that the number of tasks associated with a

particular content group or topic is not indicative of the extent such content

group, topic or related skill level will be assessed on the Exam.

Section

Remembering and

Understanding Application Analysis Evaluation

AUD 25–35% 30–40% 20–30% 5–15%

BEC 15–25% 50–60%* 20–30% —

FAR 10–20% 50–60% 25–35% —

REG 25–35% 35–45% 25–35% —

Each section of the Exam has a section introduction and a corresponding

section blueprint.

• The section introduction outlines the scope of the section, the content

organization and tasks, the content allocation, the overview of content areas,

the skill allocation and a listing of the section’s applicable reference literature.

• The section blueprint outlines the content to be tested, the associated skill

level to be tested and the representative tasks a newly licensed CPA would

need to perform to be considered competent. The blueprints are organized by

content AREA, content GROUP, and content TOPIC. Each topic includes one

or more representative TASKS that a newly licensed CPA may be expected to

complete.

Revised taxonomy see Anderson, L.W. (Ed.), Krathwohl, D.R. (Ed.), Airasian, P.W., Cruikshank, K.A., Mayer, R.E., Pintrich, P.R., Raths, J., & Wittrock, M.C. (2001). A taxonomy for learning, teaching, and assessing: A revision of Bloom’s Taxonomy of

Educational Objectives (Complete Edition). New York: Longman. For original taxonomy see Bloom, B.S. (Ed.), Engelhart, M.D., Furst, E.J., Hill, W.H., & Krathwohl, D.R. (1956). Taxonomy of educational objectives: The classication of educational

goals. Handbook 1: Cognitive domain. New York: David McKay.

Introduction

Uniform CPA Examination Blueprints (continued)

AUD1

Uniform CPA Examination Blueprints: Auditing and Attestation (AUD)

Uniform CPA Examination

Auditing and Attestation (AUD)

Blueprint

AUD2

Uniform CPA Examination Blueprints: Auditing and Attestation (AUD)

The Auditing and Attestation (AUD) section of the Uniform CPA Examination

(the Exam) tests the essential knowledge and skills a newly licensed CPA must

demonstrate when performing audit engagements, attestation engagements or

accounting and review service engagements.

Newly licensed CPAs are required to:

• demonstrate knowledge and skills related to professional responsibilities,

including ethics, independence and professional skepticism. Professional

skepticism reects an iterative process that includes a questioning mind and

a critical assessment of audit evidence.

• understand the entity including its operations, information systems (including

the use of third-party systems) and its underlying business processes, risks

and related internal controls.

• understand the ow of transactions and underlying data through a business

process and its related information systems.

Content organization and tasks

The AUD section blueprint is organized by content AREA, content GROUP and

content TOPIC. Each topic includes one or more representative TASKS that a newly

licensed CPA may be expected to complete when performing audit engagements,

attestation engagements or accounting and review service engagements.

The engagements tested under the AUD section of the Exam are performed in

accordance with professional standards and/or regulations promulgated by various

governing bodies A listing of standards promulgated by these bodies, and other

reference materials that are eligible for assessment in the AUD section of the Exam

are included under References at the conclusion of this introduction.

Candidates should be aware that the tasks included in the AUD blueprint may, and

typically do, relate to and can be applied to various engagement types

such as:

• Audit engagements - Financial statement audits as well as other types of audits

a newly licensed CPA may perform, such as compliance audits, audits of internal

control integrated with an audit of nancial statements and audits of entities

receiving federal grants. Audits may be for issuer entities subject to the audit

requirements set forth by the Public Company Accounting Oversight Board

(PCAOB), nonissuer entities subject to the audit requirements set forth by the

American Institute of CPA’s (AICPA) Auditing Standards Board or governmental

entities subject to the audit requirements of the U.S. Government Accountability

Ofce or the Ofce of Management and Budget.

• Attestation engagements - Examinations, reviews or agreed-upon procedures

engagements that a newly licensed CPA may perform in accordance with the

requirements set forth by the AICPA’s Auditing Standards Board.

• Accounting and review service engagements - Preparation, compilation and

review engagements that a newly licensed CPA may perform in accordance

with requirements set forth by the AICPA’s Accounting and Review Services

Committee.

For example, tasks related to Analytical procedures (included under Area III, Group

C, Topic 1) may be performed during a review engagement as a presumptively

mandatory procedure, or during an audit engagement as a substantive procedure,

or near the end of the engagement to assist with forming an overall conclusion on

the nancial statements.

The tasks in the blueprint are representative. They are not intended to be (nor

should they be viewed as) an all-inclusive list of tasks that may be tested in the

AUD section of the Exam. Additionally, it should be noted that the number of tasks

associated with a particular content group or topic is not indicative of the extent

such content group, topic or related skill level will be assessed on the Exam.

Similarly, examples provided within the task statements should not be viewed as

all-inclusive.

Section introduction

Auditing and Attestation

AUD3

Uniform CPA Examination Blueprints: Auditing and Attestation (AUD)

Content allocation

The following table summarizes the content areas and the allocation of content

tested in the AUD section of the Exam:

Overview of content areas

Area I of the AUD section blueprint covers several topics, including ethics,

independence and professional conduct and concepts relating to professional

skepticism and professional judgment. This area also includes the nature and

scope of an engagement, engagement terms, documentation, communication

requirements and quality control.

The remaining three areas of the AUD section blueprint (Areas II, III and IV)

cover the activities that a newly licensed CPA should be able to perform when

providing professional services related to audit, attestation and accounting

and review service engagements. The organization of these sections follows a

typical engagement process, from planning through reporting.

Area II of the AUD section blueprint covers planning, risk assessment and

design of procedures responsive to identied risks. The area is focused on

obtaining an understanding of an entity, its environment (internal and external),

business processes, information systems and internal controls (manual and

automated) in order to appropriately assess the risk of material misstatement

due to fraud or errors and to design appropriate procedures to respond to those

identied risks.

Area III of the AUD section blueprint covers performing planned engagement

procedures that are responsive to identied risk. The area is focused on

concluding on the sufciency and appropriateness of evidence obtained by

performing general procedures (e.g. observation, reperformance, sampling,

etc.) and specic procedures (e.g. analytical procedures, external conrmation

and audit data analytics). This area also covers testing the operating

effectiveness of internal controls, responding to specic matters that require

special consideration (e.g. accounting estimates, inventory, etc.), evaluating and

responding to misstatements and internal control deciencies.

Area IV of the AUD section blueprint covers the reporting requirements for

audit, attestation and accounting and review service engagements. This area

also includes other reporting considerations such as comparative nancial

statements, consistency, supplementary information and special considerations

when performing engagements under Government Auditing Standards.

Section assumptions

When completing multiple-choice questions, task-based simulations and

research prompts in the AUD section of the Exam, candidates should be aware

of the entity type and engagement type presented in the question. To the extent

that there are different requirements for an entity under audit or review, the

question will include an explicit reference to the entity type (issuer or nonissuer).

Questions may refer to an audit engagement by including phrases such as

“an audit of a nonissuer” or “an audit of an issuer”. Questions will refer to other

types of engagements by including phrases such as “examination of pro forma

nancial information”, “review engagement”, “interim review”, “compilation

engagement”, etc. The use of the terms “auditor”, “accountant” or “practitioner”

will also be used to further identify engagement types and applicable

professional standards. Candidates should be mindful of the engagement type

when answering a question.

Section introduction

Auditing and Attestation (continued)

Content area Allocation

Area I

Ethics, Professional Responsibilities

and General Principles

15–25%

Area II

Assessing Risk and Developing a Planned

Response

25–35%

Area III

Performing Further Procedures and

Obtaining Evidence

30–40%

Area IV

Forming Conclusions and Reporting

10–20%

AUD4

Uniform CPA Examination Blueprints: Auditing and Attestation (AUD)

Skill allocation

The Exam focuses on testing higher order skills. Based on the nature of the task,

each representative task in the AUD section blueprint is assigned a skill level.

AUD section considerations related to the skill levels are discussed below.

• Remembering and Understanding is mainly concentrated in Area I and Area IV.

These areas contain much of the general audit knowledge that is required for

newly licensed CPAs. In Area IV, many of the tasks relate to reporting and are

driven by templates and illustrative examples.

• Application is tested in all four areas of the AUD section. Application

tasks focus on general topics such as professional responsibilities and

documentation, and the day-to-day tasks that newly licensed CPAs perform,

frequently using standardized application tools such as audit programs and

sampling techniques.

• Analysis and Evaluation skills, tested in Area II and Area III, involve tasks that

require a higher level of analysis and interpretation. These tasks, such as

concluding on sufciency and appropriateness of evidence, frequently require

newly licensed CPAs to apply professional skepticism and judgment.

The representative tasks combine both the applicable content knowledge and

the skills required in the context of the work that a newly licensed CPA would

reasonably be expected to perform.

Section introduction

Auditing and Attestation (continued)

Skill levels

Evaluation

The examination or assessment of problems, and

use of judgment to draw conclusions.

Analysis

The examination and study of the interrelationships

of separate areas in order to identify causes and nd

evidence to support inferences.

Application

The use or demonstration of knowledge, concepts

or techniques.

Remembering and

Understanding

The perception and comprehension of the

signicance of an area utilizing knowledge gained.

AUD5

Uniform CPA Examination Blueprints: Auditing and Attestation (AUD)

References — Auditing and Attestation

• AICPA Statements on Auditing Standards and Interpretations

• Public Company Accounting Oversight Board (PCAOB) Standards (SEC-Approved)

and Related Rules, PCAOB Staff Questions and Answers and PCAOB Staff Audit

Practice Alerts

• U.S. Government Accountability Ofce Government Auditing Standards

• Single Audit Act, as amended

• Ofce of Management and Budget (OMB) Audit requirements for Federal

Awards (2 CFR 200)

• AICPA Statements on Quality Control Standards

• AICPA Statements on Standards for Accounting and Review Services and

Interpretations

• AICPA Statements on Standards for Attestation Engagements and Interpretations

• AICPA Audit and Accounting Guides

• AICPA Code of Professional Conduct

• Sarbanes-Oxley Act of 2002

• U.S. Department of Labor (DOL) Guidelines and Interpretive Bulletins re: Auditor

Independence

• SEC Independence Rules

• Employee Retirement Income Security Act of 1974

• The Committee of Sponsoring Organizations of the Treadway Commission

(COSO): Internal Control — Integrated Framework

• Current textbooks on auditing, attestation services, ethics and independence

Section introduction

Auditing and Attestation (continued)

AUD6

Uniform CPA Examination Blueprints: Auditing and Attestation (AUD)

Content area allocation Weight

I. Ethics, Professional Responsibilities and General Principles 15–25%

II. Assessing Risk and Developing a Planned Response 25–35%

III. Performing Further Procedures and Obtaining Evidence 30–40%

IV. Forming Conclusions and Reporting 10–20%

Skill allocation Weight

Evaluation 5–15%

Analysis 20–30%

Application 30–40%

Remembering and Understanding 25–35%

Auditing and Attestation (AUD)

Summary blueprint

AUD7

Uniform CPA Examination Blueprints: Auditing and Attestation (AUD)

Auditing and Attestation (AUD)

Area I — Ethics, Professional Responsibilities

and General Principles (15–25%)

Skill

Content group/topic

Remembering and

Understanding

Application Analysis Evaluation Representative task

A. Nature and scope

1. Nature and scope: audit

engagements

Identify the nature, scope and objectives of the different types of audit engagements,

including issuer and nonissuer audits.

2. Nature and scope:

engagements conducted

under Government

Accountability Ofce

Government Auditing

Standards

Identify the nature, scope and objectives of engagements performed in accordance

with Government Accountability Ofce Government Auditing Standards.

3. Nature and scope: other

engagements

Identify the nature, scope and objectives of attestation engagements and accounting

and review service engagements.

B. Ethics, independence and professional conduct

1. AICPA Code of

Professional

Conduct

Understand the principles, rules and interpretations included in the AICPA Code of

Professional Conduct.

Recognize situations that present threats to compliance with the AICPA Code of

Professional Conduct, including threats to independence.

Apply the principles, rules and interpretations included in the AICPA Code of

Professional Conduct to given situations.

Apply the Conceptual Framework for Members in Public Practice included in the AICPA

Code of Professional Conduct to situations that could present threats to compliance with

the rules included in the Code.

Apply the Conceptual Framework for Members in Business included in the AICPA

Code of Professional Conduct to situations that could present threats to compliance

with the rules included in the Code.

Apply the Conceptual Framework for Independence included in the AICPA Code

of Professional Conduct to situations that could present threats to compliance with

the rules included in the Code.

AUD8

Uniform CPA Examination Blueprints: Auditing and Attestation (AUD)

Skill

Content group/topic

Remembering and

Understanding

Application Analysis Evaluation Representative task

B. Ethics, independence and professional conduct (continued)

2. Requirements of the

Securities and

the Exchange Commission

and the Public Company

Accounting Oversight Board

Understand the ethical requirements of the Securities and Exchange Commission

and the Public Company Accounting Oversight Board.

Recognize situations that present threats to compliance with the ethical requirements

of the Securities and Exchange Commission and the Public Company Accounting

Oversight Board.

Apply the ethical requirements and independence rules of the Securities and

Exchange Commission and the Public Company Accounting Oversight Board to

situations that could present threats to compliance during an audit of an issuer.

3. Requirements of the

Government

Accountability Ofce

and the Department

of Labor

Recognize situations that present threats to compliance with the ethical

requirements of the Government Accountability Ofce Government Auditing

Standards.

Recognize situations that present threats to compliance with the ethical

requirements of the Department of Labor.

Apply the ethical requirements and independence rules of the Government

Accountability Ofce Government Auditing Standards to situations that could

present threats to compliance during an audit of, or attestation engagement for, a

government entity or an entity receiving federal awards.

Apply the independence rules of the Department of Labor to situations that could

present threats to compliance during an audit of employee benet plans.

4. Professional skepticism

and professional judgment

Understand the concepts of professional skepticism and professional judgment.

Understand personal bias and other impediments to acting with professional

skepticism, such as threats, incentives and judgment-making shortcuts.

Auditing and Attestation (AUD)

Area I — Ethics, Professional Responsibilities

and General Principles (15–25%) (continued)

AUD9

Uniform CPA Examination Blueprints: Auditing and Attestation (AUD)

Skill

Content group/topic

Remembering and

Understanding

Application Analysis Evaluation Representative task

C. Terms of engagement

1. Preconditions for an

engagement

Identify the preconditions needed for accepting or continuing an engagement.

2. Terms of engagement

and engagement letter

Identify the factors affecting the acceptance or continuance of an engagement.

Identify the factors to consider when management requests a change in the type of

engagement (e.g., from an audit to a review).

Perform procedures to conrm that a common understanding of the terms of an

engagement exist with management and those charged with governance.

Document the terms of an engagement in a written engagement letter or other

suitable form of written agreement.

D. Requirements for engagement documentation

Identify the elements that comprise sufcient appropriate documentation for an

engagement.

Identify the requirements for the assembly and retention of documentation for an

engagement.

Prepare documentation that is sufcient to enable an experienced auditor having no

previous connection with an engagement to understand the nature, timing, extent

and results of procedures performed and the signicant ndings and conclusions

reached.

Auditing and Attestation (AUD)

Area I — Ethics, Professional Responsibilities

and General Principles (15–25%) (continued)

AUD10

Uniform CPA Examination Blueprints: Auditing and Attestation (AUD)

Skill

Content group/topic

Remembering and

Understanding

Application Analysis Evaluation Representative task

E. Communication with management and those charged with governance

1. Planned scope

and timing of an

engagement

Identify the matters related to the planned scope and timing of an engagement that

should be communicated to management and those charged with governance.

Prepare presentation materials and supporting schedules for use in communicating

the planned scope and timing of an engagement to management and those charged

with governance.

2. Internal control

related matters

Identify the matters related to deciencies and material weaknesses in internal

control that should be communicated to those charged with governance and

management for an engagement and the timing of such communications.

Prepare written communication materials for use in communicating identied

internal control deciencies and material weaknesses for an engagement to those

charged with governance and management.

F. A rm’s system of quality control, including quality control at the engagement level

Recognize a CPA rm’s responsibilities for its accounting and auditing practice’s

system of quality control.

Apply quality control procedures on an engagement.

Auditing and Attestation (AUD)

Area I — Ethics, Professional Responsibilities

and General Principles (15–25%) (continued)

AUD11

Uniform CPA Examination Blueprints: Auditing and Attestation (AUD)

Auditing and Attestation (AUD)

Area II — Assessing Risk and Developing

a Planned Response (25–35%)

Skill

Content group/topic

Remembering and

Understanding

Application Analysis Evaluation Representative task

A. Planning an engagement

1. Developing an

overall engagement

strategy

Explain the purpose and signicance of the overall engagement strategy for an

engagement.

2. Developing a detailed

engagement plan

Prepare a detailed engagement plan for an engagement starting with the prior-year

engagement plan or with a template.

Prepare supporting planning related materials (e.g., client assistance request listings,

time budgets) for a detailed engagement plan starting with the prior-year engagement

plan or with a template.

B. Understanding an entity and its environment

1. External factors

Identify the relevant external factors. (e.g., industry, regulation, applicable nancial

reporting framework and technology) that impact an entity and/or the inherent risk

of material misstatement, and document the procedures performed to obtain that

understanding.

2. Internal factors

Identify the relevant factors that dene the nature of an entity, including the impact

on the risk of material misstatement (e.g., its operations, ownership and governance

structure, investment and nancing plans, selection of accounting policies and

objectives and strategies) and document the procedures performed to obtain that

understanding.

Obtain an understanding of an entity’s IT systems infrastructure (e.g., ERP, cloud

computing or hosting arrangements, custom or packaged applications) and document

the procedures performed to obtain that understanding.

Identify and document the signicant business processes and data ows that directly

or indirectly impact an entity’s nancial statements.

AUD12

Uniform CPA Examination Blueprints: Auditing and Attestation (AUD)

Auditing and Attestation (AUD)

Skill

Content group/topic

Remembering and

Understanding

Application Analysis Evaluation Representative task

C. Understanding an entity’s control environment and business processes, including information technology (IT) systems

1. Control environment,

IT general controls and

entity-level controls

Identify the signicant components of an entity’s control environment, including its

IT general controls and entity-level controls, and document the procedures performed

to obtain that understanding.

2. Business processes

and the design of internal

controls, including IT

systems

Perform a walkthrough of a signicant business process and document (e.g., ow

charts, process diagrams, narratives) the ow of relevant transactions and data from

initiation through nancial statement reporting and disclosure.

Obtain an understanding of IT systems that are, directly or indirectly, the source of

nancial transactions or the data used to record nancial transactions (e.g. how the

entity uses IT systems to capture, store, and process information) and document the

procedures performed to obtain that understanding.

Perform tests of the design and implementation of relevant internal controls

(application and manual).

Identify and document an entity’s relevant IT application controls within the ow of

an entity’s transactions for a signicant business process and consider the effect of

these controls on the completeness, accuracy and reliability of an entity’s data.

Identify and document the relevant manual controls within the ow of an entity’s

transactions for a signicant business process and consider the effect of these

controls on the completeness, accuracy and reliability of an entity’s data.

Evaluate whether relevant internal controls (application and manual) are effectively

designed and placed in operation.

Area II — Assessing Risk and Developing

a Planned Response (25–35%) (continued)

AUD13

Uniform CPA Examination Blueprints: Auditing and Attestation (AUD)

Auditing and Attestation (AUD)

Skill

Content group/topic

Remembering and

Understanding

Application Analysis Evaluation Representative task

C. Understanding an entity’s control environment and business processes, including information technology (IT) systems (continued)

3. Implications of an

entity using a

service organization

Understand the differences between SOC 1

®

and SOC 2

®

engagements.

Identify and document the purpose and signicance of an entity’s use of a service

organization, including the impact of using a SOC 1

®

Type 2 report in an audit of an

entity’s nancial statements.

Use a SOC 1

®

Type 2 report to determine the nature and extent of testing procedures

to be performed in an audit of an entity’s nancial statements.

4. Limitations of

controls and risk of

management

override

Understand the limitations of internal controls and the potential impact on the risk of

material misstatement of an entity’s nancial statements.

Identify and document the risks associated with management override of internal

controls and the potential impact on the risk of material misstatement of an entity’s

nancial statements.

D. Assessing risks due to fraud, including discussions among the engagement team about the risk of material misstatement due to fraud or error

Assess risks of material misstatement of an entity’s nancial statements due to fraud

or error (e.g., during a brainstorming session), leveraging the combined knowledge

and understanding of the engagement team.

E. Identifying and assessing the risk of material misstatement, whether due to error or fraud, and planning further procedures responsive to identied risks

1. Impact of risks at

the nancial

statement level

Identify and document the assessed impact of risks of material misstatement at the

nancial statement level, taking into account the effect of relevant controls.

Analyze identied risks to detect those that relate to an entity’s nancial statements

as a whole (as contrasted to the relevant assertion level).

Area II — Assessing Risk and Developing

a Planned Response (25–35%) (continued)

AUD14

Uniform CPA Examination Blueprints: Auditing and Attestation (AUD)

Auditing and Attestation (AUD)

Skill

Content group/topic

Remembering and

Understanding

Application Analysis Evaluation Representative task

E. Identifying and assessing the risk of material misstatement, whether due to error or fraud, and planning further procedures responsive to identied risks (continued)

2. Impact of risks

for each relevant

assertion at the

class of transaction,

account balance

and disclosure

levels

Identify and document risks and related controls at the relevant assertion level for

signicant classes of transactions, account balances and disclosures in an entity’s

nancial statements.

Analyze the potential impact of identied risks at the relevant assertion level for

signicant classes of transactions, account balances and disclosures in an entity’s

nancial statements, taking account of the controls the auditor intends to test.

3. Further procedures

responsive to

identied risks

Develop planned audit procedures that are responsive to identied risks of material

misstatement due to fraud or error at the relevant assertion level for signicant

classes of transactions and account balances.

Analyze the risk of material misstatement, including the potential impact of

individual and cumulative misstatements, to provide a basis for developing planned

audit procedures.

Analyze transactions that may have a higher risk of material misstatement from

audit data analytic outputs (e.g., reports and visualizations) by determining

relationships among variables and interpreting results to provide a basis for

developing planned audit procedures.

F. Materiality

1. For the nancial

statements as a

whole

Understand materiality as it relates to the nancial statements as a whole.

Calculate materiality for an entity’s nancial statements as a whole.

Calculate the materiality level (or levels) to be applied to classes of transactions,

account balances and disclosures in an audit of an issuer or nonissuer.

Area II — Assessing Risk and Developing

a Planned Response (25–35%) (continued)

AUD15

Uniform CPA Examination Blueprints: Auditing and Attestation (AUD)

Auditing and Attestation (AUD)

Skill

Content group/topic

Remembering and

Understanding

Application Analysis Evaluation Representative task

F. Materiality (continued)

2. Tolerable misstatement

and performance

materiality

Understand the use of tolerable misstatement or performance materiality in an audit

of an issuer or nonissuer.

Calculate tolerable misstatement or performance materiality for the purposes of

assessing the risk of material misstatement and determining the nature, timing and

extent of further audit procedures in an audit of an issuer or nonissuer.

G. Planning for and using the work of others

Identify the factors to consider in determining the extent to which an engagement

team can use the work of the internal audit function, IT auditor, auditor’s specialist or a

component auditor.

Determine the nature and scope of the work of the internal audit function, IT auditor,

auditor’s specialist or component auditor.

Perform and document procedures to determine the extent to which an engagement

team can use the work of the internal audit function, IT auditor, auditor’s specialist or

a component auditor to obtain evidence.

Area II — Assessing Risk and Developing

a Planned Response (25–35%) (continued)

AUD16

Uniform CPA Examination Blueprints: Auditing and Attestation (AUD)

Auditing and Attestation (AUD)

Skill

Content group/topic

Remembering and

Understanding

Application Analysis Evaluation Representative task

H. Specic areas of engagement risk

1. An entity’s

compliance with

laws and

regulations,

including possible

illegal acts

Understand the accountant’s responsibilities with respect to laws and regulations

that have a direct effect on the determination of material amounts or disclosures in

an entity’s nancial statements for an engagement.

Understand the accountant’s responsibilities with respect to laws and regulations that

are fundamental to an entity’s business but do not have a direct effect on the entity’s

nancial statements in an engagement.

Perform tests of compliance with laws and regulations that have a direct effect on

material amounts or disclosures in an entity’s nancial statements in an engagement.

Perform tests of compliance with laws and regulations that are fundamental to an

entity’s business, but do not have a direct effect on the entity’s nancial statements for

an engagement.

2.

Accounting

estimates

Recognize the potential impact of lower complexity and higher complexity signicant

accounting estimates on the risk of material misstatement, including the indicators of

management bias.

3. Related parties

and related party

transactions

Perform procedures to identify related party relationships and transactions, including

consideration of signicant unusual transactions and transactions with executive

ofcers.

Area II — Assessing Risk and Developing

a Planned Response (25–35%) (continued)

AUD17

Uniform CPA Examination Blueprints: Auditing and Attestation (AUD)

Auditing and Attestation (AUD)

Skill

Content group/topic

Remembering and

Understanding

Application Analysis Evaluation Representative task

A. Sufcient appropriate evidence

Determine the sources of sufcient appropriate evidence (e.g., generated from management’s

nancial reporting system, obtained from management specialists, obtained from external sources or

developed by the audit team from internal or external sources).

Identify procedures to validate the completeness and accuracy of data and information obtained from

management (e.g., tying information back to original sources such as general ledger, subledger or

external information sources, validate search or query criteria used to obtain data, etc.)

Exercise professional skepticism and professional judgment while analyzing the data and information

to be used as evidence to determine whether it is sufciently reliable and corroborates or contradicts

the assertions in the nancial statements and the objectives of the engagement and modify planned

procedures accordingly.

Evaluate whether sufcient appropriate evidence has been obtained to achieve the objectives of the

planned procedures.

B. General procedures to obtain sufcient appropriate evidence

Understand the purpose and application of sampling techniques including the use of automated tools

and audit data analytic techniques to identify signicant events or transactions that may impact the

nancial statements.

Use sampling techniques to extrapolate the characteristics of a population from a sample of items.

Use observation and inspection to obtain evidence.

Use recalculation (e.g., manually or using automated tools and techniques) to test the mathematical

accuracy of information to obtain evidence.

Use reperformance to independently execute procedures or controls to obtain evidence.

Inquire of management and others to gather evidence and document the results.

Analyze responses obtained during structured interviews or informal conversations with management

and others, including those in non-nancial roles, and ask relevant and effective follow-up questions to

understand their perspectives and motivations.

Area III — Performing Further Procedures and

Obtaining Evidence

(

30–40%

)

AUD18

Uniform CPA Examination Blueprints: Auditing and Attestation (AUD)

Auditing and Attestation (AUD)

Area III — Performing Further Procedures and

Obtaining Evidence

(

30–40%

)

(continued)

Skill

Content group/topic

Remembering and

Understanding

Application Analysis Evaluation Representative task

B. General procedures to obtain sufcient appropriate evidence (continued)

Perform tests of operating effectiveness of internal controls, including the analysis of exceptions to

identify deciencies in an audit of nancial statements or an audit of internal control.

C. Specic procedures to obtain sufcient appropriate evidence

1. Analytical

procedures

Determine the suitability of substantive analytical procedures to provide evidence to support an

identied assertion.

Develop an expectation of recorded amounts or ratios when performing analytical procedures and

determine whether the expectation is sufciently precise to identify a misstatement in the entity’s

nancial statements or disclosures.

Perform analytical procedures during engagement planning.

Perform analytical procedures near the end of an audit engagement that assist the auditor when

forming an overall conclusion about whether the nancial statements are consistent with the auditor’s

understanding of the entity.

Evaluate the reliability of data from which an expectation of recorded amounts or ratios is developed

when performing analytical procedures.

Evaluate the signicance of the differences of recorded amounts from expected values when

performing analytical procedures.

2. External

conrmations

Conrm signicant account balances and transactions using appropriate tools and techniques

(e.g., conrmation services, electronic conrmations, manual conrmations) to obtain relevant and

reliable evidence.

Analyze external conrmation responses in the audit of an issuer or nonissuer to determine the need

for follow-up or further investigation.

AUD19

Uniform CPA Examination Blueprints: Auditing and Attestation (AUD)

Auditing and Attestation (AUD)

Area III — Performing Further Procedures and

Obtaining Evidence (30–40%) (continued)

Skill

Content group/topic

Remembering and

Understanding

Application Analysis Evaluation Representative task

C. Specic procedures to obtain sufcient appropriate evidence (continued)

3. Audit data

analytics

Verify the accuracy and completeness of data sets that are used in an engagement to

complete planned procedures.

Determine the attributes, structure and sources of data needed to complete audit data

analytic procedures.

Perform procedures using outputs (e.g., reports and visualizations) from audit data

analytic techniques to determine relationships among variables, interpret results, and

determine additional procedures to be performed.

D. Specic matters that require special consideration

1. Accounting

estimates

Recalculate and reperform procedures to validate the inputs and assumptions of an

entity’s signicant accounting estimates with a higher risk of material misstatement or

complexity, such as fair value estimates.

Perform procedures (e.g. reviewing the work of a specialist and procedures performed

by the engagement team) to validate an entity’s calculations and detailed support

for signicant accounting estimates in an audit of an issuer or nonissuer, including

consideration of information that contradicts assumptions made by management.

Evaluate the reasonableness of signicant accounting estimates with a lower risk of

material misstatement or complexity in an audit or an issuer or nonissuer.

2. Investments

in securities

Identify the considerations relating to the measurement and disclosure of the fair value

of investments in securities in an audit of an issuer or nonissuer.

Test management’s assumptions, conclusions and adjustments related to the valuation

of investments in securities in an audit of an issuer or nonissuer.

AUD20

Uniform CPA Examination Blueprints: Auditing and Attestation (AUD)

Auditing and Attestation (AUD)

Area III — Performing Further Procedures and

Obtaining Evidence (30–40%) (continued)

Skill

Content group/topic

Remembering and

Understanding

Application Analysis Evaluation Representative task

D. Specic matters that require special consideration (continued)

3. Inventory and

inventory held

by others

Analyze management’s instructions and procedures for recording and controlling the

results of an entity’s physical inventory counting in an audit of an issuer or nonissuer.

Observe the performance of inventory counting procedures, inspect the inventory and

perform test counts to verify the ending inventory quantities in an audit of an issuer or

nonissuer.

4. Litigation, claims

and assessments

Perform appropriate audit procedures, such as inquiring of management and others,

reviewing minutes and sending external conrmations, to detect the existence of

litigation, claims and assessments in an audit of an issuer or nonissuer.

5. An entity’s ability

to continue as a

going concern

Identify factors that should be considered while performing planned procedures that may

indicate substantial doubt about an entity’s ability to continue as a going concern for a

reasonable period of time.

E. Misstatements and internal control deciencies

Prepare a summary of corrected and uncorrected misstatements.

Determine the effect of uncorrected misstatements on an entity’s nancial statements in

an engagement.

Determine the effect of identied misstatements on the assessment of internal control

over nancial reporting in an audit of an issuer or nonissuer.

Evaluate the signicance of internal control deciencies on the risk of material

misstatement of nancial statements in an audit of an issuer or nonissuer.

AUD21

Uniform CPA Examination Blueprints: Auditing and Attestation (AUD)

Auditing and Attestation (AUD)

Area III — Performing Further Procedures and

Obtaining Evidence (30–40%) (continued)

Skill

Content group/topic

Remembering and

Understanding

Application Analysis Evaluation Representative task

F. Written representations

Identify the written representations that should be obtained from management or those

charged with governance in an engagement.

G. Subsequent events and subsequently discovered facts

Recall the impact of subsequently discovered facts on the auditor’s report.

Perform procedures to identify subsequent events that should be reected in an entity’s

current period nancial statements and disclosures.

Determine whether identied subsequent events are appropriately reected in an entity’s

nancial statements and disclosures.

AUD22

Uniform CPA Examination Blueprints: Auditing and Attestation (AUD)

Auditing and Attestation (AUD)

Area IV — Forming Conclusions and Reporting

(10–20%)

Skill

Content group/topic

Remembering and

Understanding

Application Analysis Evaluation Representative task

A. Reports on auditing engagements

1. Forming an audit

opinion, including

modication of an

auditor’s opinion

Identify the factors that an auditor should consider when forming an opinion on an entity’s

nancial statements.

Identify the type of opinion that an auditor should render on the audit of an issuer or

nonissuer’s nancial statements, including unmodied (or unqualied), qualied, adverse

or disclaimer of opinion.

Identify the factors that an auditor should consider when it is necessary to modify the

audit opinion on an issuer or nonissuer’s nancial statements, including when the nancial

statements are materially misstated and when the auditor is unable to obtain sufcient

appropriate audit evidence.

2. Form and content

of an audit report,

including the use of

emphasis-of-matter

and other-matter

(explanatory)

paragraphs

Identify the appropriate form and content of an auditor’s report for an audit of

an issuer or nonissuer’s nancial statements, including the appropriate use of

emphasis-of-matter and other-matter (i.e., explanatory) paragraphs.

Prepare a draft auditor’s report starting with a report example (e.g., an illustrative audit

report from professional standards) for an audit of an issuer or nonissuer.

3. Audit of

internal control

integrated with an

audit of nancial

statements

Identify the factors that an auditor should consider when forming an opinion on the

effectiveness of internal control in an audit of internal control.

Identify the appropriate form and content of a report on the audit of internal control,

including report modications and the use of separate or combined reports for the audit

of an entity’s nancial statements and the audit of internal control.

Prepare a draft report for an audit of internal control integrated with the audit of an

entity’s nancial statements, starting with a report example (e.g., an illustrative report

from professional standards).

AUD23

Uniform CPA Examination Blueprints: Auditing and Attestation (AUD)

Auditing and Attestation (AUD)

Area IV — Forming Conclusions and Reporting

(10–20%) (continued)

Skill

Content group/topic

Remembering and

Understanding

Application Analysis Evaluation Representative task

B. Reports on attestation engagements

1. General standards

for attestation

reports

Identify the factors that a practitioner should consider when issuing an examination or

review report for an attestation engagement.

Prepare a draft examination or review report for an attestation engagement starting with

a report example (e.g., an illustrative report from professional standards).

2. Agreed-upon

procedures

reports

Identify the factors that a practitioner should consider when issuing an agreed-upon

procedures report for an attestation engagement.

Prepare a draft agreed-upon procedures report for an attestation engagement starting

with a report example (e.g., an illustrative report from professional standards).

3. Reporting on

controls at a

service organization

Identify the factors that a service auditor should consider when reporting on the

examination of controls at a service organization.

Prepare a draft report for an engagement to report on the examination of controls at

a service organization, starting with a report example (e.g., an illustrative report from

professional standards).

AUD24

Uniform CPA Examination Blueprints: Auditing and Attestation (AUD)

Auditing and Attestation (AUD)

Area IV — Forming Conclusions and Reporting

(10–20%) (continued)

Skill

Content group/topic

Remembering and

Understanding

Application Analysis Evaluation Representative task

C. Accounting and review service engagements

1. Preparation

engagements

Identify the factors that an accountant should consider when performing a preparation

engagement.

2. Compilation

reports

Identify the factors that an accountant should consider when reporting on an

engagement to compile an entity’s nancial statements, including the proper form

and content of the compilation report.

Prepare a draft report for an engagement to compile an entity’s nancial statements,

starting with a report example (e.g., an illustrative report from professional standards).

3. Review reports

Identify the factors that an accountant should consider when reporting on an engagement

to review an entity’s nancial statements, including the proper form and content of the

review report.

Prepare a draft report for an engagement to review an entity’s nancial statements,

starting with a report example (e.g., an illustrative report from professional standards).

AUD25

Uniform CPA Examination Blueprints: Auditing and Attestation (AUD)

Auditing and Attestation (AUD)

Area IV — Forming Conclusions and Reporting

(10–20%) (continued)

Skill

Content group/topic

Remembering and

Understanding

Application Analysis Evaluation Representative task

D. Reporting on compliance

Identify the factors that an auditor should consider when reporting on compliance with

aspects of contractual agreements or regulatory requirements in connection with an audit

of an entity’s nancial statements.

Identify the factors that a practitioner should consider when reporting on an attestation

engagement related to an entity’s compliance with the requirements of specied laws,

regulations, rules, contracts or grants, including reports on the effectiveness of internal

controls over compliance with the requirements.

E. Other reporting considerations

1. Comparative

statements and

consistency

between periods

Identify the factors that would affect the comparability or consistency of nancial

statements, including a change in accounting principle, the correction of a material

misstatement and a material change in classication.

2. Other information

in documents with

audited statements

Understand the auditor’s responsibilities related to other information included in

documents with audited nancial statements.

3. Review of interim

nancial

information

Identify the factors an auditor should consider when reporting on an engagement to

review interim nancial information.

4. Supplementary

information

Identify the factors an auditor should consider when reporting on supplementary

information included in or accompanying an entity’s nancial statements.

AUD26

Uniform CPA Examination Blueprints: Auditing and Attestation (AUD)

Auditing and Attestation (AUD)

Area IV — Forming Conclusions and Reporting

(10–20%) (continued)

Skill

Content group/topic

Remembering and

Understanding

Application Analysis Evaluation Representative task

E. Other reporting considerations (continued)

5. Additional reporting

requirements

under Government

Accountability

Ofce Government

Auditing Standards

Identify requirements under Government Accountability Ofce Government Auditing

Standards related to reporting on internal control over nancial reporting and compliance

with provisions of the law, regulations, contracts and grant agreements that have a

material effect on the nancial statements.

6. Special-purpose

and other country

frameworks

Identify the factors an auditor should consider when reporting on the audit of nancial

statements prepared in accordance with a nancial reporting framework generally

accepted in another country, when the nancial statements are intended for use outside

of the United States.

Identify the factors an auditor should consider when reporting on the audit of nancial

statements prepared in accordance with a special-purpose framework, including cash

basis, tax basis, regulatory basis, contractual basis or other basis.

BEC1

Uniform CPA Examination Blueprints: Business Environment and Concepts (BEC)

Uniform CPA Examination

Business Environment and

Concepts (BEC)

Blueprint

BEC2

Uniform CPA Examination Blueprints: Business Environment and Concepts (BEC)

The Business Environment and Concepts (BEC) section of the Uniform CPA

Examination (the Exam) tests knowledge and skills that a newly licensed CPA

must demonstrate when performing:

• Audit, attest, accounting and review services

• Financial reporting

• Tax preparation

• Other professional services

The content areas tested under the BEC section of the Exam encompass ve

diverse subject areas. These content areas are enterprise risk management,

internal controls and business processes, economics, nancial management,

information technology and operations management. Reference materials

relevant to the BEC section of the Exam are included under References at the

conclusion of this introduction.

Content organization and tasks

The BEC section blueprint is organized by content AREA, content GROUP and

content TOPIC. Each group or topic includes one or more representative TASKS

that a newly licensed CPA may be expected to complete when performing audit,

attest, accounting and review services, nancial reporting, tax preparation or

other professional services.

The tasks in the blueprint are representative. They are not intended to be (nor

should they be viewed as) an all-inclusive list of tasks that may be tested in the

BEC section of the Exam. Additionally, it should be noted that the number of

tasks associated with a particular content group or topic is not indicative of

the extent such content group, topic or related skill level will be assessed

on the Exam. Similarly, examples provided within the task statements should

not be viewed as all-inclusive.

Content allocation

The following table summarizes the content areas and the allocation of content

tested in the BEC section of the Exam:

Overview of content areas

Area I of the BEC section blueprint covers several topics related to Enterprise

Risk Management, Internal Controls and Business Processes, including the

following:

• Recalling concepts from and applying enterprise risk management

• Recalling concepts from and applying internal controls

• Recalling and applying key corporate governance provisions of the Sarbanes-

Oxley Act of 2002

• Describing the types and purposes of accounting and nancial reporting

information systems and related tools and software

• Identifying aspects of an entity’s manual and automated business processes

and controls

• Analyzing the ow of transactions to identify the risks in key business

processes

Section introduction

Business Environment and Concepts

Content area Allocation

Area I

Enterprise Risk Management, Internal

Controls and Business Processes

20–30%

Area II

Economics

15–25%

Area III

Financial Management

10–20%

Area IV

Information Technology

15–25%

Area V

Operations Management

15–25%

BEC3

Uniform CPA Examination Blueprints: Business Environment and Concepts (BEC)

Area II of the BEC section blueprint covers several topics related to Economics,

including the following:

• Understanding business cycles and economic indicators and explaining the

impact of government intervention in a market

• Quantifying the effect of changes in economic conditions on an entity’s

products

• Determining the business reasons for, and the underlying economic substance

of, transactions and their accounting implications

• Measuring nancial risks to a business and the effect of implementing mitigating

strategies

Area III of the BEC section blueprint covers several topics related to Financial

Management, including the following:

• Assessing the factors inuencing a company’s capital structure, such

as risk, leverage, cost of capital, growth rate, protability, asset structure and

loan covenants

• Calculating metrics associated with the components of working capital, such

as current ratio, quick ratio, cash conversion cycle and turnover ratios to

determine the impact of business decisions on working capital

• Understanding commonly used nancial valuation and decision models and

applying that knowledge to assess assumptions, calculate the value

of assets and compare investment alternatives

Section introduction

Business Environment and Concepts

(continued)

Area IV of the BEC section blueprint covers several topics related to

Information Technology (IT), including the following:

• Understanding the role of IT and systems in supporting an entity’s overall

vision, strategy and business objectives

• Identifying IT-related risks associated with an entity’s systems and

processes, such as change management and information security, including

cyber risks and risks introduced by relationships with third parties

• Identifying application and IT general control activities, whether manual,

IT dependent or automated, that are responsive to IT-related risks, such as

access and authorization controls and business resiliency plans

• Obtaining and transforming data to prepare it for data analytics to support

business decisions

Area V of the BEC section blueprint covers several topics related to Operations

Management, including the following:

• Understanding business operations and use of quality control initiatives

and performance measures to improve operations

• Application of cost accounting concepts and use of variance analysis

techniques

• Utilizing budgeting and forecasting techniques to monitor progress and

enhance accountability

BEC4

Uniform CPA Examination Blueprints: Business Environment and Concepts (BEC)

Skill allocation

The Exam focuses on testing higher order skills. Based on the nature of the task,

each representative task in the BEC section blueprint is assigned a skill level.

BEC section considerations related to the skill levels are discussed below.

• Remembering and Understanding is tested in all ve areas of the BEC section.

Remembering and understanding tasks focus on the knowledge necessary

to demonstrate an understanding of the general business environment and

business concepts, such as those involving enterprise risk management.

Section introduction

Business Environment and Concepts

(continued)

• Application is also tested in all ve areas of the BEC section. Application

tasks focus on general topics such as those found in the subjects of

economics and information technology, and the day-to-day nancial

management tasks that newly licensed CPAs perform, such as those

involving calculations involving ratios, valuation and budgeting.

• Analysis skills, tested in Areas I, II, III and V involve tasks that require a

higher level of analysis and interpretation. These tasks, such as comparing

investment alternatives using calculations of nancial metrics, nancial

modeling, forecasting and projection, frequently require newly licensed CPAs

to gather evidence to support inferences.

The representative tasks combine both the applicable content knowledge

and the skills required in the context of the work that a newly licensed CPA

would reasonably be expected to perform. The BEC section does not test any

content at the Evaluation skill level as newly licensed CPAs are not expected to

demonstrate that level of skill in regards to the BEC content.

Skill levels

Evaluation

The examination or assessment of problems, and

use of judgment to draw conclusions.

Analysis

The examination and study of the interrelationships

of separate areas in order to identify causes and nd

evidence to support inferences.

Application

The use or demonstration of knowledge, concepts

or techniques.

Remembering and

Understanding

The perception and comprehension of the

signicance of an area utilizing knowledge gained.

BEC5

Uniform CPA Examination Blueprints: Business Environment and Concepts (BEC)

Section introduction

Business Environment and Concepts

(continued)

References — Business Environment and Concepts

• The Committee of Sponsoring Organizations of the Treadway Commission (COSO):

– Internal Control – Integrated Framework

• Framework and Appendices

• Internal Control over External Financial Reporting: A Compendium of Examples

• Guidance on Monitoring Internal Control Systems Volume I, II and III

– Enterprise Risk Management – Integrating with Strategy and Performance

• Volume I and II

• Compendium of Examples

• Managing Cyber Risk in a Digital Age

• AICPA TSP 100: 2017 Trust Services Criteria for Security, Availability, Processing Integrity,

Condentiality, and Privacy (includes March 2020 updates)

• Sarbanes-Oxley Act of 2002:

– Title III, Corporate Responsibility

– Title IV, Enhanced Financial Disclosures

– Title VIII, Corporate and Criminal Fraud Accountability

– Title IX, White-Collar Crime Penalty Enhancements

– Title XI, Corporate Fraud Accountability

• Current business periodicals

• Current textbooks on:

– Accounting Information Systems

– Data Analytics (for accountants)

– Economics

– Finance

– Management Information Systems

– Managerial and Cost Accounting

– Production Operations

BEC6

Uniform CPA Examination Blueprints: Business Environment and Concepts (BEC)

Content area allocation Weight

I. Enterprise Risk Management, Internal Controls and Business

Processes

20–30%

II. Economics 15–25%

III. Financial Management 10–20%

IV. Information Technology 15–25%

V. Operations Management 15–25%

Skill allocation Weight

Evaluation —

Analysis 20–30%

Application 50–60%

Remembering and Understanding 15–25%

Business Environment and Concepts (BEC)

Summary blueprint

BEC7

Uniform CPA Examination Blueprints: Business Environment and Concepts (BEC)

Business Environment and Concepts (BEC)

Area I — Enterprise Risk Management, Internal Controls and Business Processes

(20–30%)

Skill

Content group/topic

Remembering and

Understanding

Application Analysis Evaluation Representative task

A. Enterprise risk management (ERM)

1. Purpose and

objectives

Dene ERM within the context of the COSO ERM framework, including the purpose and

objectives of the framework.

2. Components

and principles

Identify and dene the components, principles and underlying structure of the COSO

ERM framework.

Understand the relationship among risk, business strategy and performance within the

context of the COSO ERM framework.

Apply the COSO ERM framework to identify risk/opportunity scenarios in an entity.

B. Internal controls

1. Purpose and

objectives

Dene internal control within the context of the COSO internal control framework,

including the purpose, objectives and limitations of the framework.

2. Components

and principles

Identify and dene the components, principles and underlying structure of the COSO internal

control framework.

Apply the COSO internal control framework to identify entity-level risks (inherent and

residual) related to an organization’s compliance, operations and reporting (internal and

external, nancial and non-nancial) objectives.

Apply the COSO internal control framework to identify risks related to fraudulent nancial

and non-nancial reporting, misappropriation of assets and illegal acts, including the risk

of management override of controls.

Apply the COSO internal control framework to identify controls to meet an entity’s

compliance, operations and reporting (internal and external, nancial and non-nancial)

objectives at the entity and sub-unit level.

Describe the corporate governance structure within an organization (e.g., tone at the top,

policies, steering committees, oversight and ethics).

BEC8

Uniform CPA Examination Blueprints: Business Environment and Concepts (BEC)

Business Environment and Concepts (BEC)

Area I — Enterprise Risk Management, Internal Controls and Business Processes

(20–30%) (continued)

Skill

Content group/topic

Remembering and

Understanding

Application Analysis Evaluation Representative task

B. Internal controls (continued)

3. Sarbanes-Oxley Act

of 2002

Identify and dene key corporate governance provisions of the Sarbanes-Oxley Act

of 2002.

Identify regulatory deciencies within an entity by using the requirements associated with

the Sarbanes-Oxley Act of 2002.

C. Business processes

Describe the types and purposes of accounting and nancial reporting systems along

with the related tools and software, and the benets they provide to an entity’s business

processes.

Distinguish business process controls by type (e.g., preventive vs. detective, automated

vs. manual).

Identify the sequence of steps and the information, documents, tools and technology

commonly used in key business processes (e.g., sales, cash collections, purchasing,

disbursements, human resources, payroll, production, treasury, xed assets, general

ledger and reporting).

Identify the appropriate System and Organization Controls (SOC) for Service

Organizations report to meet a user entity’s needs and review the SOC report to obtain

information such as the period covered, modications and complementary user entity

controls.

Identify an appropriate mix of business process controls (e.g., segregation of duties,

input edit checks, authorization and approval, verications, physical controls, controls

over standing data, spreadsheet controls, reconciliations and supervisory controls) to

prevent or detect errors in transactions.

BEC9

Uniform CPA Examination Blueprints: Business Environment and Concepts (BEC)

Area I — Enterprise Risk Management, Internal Controls and Business Processes

(20–30%) (continued)

Skill

Content group/topic

Remembering and

Understanding

Application Analysis Evaluation Representative task

C. Business processes (continued)

Identify the appropriate techniques, methods, systems or other tools that could improve

the performance of a process.

Identify the structured and unstructured data needed to perform data analytics related

to a key business process and identify the appropriate analytic technique for a given

purpose.

Analyze the ow of transactions represented in a narrative, owchart, data diagram and

system interface diagram to identify the risks in key business processes related to the

completeness, accuracy and continued processing integrity in input, storage, processing

and output processes.

Business Environment and Concepts (BEC)

BEC10

Uniform CPA Examination Blueprints: Business Environment and Concepts (BEC)

Area II — Economics

(15–25%)

Skill

Content group/topic

Remembering and

Understanding

Application Analysis Evaluation Representative task

A. Economic and business cycles — measures and indicators

Understand the business cycle (trough, expansion, peak, recession) and leading, coincident and

lagging indicators of economic activity (e.g., bond yields, new housing starts, personal income

and unemployment).

Recall the characteristics of market types (e.g., perfect competition, monopolistic competition,

oligopoly, monopoly) as well as the common competitive strategies in each type.

Explain the impact on an entity’s industry and operations due to changes in government scal

policies, monetary policies, regulations and trade controls.

B. Market inuences on business

Use the laws of supply and demand and elasticity measures to explain the effect on a product.

Calculate the effect of ination on a product’s real price or an entity’s investments, debt and future

expenses.

Explain how changes in currency markets impact an entity.

Explain the opportunity cost of a business decision.

Determine the impact of market inuences on an entity’s business strategy, operations and risk (e.g.,

increasing investment and nancial leverage, innovating to develop new product offerings, seeking

new foreign and domestic markets and undertaking productivity or cost-cutting initiatives).

Determine the business reasons for, and explain the underlying economic substance of, signicant

transactions (e.g., business combinations and divestitures, product line diversication, production

sourcing and public and private offerings of securities).

Business Environment and Concepts (BEC)

BEC11

Uniform CPA Examination Blueprints: Business Environment and Concepts (BEC)

Area II — Economics

(15–25%) (continued)

Skill

Content group/topic

Remembering and

Understanding

Application Analysis Evaluation Representative task

C. Financial risk management

1. Market, interest

rate, currency,

liquidity, credit,

price and other

risks

Calculate and use ratios and measures to quantify risks associated with interest rates,

currency exchange, liquidity, prices, etc. in a business entity.

2. Means for

mitigating/controlling

nancial risks

Identify strategies to mitigate nancial risks (e.g., market, interest rate, currency and

liquidity) and quantify their impact on a business entity.

Business Environment and Concepts (BEC)

BEC12

Uniform CPA Examination Blueprints: Business Environment and Concepts (BEC)

Area III — Financial Management

(10–20%)

Skill

Content group/topic

Remembering and

Understanding

Application Analysis Evaluation Representative task

A. Capital structure

Describe an organization's capital structure and related concepts, such as cost of capital,

asset structure, loan covenants, growth rate, protability, leverage and risk.

Calculate the cost of capital for a given nancial scenario.

B. Working capital

1. Fundamentals

and key metrics

of working

capital

management

Calculate the metrics associated with the working capital components, such as current ratio,

quick ratio, cash conversion cycle, inventory turnover and receivables turnover.

Detect signicant uctuations or variances in the working capital cycle using working capital

ratio analyses.

2. Strategies for

managing

working

capital

Compare inventory management processes, including pricing and valuation methods, to

determine the effects on the working capital of a given entity.

Compare accounts payable management techniques, including usage of discounts, factors

affecting discount policy, uses of electronic funds transfer as a payment method and

determination of an optimal vendor payment schedule in order to determine the effects on the

working capital of a given entity.

Distinguish between corporate banking arrangements, including establishment of lines of

credit, borrowing capacity and monitoring of compliance with debt covenants in order to

determine the effects on the working capital of a given entity.

Interpret the differences between the business risks and the opportunities in an entity's credit

management policies to determine the effects on the working capital of a given entity.

Analyze the effects on working capital caused by nancing using long-term debt and/or

short-term debt.

Business Environment and Concepts (BEC)

BEC13

Uniform CPA Examination Blueprints: Business Environment and Concepts (BEC)