The Time Value of Money

Warren Buffett’s Advice

On spending, “If you buy things you do not

need, soon you will have to sell things you

need”

On savings, “Do not save what is left after

spending, but spend what is left after saving”

On earnings, “Never depend on single income,

make investment to create a second source”

On investment, “Do no put all eggs in one

basket”

On taking risks, “Never test the depth of river

with both the feet”

Lecture Outline

Future Value and Compounding

Present Value and Discounting

Discount Rate

Number of Periods

Annuities and Perpetuities

Formulas for Annuities and Perpetuities

EAR and APR

Interest Rates and Inflation

Basic Definitions

Present Value – earlier money on a time line

Future Value – later money on a time line

Interest rate – “exchange rate” between

earlier money and later money

The Timeline

Assume that you are lending $10,000 today and

that the loan will be repaid in two annual

$6,000 payments.

5

Three Rules of Time Travel

6

The 1st Rule of Time Travel

A dollar today and a dollar in one year

are not equivalent.

It is only possible to compare or combine

values at the same point in time.

7

The 2nd Rule of Time Travel

To move a cash flow forward in time, you must

compound it.

• Future Value of a Cash Flow

n

n

rC

n

rrrCFV ) (1

times

) (1 ) (1 ) (1

8

The 3rd Rule of Time Travel

To move a cash flow backward in time, we

must discount it.

Present Value of a Cash Flow

PV C (1 r )

n

C

(1 r )

n

9

Combining Values Using

the Rules of Time Travel

Suppose we plan to save $1000 today, and

$1000 at the end of each of the next two

years. If we can earn a fixed 10% interest

rate on our savings, how much will we

have three years from today?

10

The time line would look like this:

11

12

13

14

0

3 4 521

$10,000

$5,000

Assume that an investment will pay you

$5,000 now and $10,000 in five years.

◦ The time line would like this:

15

0

3 4 521

$6,209 $10,000

$5,000

$11,209

÷ 1.10

5

You can calculate the present value of the

combined cash flows by adding their values

today.

16

0

3 4 521

$5,000 $8,053

x 1.10

5

$10,000

$18,053

You can calculate the future value of the

combined cash flows by adding their

values in Year 5.

17

0

3 4 521

$11,209 $18,053

÷ 1.10

5

0

3 4 521

$11,209 $18,053

x 1.10

5

Present

Value

Future

Value

19

The Power of Compounding

20

Rule of 72

21

Valuing a Stream of Cash Flows

Based on the first rule of time travel we

can derive a general formula for valuing a

stream of cash flows: if we want to find

the present value of a stream of cash

flows, we simply add up the present

values of each.

22

Present Value of a Cash Flow Stream

PV PV (C

n

)

n 0

N

C

n

(1 r)

n

n 0

N

23

Example

24

Annuities and Perpetuities Defined

Annuity – finite series of equal payments

that occur at regular intervals

◦ If the first payment occurs at the end of the

period, it is called an ordinary annuity

◦ If the first payment occurs at the beginning of

the period, it is called an annuity due

Perpetuity – infinite series of equal

payments

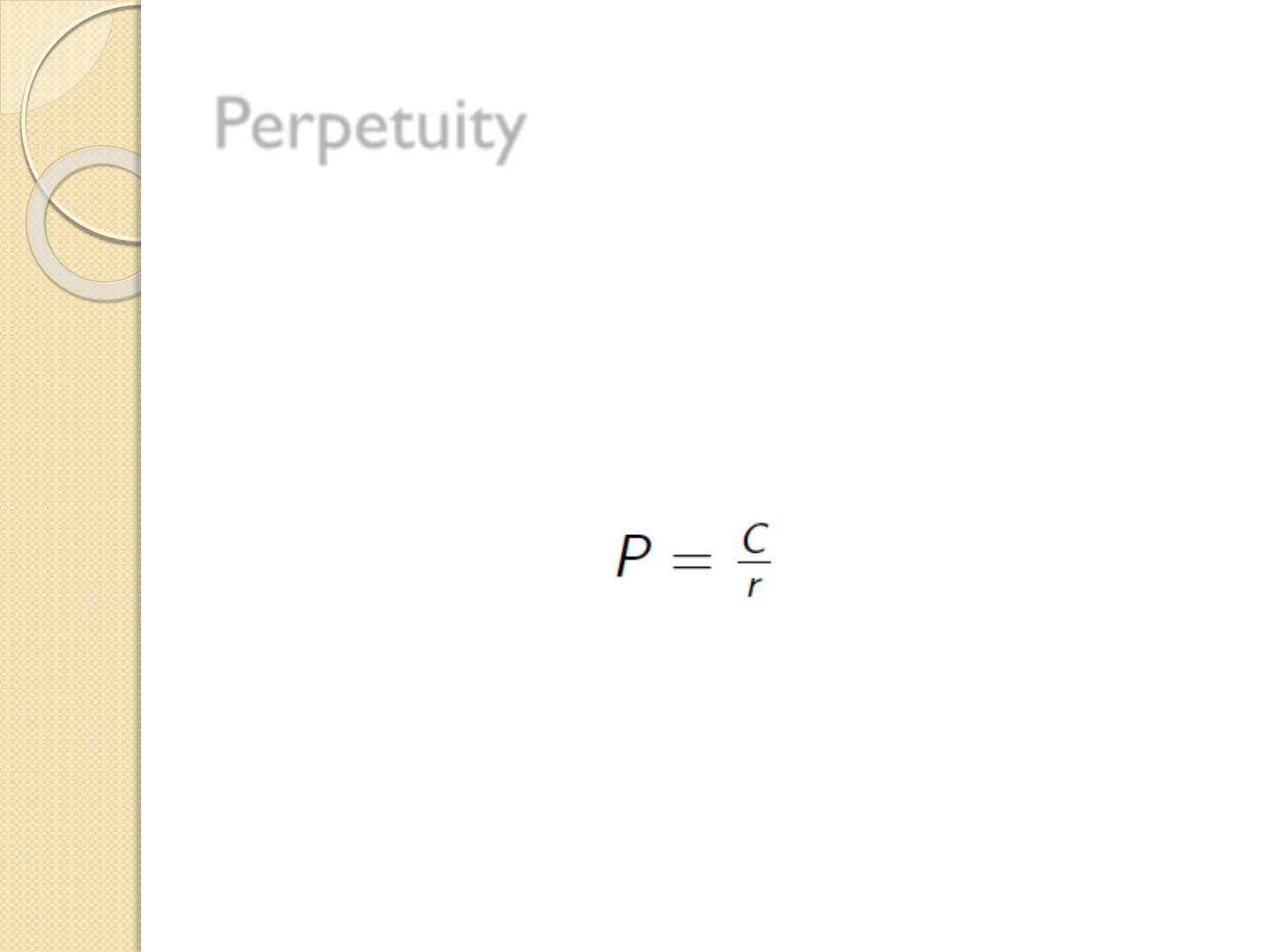

Valuing a Perpetuity

A perpetuity is a constant stream of cash

flows lasting forever.

Mathematically,

Suppose you bought the perpetuity today

and sold it for P1 in a year. The PV of the

perpetuity is the PV of the cash flow C+P1

But the PV of the perpetuity must be the

same at each point of time because the

future cash flows are identical. So

Thus, or or

Valuing a Perpetuity

Alternatively…

Mathematically, summing a geometric series

that goes to infinity:

Perpetuity is:

A =

r =

What is P?

Value a Growing Perpetuity

A growing perpetuity provides a cash flow of

$C in one year, and grows at a rate of g each

subsequent year. The cash flows from a

growing unit perpetuity looks like this (g=5%)

Mathematically,

Suppose you bought the growing perpetuity

today and sold it for P1 in a year. The PV of

the perpetuity is the PV of the cash flow

C+P1

The price in 1 year must be (1+g) times its

price now, because its future cash flows are

all g% larger. So,

Thus, or

Valuing a Growing Perpetuity

Valuing an Annuity

An Annuity is a constant stream of cash

flows lasting for a fixed number of years.

The PV formula for an annuity is simply

time 0 perpetuity minus time t perpetuity

Valuing an Annuity

The PV of time 0 perpetuity is

The PV of time t perpetuity is

The value of the annuity is the difference:

What if the first payment occurs today

(year 0) rather than in a year?

What is the future value (at time 6) of the

annuity?

Valuing a Growing Annuity

A growing annuity is a stream of cash flows that

grows at a constant rate, say, g, for a fixed

number of periods. The cash flows of a growing

unit annuity look like this:

Again, the value of the growing annuity is

calculated by noting that it is a growing

perpetuity at year 0 minus a growing perpetuity

at year t

Valuing a Growing Annuity

The PV of time 0 growing perpetuity is

The time t growing perpetuity is and

its PV is

The value of the annuity is the difference:

Annuity (1) – Lottery Example

Annuity (2)

Suppose you deposit $50 a month into an account

that has annual interest of 9%, based on monthly

compounding. How much will you have in the

account in 35 years?

◦ Monthly rate = .09 / 12 = .0075

◦ Number of months = 35(12) = 420

◦ 35(12) = 420 N

◦ 9 / 12 = .75 I/Y

◦ 50 PMT

◦ CPT FV = 147,089.22

Finding the Payment (1)

Finding the Payment (2)

o 10 N

o 10,000,000 FV

o 5 I/Y

o CPT PMT = -795,046

Finding the Number of Payments (1)

o 8 I/Y

o 300,000 PV

o -45,000 PMT

o CPT N = 9.9

Finding the Rate

Future Values for Annuities

Perpetuity

Company A has an existing perpetual bond that

pays $1 quarterly, which is currently priced at

$40. If the company plans to raise $100 by

issuing a new perpetual bond that pays

quarterly, how much dividend per quarter

should the company pays?

Current required return:

◦ 40 = 1 / r

◦ r = .025 or 2.5% per quarter

Dividend for new perpetual bond:

◦ 100 = C / .025

◦ C = 2.50 per quarter

Growing Perpetuity

A company will pay an annual dividend next

year of $3. You expect its dividend to grow

at the rate of 5% per year forever. You

calculate that the expected return on their

equity should be 10%. What should be the

company’s price per share?

Important Notes

The previous examples are direct

applications of the annuity/perpetuity

formula.

In trickier scenarios, we need to be

careful about the timing of the cash flows.

◦ When do cash flows occur?

◦ How often do they occur?

What is the difference between an ordinary

annuity and an annuity due?

Ordinary Annuity

PMT PMTPMT

0 1 2 3

i%

PMT PMT

0 1 2 3

i%

PMT

Annuity Due

Annuity Due (1) – Lottery Example

Bob has just won the lottery, paying 20

equal installments of $50,000 each. He

receives his first payment now, i.e. at year

0. If the interest rate is 8 percent, what is

the present value of the lottery?

OR

Annuity Due (2)

You are saving for a new house and you put

$10,000 per year in an account paying 8%. The

first payment is made today. How much will you

have at the end of 3 years?

◦ Set Type=1

◦ 3 N

◦ -10,000 PMT

◦ 8 I/Y

◦ CPT FV = 35,061.12

Delayed Annuity - Saving For

Retirement Example

You are offered the opportunity to put

some money away for retirement. You will

receive four annual payments of $500

each beginning at year 6. How much

would you be willing to invest today if you

desire an interest rate of 10%?

An Infrequent Annuity

Charlie receives an annuity of $450, payable

once every two years. The annuity stretches

out over 20 years. The first payment occurs

at date 2, that is, two years from today. The

annual interest rate is 6 percent. What is the

present value of the annuity?

The (annual) interest rate over two-year

period, denoted by R, is

So,

Multiple Annuities

An insurance agent approaches Debra and

would like to sell her the following contract: (1)

Debra pays $5,000 per year for the coming 15

years. (2) In return, she will receive $7,000 a

year for the following 15 years.

Assume that interest rates will remain at a

constant 9%. How much profit does the

insurance company make? In order for the deal

to generate zero profits, what an annual

payment does Debra need to receive?

The insurance company’s profit:

For zero profit, we need:

Multiple Annuities (con’t)

Decisions, Decisions

Your broker calls you and tells you that he has this

great investment opportunity. If you invest $100

today, you will receive $40 in one year and $75 in

two years. If you require a 15% return on

investments of this risk, should you take the

investment?

◦ CF

0

= 0; C01 = 40; C02 = 75

◦ I = 15

◦ CPT NPV = 91.49

◦ No – the broker is charging more than you would be

willing to pay.

Perpetuity

◦ A constant stream of cash flows that lasts forever.

Growing perpetuity

◦ A stream of cash flows that grows at a constant rate

forever.

Annuity

◦ A stream of constant cash flows that lasts for a fixed

number of periods.

Growing annuity

◦ A stream of cash flows that grows at a constant rate for

a fixed number of periods.

Summary

We presented four simplifying formulae:

r

C

PV :Perpetuity

gr

C

PV

:Perpetuity Growing

T

rr

C

PV

)1(

1

1:Annuity

T

r

g

gr

C

PV

)1(

1

1 :Annuity Growing

Summary